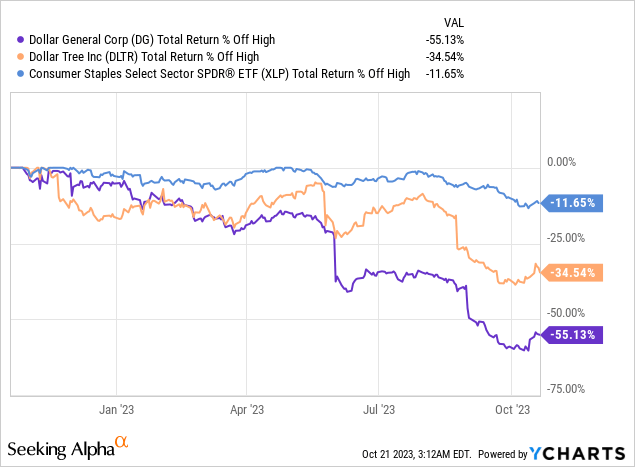

The magnitude of decline in dollar shop stocks is comparable to previous economic recessions.

Supply chain issues, stacked inventories, narrowing margins, slashed earnings projections and a pessimistic economic atmosphere are the primary culprits of this fall. It was usually the consumer staples stocks that offered protection to our capital. But this plummet has made many investors question whether these stocks are still safe haven in an economic recession. Nevertheless, I opine that this surprising state of dollar shop stocks provides a rare opportunity for investors.

The magnitude of decline in dollar shops stocks are comparable to previous economic recessions.

A Quick Review on Stock Performance

The performance of Dollar General (NYSE:DG) and Dollar Tree (DLTR) was jaw-dropping in 2023, in a negative way.

DG and DLTR fell 55.1% and 34.5% from their 52-week high, respectively, which contrasted greatly with the consumer staples sector and the broader market.

Reviewing the history of DLTR, there were only five times that the stock dropped over 40% post Dot-com Bubble. The last time it plummeted by 50% was when COVID-19 hit the globe. But it eventually recovered in a year and gained almost 200%.

I utilized DLTR as a reference, as DG was only listed in the middle of the Global Financial Crisis in 2009.

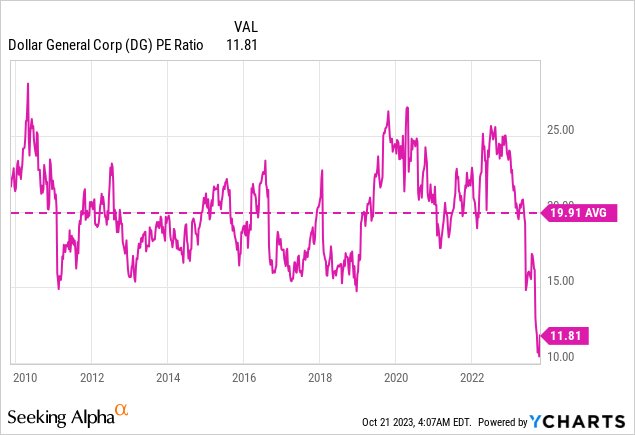

So, when Dollar General is suffering the biggest drop in its 14-year history and trading at a historically low P/E ratio, it is worth looking at it.

Major concerns

The major concerns of investors can be categorized into two groups:

1. Consumers are having financial difficulties

The multi-decade high inflation since early 2022 hit consumers sentiment hard amid receding economic conditions, even though the National Bureau of Economic Research confirmed not to declare the inflationary economic downturn a recession. Nevertheless, the University of Michigan Consumer Sentiment Index dropped to a level lower than the Global Financial Crisis in 2008.

With inflation eroding purchasing power, consumers shifted to purchase staple goods from discretionary items.

The percentage of net sales of consumables (including paper and cleaning products, packaged food, perishables, snacks, etc.) rose from 76.8% in FY 2020 to 80.9% in the latest financial quarter. As discretionary products often have higher margins, the secular shift in consumer preferences caused DG suffering from margin compression. Thus, in the latest financial quarter, gross margin declined by 126 basis points year over year.

