March 12th ended up being a pretty positive day for shareholders of ArcelorMittal S.A. (NYSE:MT). Shares of the company popped up by 3.4%. And after the market closed on that day, news broke that the company agreed to acquire a sizable minority stake in a firm called Vallourec (OTCPK:VLOUF, OTCPK:VLOWY) in exchange for €955 million, or about $1.04 billion. Management made clear that they do not intend to put in an offer to buy up the rest of the business for at least the next six months. But given how cheap the stock currently is, it might not be a bad idea for a management to eventually consider doing that. All in all, this maneuver brings in additional significant value to shareholders. And investors would be wise to applaud the deal accordingly.

A necessary note

Unless otherwise stated, and even then on a case-by-case basis, all financial figures throughout this article will be in U.S. dollars. This includes historical financial results reported by Vallourec and terms of the deal between it and ArcelorMittal. For these figures, I am using the current exchange rate.

A great transaction

According to the press release issued by ArcelorMittal on March 12th, the company had agreed to acquire about 65.24 million shares, equating to 28.4% interest in, Vallourec in exchange for €14.64 per share. This comes out to roughly €955 million, or $1.04 billion. Instead of coming from the company directly in a move that would bring it additional capital but that would simultaneously result in a smaller ownership stake for ArcelorMittal, the shares are coming from funds managed by Apollo Global Management (APO).

ArcelorMittal

The management team at ArcelorMittal has lauded Vallourec for what it calls a “successful restructuring” that has occurred over the past few years. As you will see, this statement is most certainly true. But of course, it’s more than just financial data that matters. Also important is the product that Vallourec produces. You see, of the 2.2 million tons of annual rolling capacity that comes out of the company, an estimated 85% it’s centered around low carbon, integrated production hubs in the markets in which it operates. This would be the U.S. and Brazil. This is perfect, strategically, for ArcelorMittal because a whopping 13% of its revenue comes from the U.S., while a further 12.1% comes from Brazil. In fact, these are the two largest markets for ArcelorMittal from a sales perspective.

Operationally speaking, Vallourec focuses most of its efforts on the production and sale of tubes. The uses for the tubes the company produces are varied. For instance, for the oil and gas space, the company produces casing, tubing, and accessory products for the exploration and production mark it. The tubes that it makes can be used in associated with addressing pipe challenges for pipelines for transporting oil, gas, and refined products. They also offer seamless pipes for the processing of oil and gas. The enterprise operates in more than just the oil and gas market however. It actually caters to a variety of industries such as the automotive space, steel construction, and more. For instance, its automotive portfolio consists of tubes that are used for the production of axles and truck trailers. Its precision tubes can be used for airbags, diesel injection pipes, gear shafts, suspension components, and more. Some of these are even used in the railway industry. Geothermal wells require tubular solutions that can factor in high temperatures, corrosion, and more. The list of its offerings and their uses could fill up an article on its own.

