Armada Hoffler Properties (NYSE:AHH) recently bought The Interlock, which will most likely bring further rental revenue in the coming years. There is also information about recent divestitures, which may enhance the way the balance sheet looks, and may lower the total amount of leverage. Additionally, I do believe that the stock repurchase program announced in 2023 will most likely bring stock demand, and may enhance the stock price. Yes, I do see some risks from the total amount of debt or lack of new suitable acquisitions, however, I believe that the stock appears cheap right now.

Armada Hoffler Properties

With more than 40 years of experience in the development, construction, acquisition, and management of commercial office and multifamily residential buildings in the United States, Armada Hoffler is an independent real estate company with a presence in the Southeastern states and the Atlantic coast of the United States.

In addition to its core business in land development and housing construction, the company also offers construction and development services to other market participants. By April 2023, Armada Hoffer had 97% occupancy of its homes and offices.

The activities are divided into commercial office rentals, retail real estate rentals, multifamily housing activities, and the offering of services for other developers in the real estate industry, thus forming four operating segments according to which the structure of the company is organized.

Armada Hoffler maintains an active acquisition strategy for the purchase and remodeling of old buildings in commercial and residential areas mentioned above, having at its disposal important constructions in cities with great consumer activity, receiving income directly from the occupants in terms of the rental of properties. In some cases, buildings are rented by entire floors to other companies to use as headquarters for their operations in that region. On some occasions, the buildings are sold for the development of other companies.

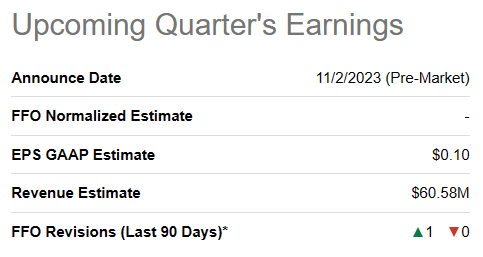

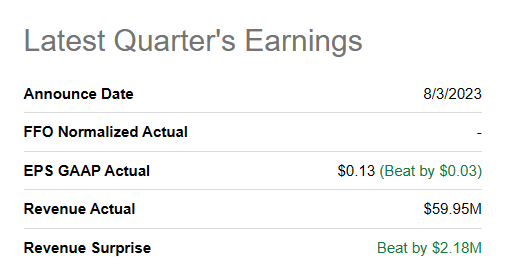

Taking into account the incoming quarterly earnings results, I believe that it is a great time for assessing the current valuation of the company. Analysts are expecting quarterly revenue of close to $60 million, however, final results may be a bit better. Let’s keep in mind that in the previous earnings results, the company reported better-than-expected results.

