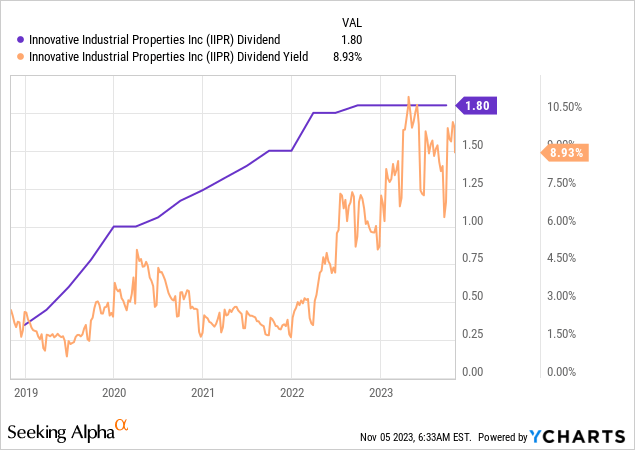

Innovative Industrial Properties (NYSE:IIPR) along with NewLake Capital (OTCQX:NLCP) form the only two publicly traded equity cannabis REITs. IIPR is the more investable REIT as it trades on the NYSE versus over the counter, going public in late 2016 during a loophole period that’s left the ticker as the only viable way to play the real estate space of an industry that’s being forecast to grow to reach $71 billion in sales in the US by 2030 even without federal legalization. The cannabis REIT last declared a quarterly cash dividend of $1.80 per share, unchanged from its prior payout for an 8.9% annualized forward yield.

With the Fed following through with a consecutive pause of interest rates at its November meeting, the equity market likely stands at the cusp of an even stronger everything rally. IIPR’s adjusted funds from operations saw year-over-year growth for its recent fiscal 2023 third quarter with the dividend now more comprehensively covered. The REIT is swapping hands for a 9x price to trailing 12-month AFFO multiple and has grown its dividend by a remarkable 15.4% compound annual growth rate over the last 3 years from its most recent quarterly payout.

Innovative Industrial Properties Fiscal 2023 Third Quarter Supplemental

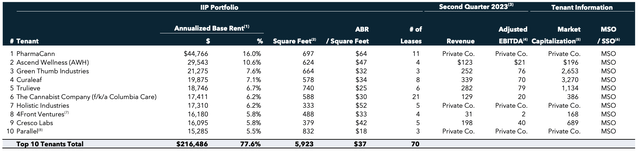

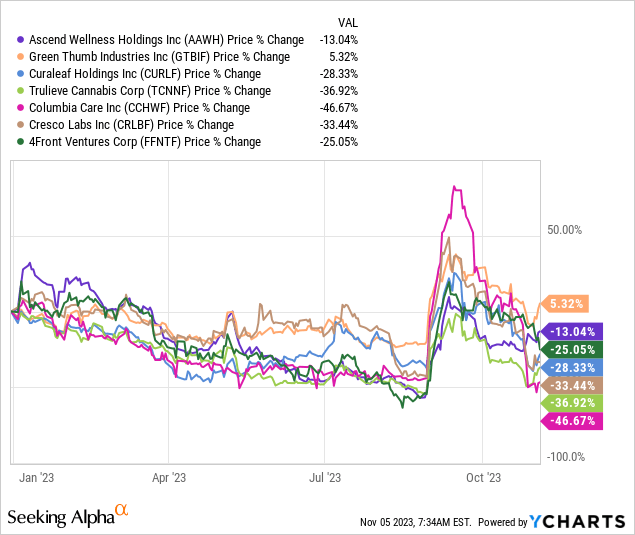

The headwinds being faced by the cannabis sector remain salient and just looking at the charts and financials of the publicly traded tranche of IIPR’s largest tenants reveals continued pains and what now seems like perpetual headwinds. These public MSOs form 50% of IIPR’s annualized base rent with a few of them flashing red in terms of liquidity. It’s important to flag that the series A preferreds (NYSE:IIPR.PR.A) currently offer a similar 8.8% yield to its holders.

Dual Beats As Industry Flashes Red

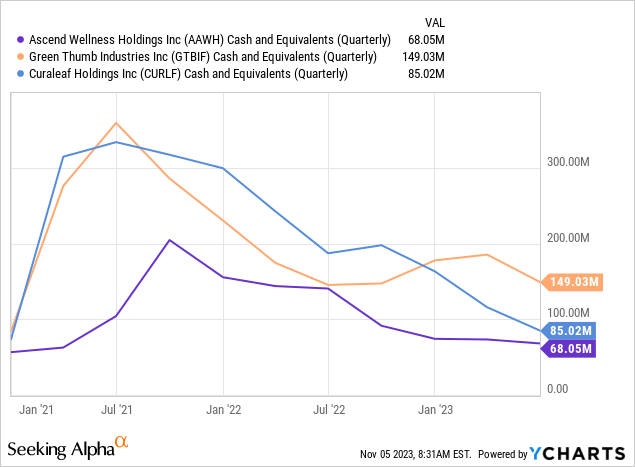

IIPR’s top 3 largest public tenants Ascend Wellness (OTCQX:AAWH), Green Thumb Industries (OTCQX:GTBIF), and Curaleaf Holdings (OTCPK:CURLF) are all facing declining liquidity set against flatlined sales and large total debt balances. Ascend’s total cash and equivalents as of the end of its last reported second quarter at $68 million, down from $140.6 million in its year-ago quarter with a long-term debt balance of $300.1 million. The MSO’s current market cap stands at $148 million and it recorded a negative levered free cash flow of $64.4 million for its trailing 12-month from the second quarter.

