Wall Street analysts seem to like buy-now-pay-later services company Affirm Holdings Inc., but most of them expect the stock to pull back — a lot — in 2024 after rocketing more than five-fold this year.

The financial technology company has benefited immensely during the holiday months, as a growing number of consumers, who have grown weary of inflation and rising borrowing costs, have embraced the delayed-payment options provided by BNPL providers.

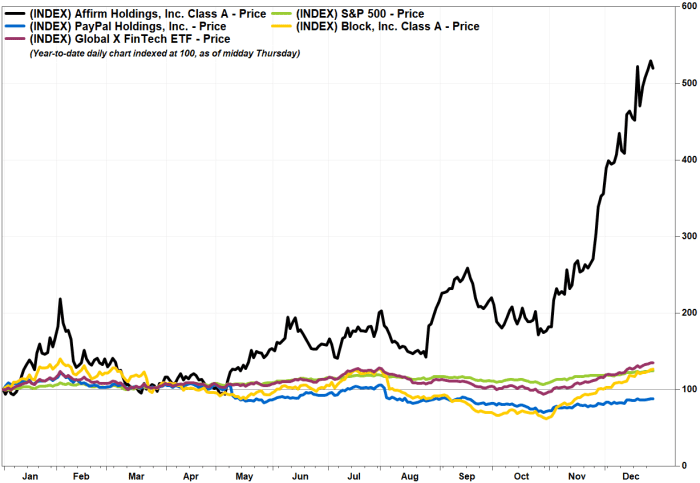

Affirm’s stock

AFRM,

has rocketed 420.7% year to date as of midday trading Thursday, including a near-tripling (up 186%) since the end of October.

Don’t miss: Affirm’s stock rockets after Walmart expands buy-now-pay-later option to include self-checkout purchases.

Truist analyst Andrew Jeffrey wrote in a recent note to clients BNPL volume on Cyber Monday, or the Monday following the Thanksgiving weekend, jumped 42.5% from a year ago, as consumers sought payment flexibility and shied away from legacy bank cards.

The Financial Brand, which analyzes financial services sector trends, reported that BNPL accounted for 8% of all spending on Cyber Monday, up from 6.5% on Amazon Prime Day just four months earlier, as Jeffrey noted.

Read: Affirm’s stock wins over a former skeptic as BNPL trends seem to be improving.

Also read: Affirm’s stock pops after earnings bring narrowing loss, big revenue beat.

But despite this bullish outlook on BNPL, Jeffrey is among the minority on Wall Street who recommend investors buy Affirms’ stock at current levels.

Of the 19 analysts surveyed by FactSet who cover Affirm, only six are bullish, while eight are neutral and five are bearish. The average 12-month stock price target is $29.24, which implies 42% downside from current levels.

Jeffrey’s been bullish on the stock since the beginning, and his 12-month stock price target of $55 is one of only two that are above current levels. (Affirm’s stock went public in January 2021.)

The other is Mizuho Securities analyst Dan Dolev’s 12-month target of $65.

“We expect the debate around Affirm to increasingly shift from BNPL and partnerships like Walmart, to [Affirm] becoming a full-fledged financial services firm with direct deposits, saving, etc.,” Dolev wrote in a note to clients.

Meanwhile, J.P. Morgan’s Reginal Smith is positive about Affirm’s prospects following a blowout earnings report, given the outlook for sustained growth, improving profitability and strong credit performance.

But Smith rates Affirm neutral and the 12-month price target of $35 implies about 30% downside: “We increasingly see Affirm as a core holding in our fintech coverage universe, but think shares are likely due for a breather.”

Even Wedbush’s David Chiaverini, who is among the most bearish on Affirm’s stock with a $15 price target given concerns over valuation, competition the health of consumers, views the company’s growth and profitability goals over the medium- and long-term as “net positive.”

Among Affirm’s biggest BNPL rivals, shares of PayPal Holdings Inc.

PYPL,

have shot up 21.5% since the end of October but have dropped 11.7% year to date, while Block Inc.’s stock

SQ,

has soared 98.4% over the past two months and has rallied 27.1% this year.

In comparison, the Global X FinTech ETF

FINX

has powered up 39.4% the past two months and hiked up 35.5% year to date, while the S&P 500 index

SPX

has gained 14.1% since October and advanced 24.7% this year.

Of the 48 analysts surveyed by FactSet who cover PayPal, 58% are bullish and the average 12-month stock price target of $73.99 implies about 18% upside.

And the bulk of analysts who cover Block are bullish — 36 out of 50 — even as the average stock price target of $76.19 is about 5% below current levels.

Read the full article here