Source: SA Source: SA

Balance Sheet

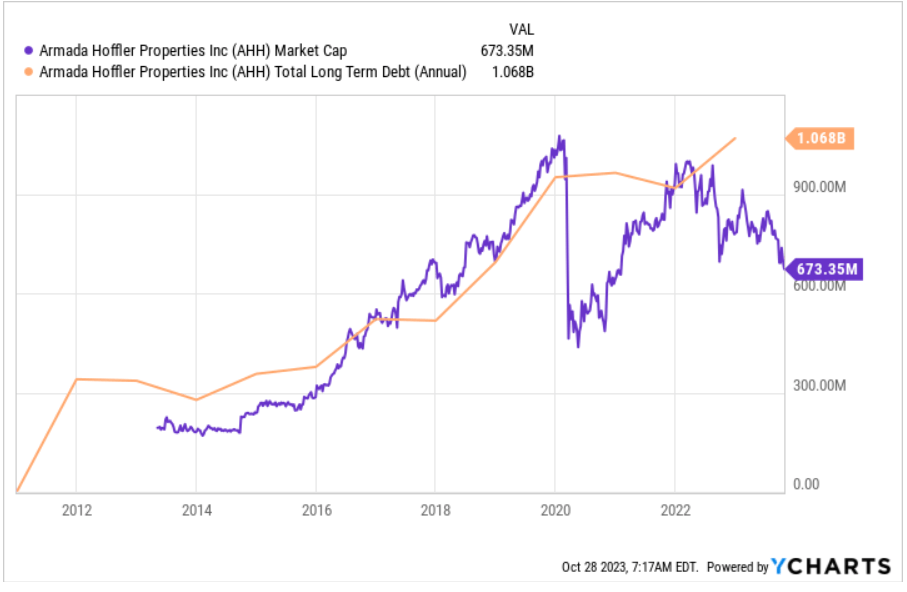

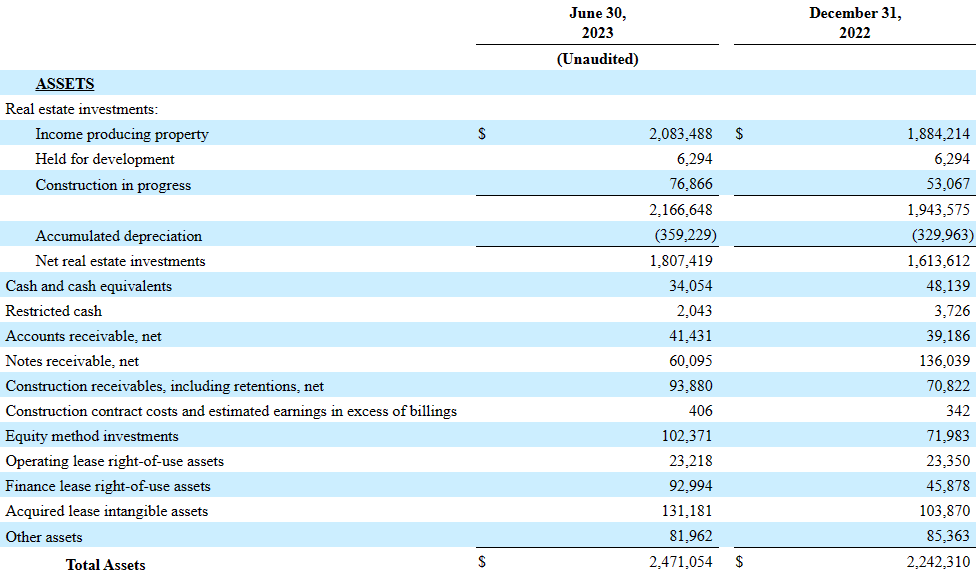

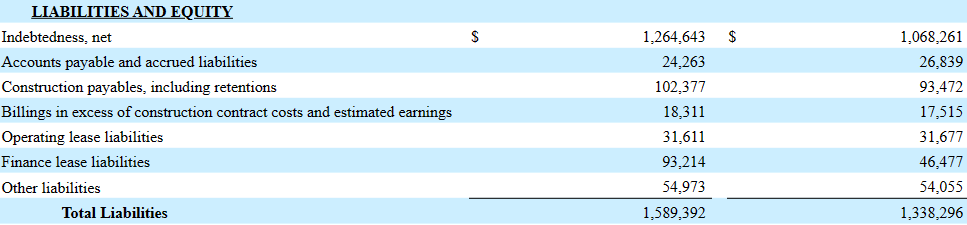

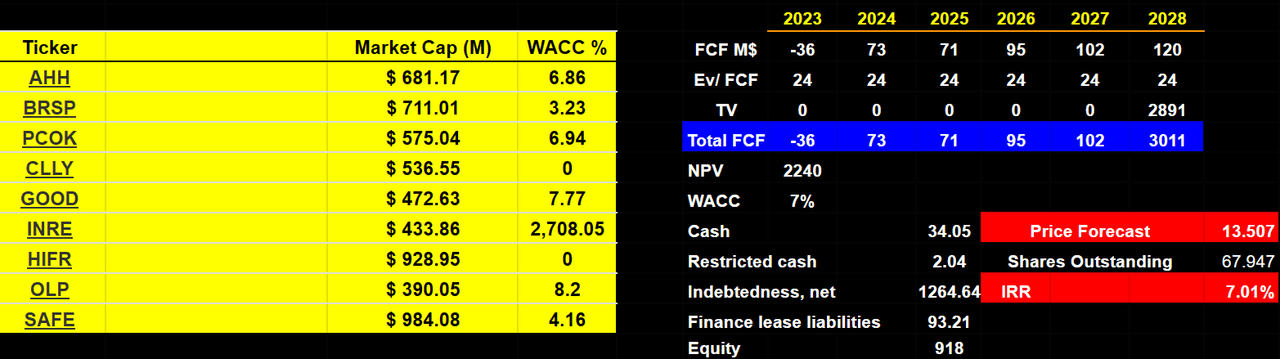

As of June 30, 2023, the company reported income-producing property worth $2.083 billion and net real estate investments worth $1807 million. Armada Hoffler Properties reports a market capitalization close to $600-$750 million, and the total long-term debt does not exceed $1.3 billion. With these figures in mind, I do believe that Armada Hoffler Properties appears undervalued.