IIPR reported third-quarter revenue of $77.82 million, up 9.8% over its year-ago figure and a beat by $1.26 million on analyst consensus. Growth was driven by what was a $3.5 million increase in tenant reimbursements for property insurance premiums and property taxes to $6.2 million for the third quarter. Tenants previously paid real estate taxes directly to tax authorities before calendar 2023. IIPR’s rent collection for its operating portfolio came in at 97% for the third quarter, however, this included $2.2 million of security deposits applied with properties leased to Holistic Industries, Temescal Wellness, and 4Front Ventures.

The risk here is declining cash and the rising debt burden of its public tenants drives greater rent arrears even as rent collection remains relatively strong. It’s clear that there’s a looming liquidity headwinds and the extent to which it can be avoided will depend on current cost-cutting efforts and the ability of the tenants to raise more funds to extend their respective cash runways. Third quarter FFO came in at $2.09 to beat consensus estimates by 4 cents with AFFO of $2.29 per share, increasing by 7.5% over its year-ago comp.

Dividend Coverage And Debt

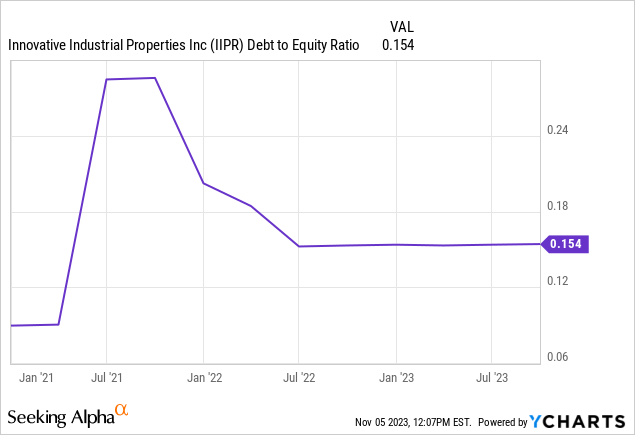

AFFO meant that the $1.80 per share dividend was 127% covered, around a 78% payout ratio. This came with $296 million of notes due in 2026 as of the end of the third quarter. Critically, IIPR’s total debt-to-equity ratio stood at a terrifically low 0.15x with its total equity ending the third quarter at $1.95 billion. This means that the REIT could at some point in the future lever up to the standard 1x ratio of the broader equity REIT universe to drive greater returns or take on more debt to maintain the dividend at its current level. The low ratio also embeds a greater level of flexibility in its balance sheet against what’s set to be a tight liquidity environment for its tenants.

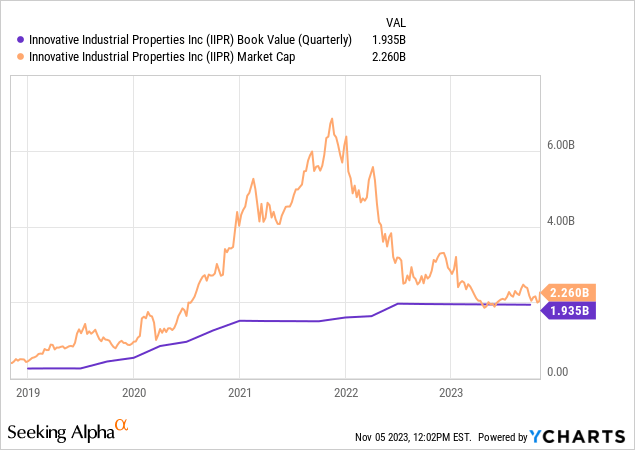

The REIT’s book value at $1.93 billion, around $69 per share, was down 81 cents from its year-ago period and dipped roughly 16 cents versus its second quarter. However, the premium of the commons over book value has fallen to lows at 16.8%. The next few months could see an everything rally for REITs and cannabis tickers alike as the market begins to more heavily price an end of Fed hawkishness with what’s currently a 95% chance that the Fed yet again keeps rates unchanged at its upcoming 13 December meeting. This has also brought up the real possibility of a 75 basis points rate cut by the end of 2024. I see 2024 being a more material year of recovery for IIPR’s commons if rent collection remains strong, the US economy does not slip into a recession, and inflation falls back to 2%. Do I think the common shares are a buy? Yes.

Read the full article here