2. DG is facing growth ceiling

Dollar General benefited from the stimulus check and WFH trend in FY2020, leading to a significant gain in revenue and earnings. But its diluted EPS has been plateaued since then.

| 2019 | 2020 | 2021 | 2022 | 2023 | |

| Diluted EPS | $5.97 | $6.64 | $10.62 | $10.17 | $10.68 |

As discussed above, consumers had declining purchasing power, and thus their confidence was running low, which gave investors little hope for DG to reposition itself on the growth trajectory.

The underwhelming projections were reflected in the latest results. Its same-store sales dropped by 0.1%, and diluted EPS fell by 28.5%.

Thus, DG is arguably a company that lacks growth potential and should be punished.

Opportunities Revealed in Pessimistic Investing Atmosphere

Trading at a historic low P/E range, there is little doubt that DG right now is inexpensive, if not a bargain.

Despite strong arguments as I mentioned, I upgraded DG from “Hold” to “Buy” based on the following reasons:

1. Dollar General has a good track record

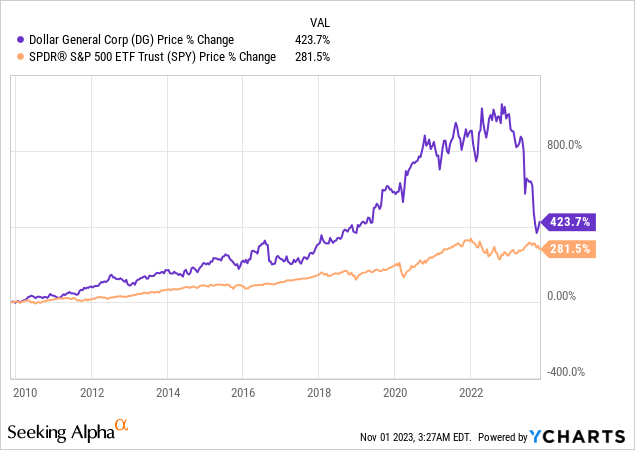

Dollar General is an investment-grade company with an excellent track record. Despite its disappointing performance this year, it still outperformed the S&P 500 by nearly 140% since inception in late 2009.

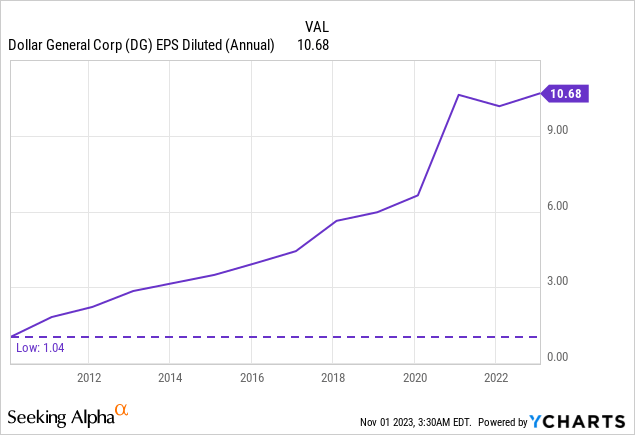

Earnings per share of Dollar General also ten-folded in the past twelve years, representing an impressive 22.3% CAGR.

The graphs above also displayed the unequal magnitude of growth between stock prices and earnings. As Peter Lynch advocated, “Stocks follow earnings”, the huge discrepancies between both may unveil an opportunity for investors.