Source: YCharts

The company also reported cash and cash equivalents worth $34 million, restricted cash of $2 million, accounts receivable of about $41 million, and construction receivables, including retention of about $93 million. Total assets stand at about $2.471 billion, and the asset/liability ratio is around 1x-2x. I believe that the balance sheet looks clean.

Source: 10-Q

With indebtedness of around $1264 million, accounts payable and accrued liabilities worth $24 million, and construction payables, including retentions close to $102 million, total liabilities are equal to $1.589 billion.

Source: 10-Q

According to the last quarterly report, Armada Hoffler Properties is paying interest rates close to 6% and 7%, but also lower than these interest rates. With this in mind, I believe that assuming a WACC of 7% appears conservative.

As of June 30, 2023, the effective interest rates on the revolving credit facility and the term loan facility, before giving effect to interest rate caps and swaps, were 6.64% and 6.54%, respectively. After giving effect to interest rate caps and swaps, the effective interest rates on the revolving credit facility and the term loan facility were 4.59% and 2.45%, respectively, as of June 30, 2023. Source: 10-Q

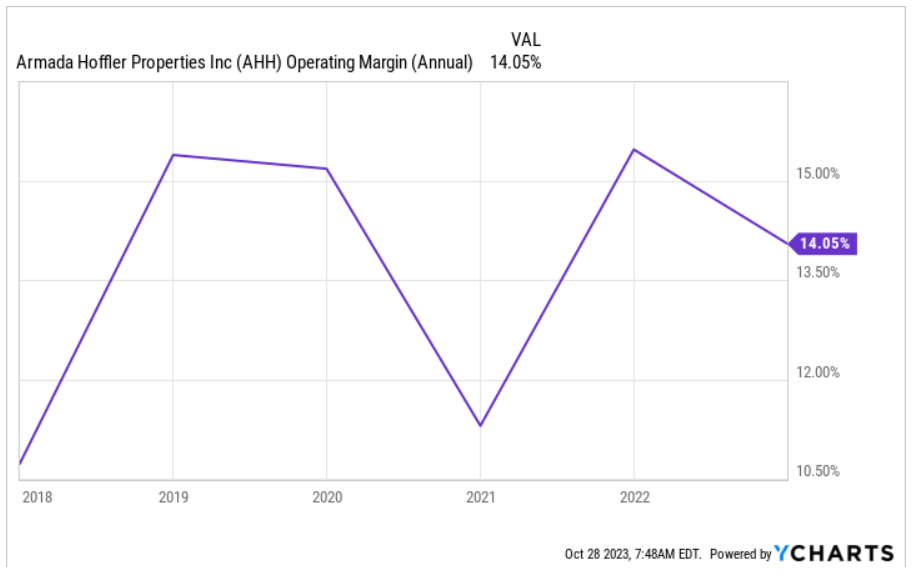

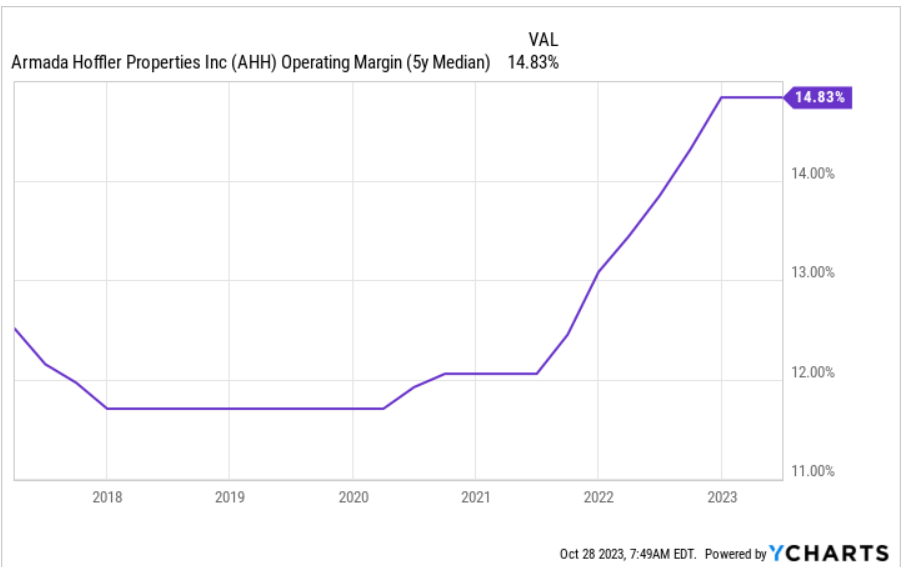

Further Acquisition Of Properties Will Most Likely Bring Operating Margin Growth And FCF Growth

The current strategy for this company continues to be the same that guided it to obtain positive results at an operational and financial level: to develop first-class properties for commercial and residential use within the markets where it has its activities. This strategy has as components the acquisition of properties with potential value in their remodeling as well as the construction of buildings in some cases, in joint agreements with other industry participants. The objective is to achieve an intelligent and disciplined movement of capital in order to increase the value of the properties under ownership. Under my forecasts, Armada Hoffler would be successful in the acquisition and development of properties, and economies of scale will most likely continue to play a major role in operating profit margin growth.

Source: YCharts Source: YCharts

Further Increase In The Relationship With State Institutions And Private Participants In The Industry Will Most Likely Bring Net Sales Growth

In addition to continuing the development of value opportunities within the commercial and residential housing markets, I believe that there will most likely exist opportunities that are aimed to increase public and private relations with state institutions and private participants in the industry. In addition, these opportunities will likely aim to allocate investments to increase the productive capacity of its construction segment, which would also serve to diversify the rental business which is the core element of the company’s model. As a result, I believe that we may see FCF growth in the next few years.

In particular, I believe that the recent acquisition of The Interlock in West Midtown Atlanta with a combination of cash and debt will most likely bring further increase in the book value per share and net sales growth. As a result of the transaction, I would be expecting further increase in the net sales growth thanks to office and retail space rentals.

On May 19, 2023, we acquired The Interlock, a 311,000 square foot Class A commercial mixed-use asset in West Midtown Atlanta anchored by Georgia Tech. As part of this acquisition, we paid $6.1 million in cash, redeemed our outstanding $90.2 million mezzanine loan, issued $12.2 million of Class A units of limited partnership interest in the Operating Partnership to the seller, and assumed the asset’s senior construction loan of $105.6 million, that was paid off on the acquisition date using the proceeds of the TD term loan facility and an increase in borrowings under the revolving credit facility. Source: 10-Q

At this point, due to the magnitude of the projects carried out and the collaboration with the Commonwealth of Virginia or even with the Kingdom of Sweden, Armada Hoffler enjoys great recognition in the markets of the Eastern United States, which of course grants it a wide margin of realization and access to lands and joint agreements. I believe that these connections may bring further contracts and business growth.

We have extensive experience with public/private real estate development projects dating back to 1984, having worked with the Commonwealth of Virginia, the State of Georgia, and the Kingdom of Sweden, as well as various municipalities. Through our experience and longstanding relationships with governmental entities such as these, we have learned to successfully navigate the often complex and time-consuming government approval process, which has given us the ability to capture opportunities that we believe many of our competitors are unable to pursue. Source: 10-k

Armada Hoffler Noted That It May Divest Certain Properties, Which May Bring Cash In Hand, And Enhance The Company Valuation

The fact that the company is ready to sell certain properties could also bring significant cash in hand, and lower leverage in the coming years.

We intend to opportunistically divest properties when we believe returns have been maximized and to redeploy the capital into new development, acquisition, repositioning, or redevelopment projects that are expected to generate higher potential risk-adjusted returns. Source: 10-k