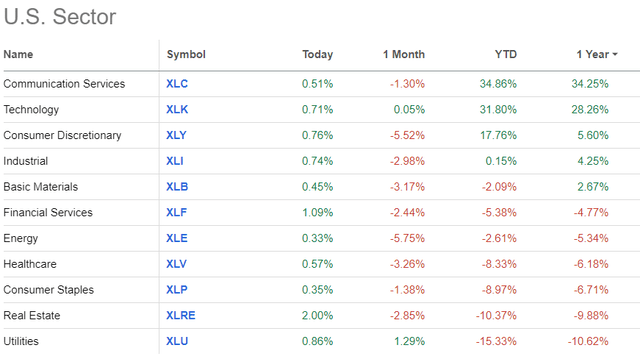

2. Dollar General are less affected by interest rate moves

Only real estate and utilities performed slightly worse than consumer staples sector worst performing sectors in the previous 52 weeks. It would be easier to search for bargains in an out-of-favour sector like these three.

Seeking Alpha

The valuation of real estate is very sensitive to interest rate change and thus affects stock prices significantly. On the flip side, a dollar shop’s valuation is less sensitive to interest rate moves.

Although interest rate hikes will increase DG’s interest payment for the newly issued debts, literally all of DG’s long-term debt obligations are fixed rate. And ~90% of its debt will not mature in the coming twelve months, which reduced the need for DG to issue new debt.

3. Dollar General is still expanding its business

Dollar General is an enormous company with almost 20,000 stores in the United States and Mexico. But it still endeavours to expand its territory by opening new stores. In the second quarter of 2023 alone, there are another 215 new stores are in business.

They also entered the Mexico market this year, targeting to operate up to 10 stores by the end of FY2023.

4. We may face a recession in 2024

Recession signals like ECRI leading economic index and inverted yield curves alert us that an economic recession may soon hit, despite the fact that it has been long-awaited.

During the economic downturn, consumer staples sector is often a popular choice over other sectors (e.g. tech stocks, consumer discretionary, etc.), as consumers intend to purchase less on discretionary products. Currently, investors view this trend as a bane for Dollar General as it leads to margin compression.

But a coin has two sides. The high proportion of essential product sales (~80% of net sales) provides Dollar General a cushion in a recession, where investors will see this as a boon.

5. Unpopular stocks may turnaround in the next cycle

I was reminded by Howard Marks in his book Mastering the Market Cycle that:

In times of extreme negativism, exaggerated risk aversion is likely to cause prices to already be as low as they can go, further losses to be highly unlikely, and thus the risk of loss to be minimal.

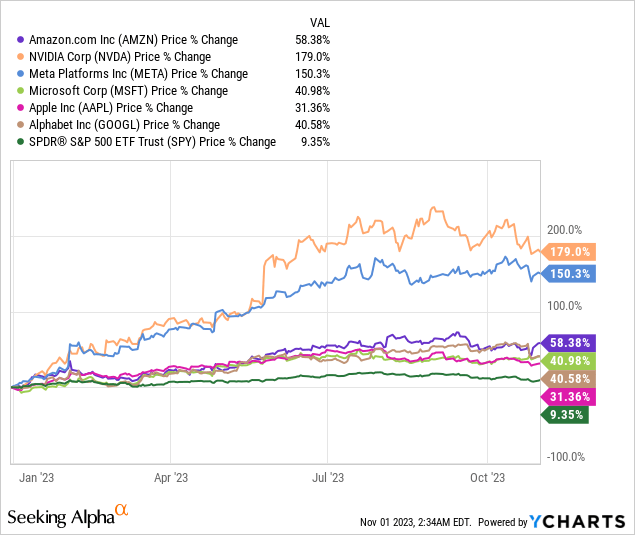

Let’s recall when tech stocks were unpopular in late 2022. Meta (META) and Amazon (AMZN) were trading at multi-year lows. Most people were sceptical about their prospects as they were falling short of investors’ expectations and laying off thousands of employees.

One year later, most popular tech stocks have turned the table, outperforming the broader market by a wide margin. It provides a perfect example that the out-of-favour sector may become popular again when market sentiment turns more optimistic.

I can’t tell either if Dollar General has hit the bottom, but the potential downside of DG has been so limited at its historically low valuation. And with the five bullish reasons I listed, I opined that Dollar General will have more upside opportunities in 2024.

Read the full article here