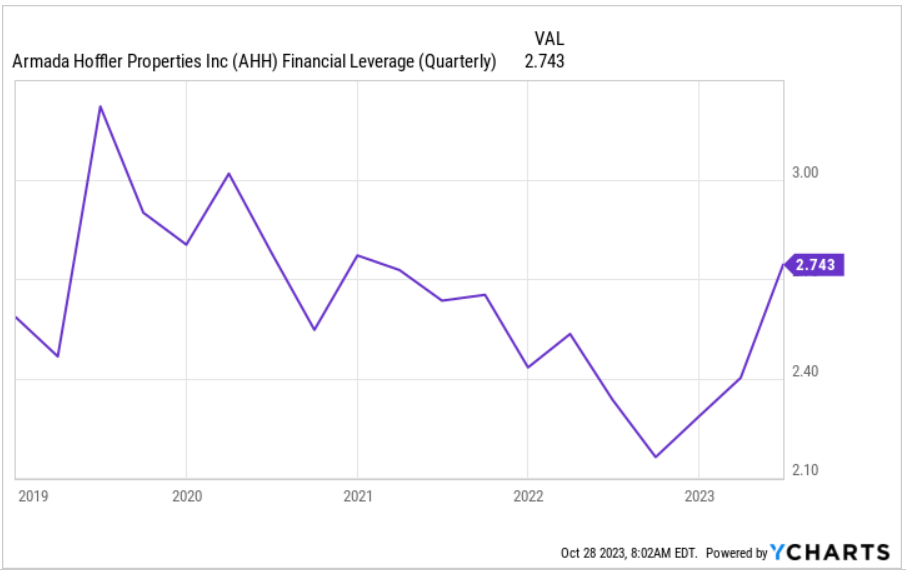

Financial leverage appears to be decreasing as compared to the level in 2019. In my view, further decrease in the total amount of leverage will most likely bring more investors to the market. The demand for the stock could increase.

Source: YCharts

The company reported the sale of certain assets in 2023, so I believe that we are not only talking about words. Divestitures are happening.

On April 11, 2023, we completed the sale of a non-operating outparcel at Market at Mill Creek in full satisfaction of the outstanding consideration payable for the acquisition of the noncontrolling interest in the property completed on December 31, 2022. Source: 10-Q

The Share Repurchase Program Will Most Likely Bring Demand For The Stock

In June 2023, the company reported a share repurchase program of about $50 million, which may bring significant demand for the stock and could enhance the stock price. The fact that management decided to run a repurchase program could indicate that management believes that the stock is cheap.

On June 15, 2023, the Company adopted a $50.0 million share repurchase program. Under the Share Repurchase Program, the Company may repurchase shares of common stock and Series A Preferred Stock from time to time in the open market, in block purchases, through privately negotiated transactions, the use of trading plans intended to qualify under Rule 10b5-1 under the Securities Exchange Act of 1934, as amended, or other means permitted. Source: 10-Q

DCF Model

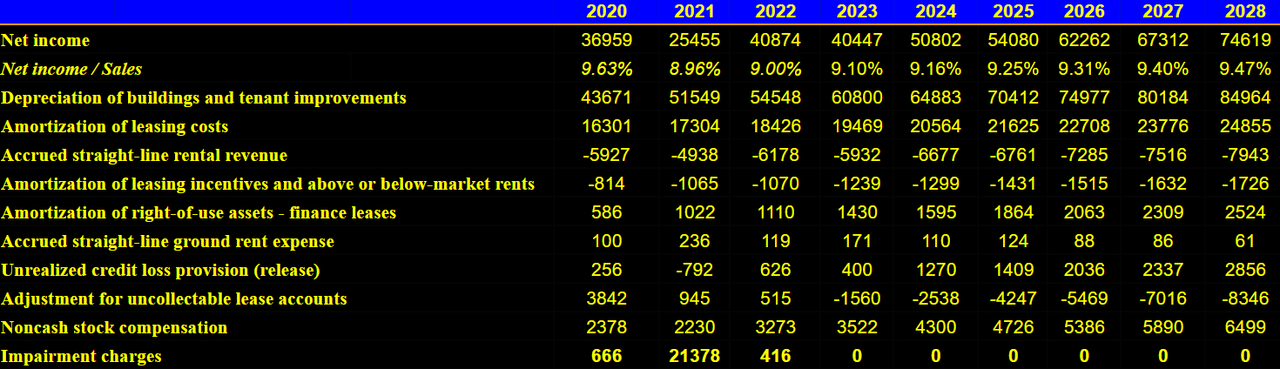

My revenue forecast by segment includes 2028 rental revenues of $378 million and 2028 general contracting and real estate services revenues close to $409 million. Finally, total revenues would be close to $788 million.

Source: DCF Expectations

I assumed growing net income/sales close to 9%-9.4% with 2028 net income of close to $74 million, accrued straight-line rental revenue of about -$8 million, amortization of leasing incentives and above or below-market rents close to -$2 million, and amortization of right-of-use assets close to $2 million.

Source: DCF Expectations

Also, with non-cash stock compensation close to $6 million, non-cash interest expense of about $22 million, and property assets of close to -$36 million, I included changes in construction liabilities of $309 million, which implied 2028 CFO of $497 million. Finally, with acquisitions of real estate investments close to -$377 million, 2028 FCF would be about $120 million.

Source: DCF Expectations

Other competitors report a WACC close to 8% and 3%, so I assumed that a WACC of 7% would be conservative. Besides, with a terminal EV/FCF of 24x, the implied forecast would be around $13-$15 per share with an IRR of 7%. Other analysts may use other figures, but I believe that their conclusions would most likely not be far from those of mine.

Source: DCF Expectations

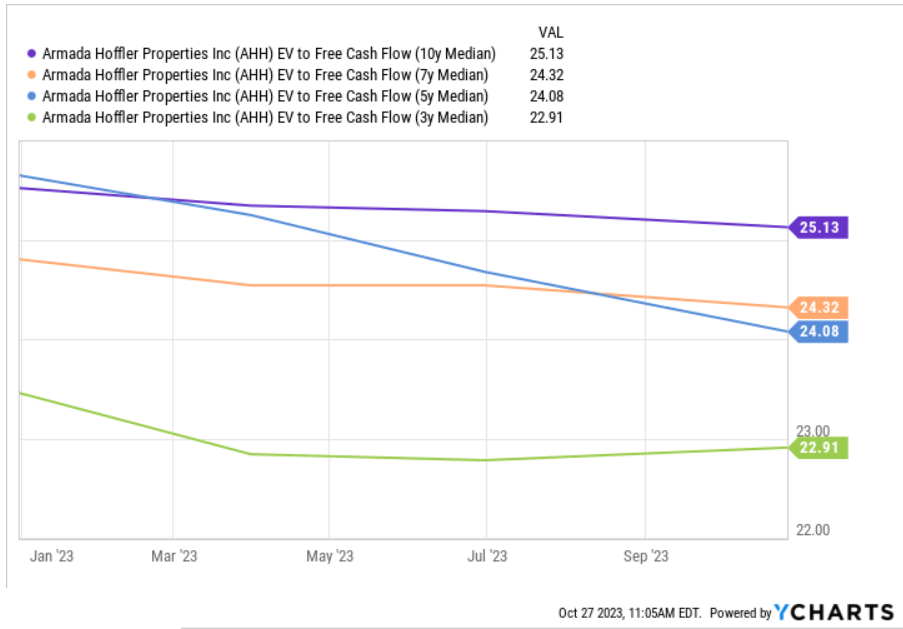

Note that Armada Hoffler Properties traded at close to 22x-25x FCF in the past, so I believe that my EV/FCF multiple appears reasonable.

Source: YCharts

Competitors

The competition for this company is high and is given by companies that offer services and develop similar activities, and they have, in several cases, greater capabilities and access to resources. To a lesser extent, a series of minor and independent participants complete the competitive environment within the aforementioned regional markets. Competition exists for the acquisition of land and the negotiation of rental contracts or purchase contracts for properties. The competition also extends to the construction segment. In this last aspect, although it is the most modern of the businesses in progress, the company is confident that it has the necessary development capabilities to compete at a large scale in the short term.

Risks

The risks are various and largely depend on the management capacity and recognition of business opportunities in land or homes to be developed. Likewise, the company has almost total dependence on local economies, and the business of this company is subject to the development of the real estate market in particular, but of economic activity in general, the insertion of new companies, and the payment capacity of its clients. More so, we should take into account that in the last year almost 50% of its revenue came from retail rental activity.

Armada Hoffler’s ability to increase the value of its properties will be a risk factor in the short and long term due to the nature of the real estate business and the availability of capital to finance future operations.

Conclusion

Armada Hoffler Properties recently bought The Interlock, which will most likely bring rental revenue growth increases in the coming years. The company also intends to divest certain properties. Additionally, the company recently enacted a new stock repurchase program, which may bring further demand for the stock and may enhance future stock valuations. I do see risks from the total amount of debt or the inability to find new acquisitions at decent valuations, however, the stock remains significantly undervalued.

Read the full article here