Author – SEC EDGAR Data

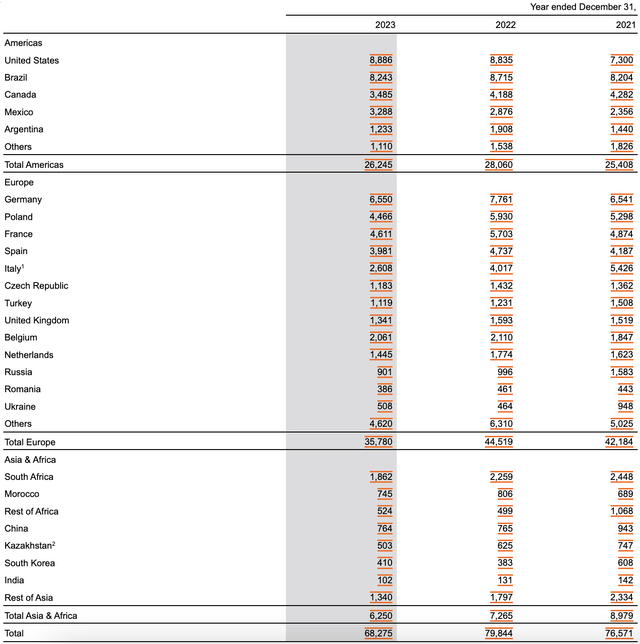

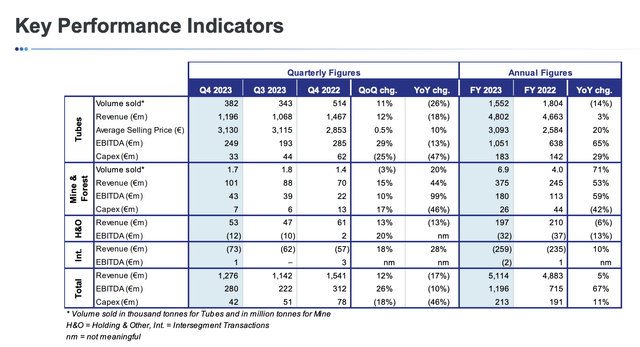

Using data from the 2023 fiscal year, it’s clear that the tube production operations of the company comprise the vast majority of what it does. About 93.9% of overall revenue for the enterprise comes from the Tubes segment. However, the company does have some other operations. For instance, it has a separate segment called Mine & Forests, which manages the iron ore mine and the forests that the company owns. The latter of these supplies charcoal to the blast furnace that it has in Brazil.

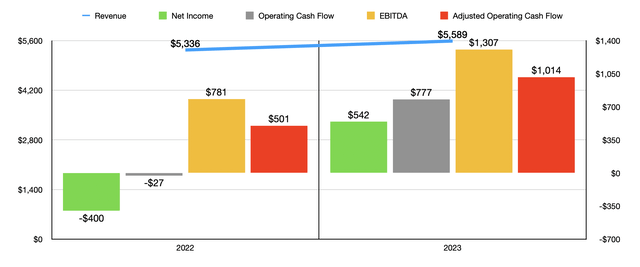

From a financial perspective, the picture has been improving for Vallourec and its investors. Take the time from 2022 to 2023 as an example. In 2023, the company generated a revenue of about $5.59 billion. That’s 4.7% above the $5.34 billion the company generated one year earlier. While the Mine & Forest segment of the company reported a sales increase from $245 million to $375 million, the largest share of the increase came from revenue for the Tubes segment growing from $5.10 billion to $5.25 billion. Although the total firm experienced a decline in tons sold from 1.80 million to 1.55 million, the price per ton shot up from $2,584 to $3,093. Under the Mine & Forest segment, the company also benefited from a rise in tons sold from 4 million to 6.9 million.

Vallourec

This increase in revenue brought with it higher profits as well. The firm went from generating a net loss of $400 million in 2022 to generating a net profit of $542 million last year. Other profitability metrics followed a very similar trajectory. Operating cash flow went from negative $27 million to positive $777 million. Even after adjusting for changes in working capital, we get a rise from $501 million to $1.01 billion. And lastly, EBITDA for the company jumped from $781 million to $1.31 billion. This increase in profitability has also allowed management to reduce overall debt. At the end of the most recent quarter, net debt stood at $685 million. That’s down from the $1.05 billion that the company had at the end of the 2021 fiscal year.

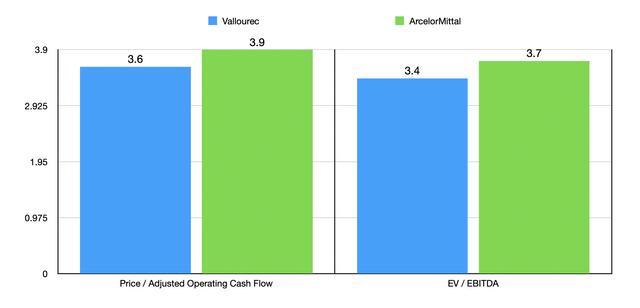

In addition to opening up a door toward additional market control, this purchase makes sense from a financial perspective. Based on the terms of the acquisition, ArcelorMittal is paying a price to adjusted operating cash flow multiple for the shares of 3.6. It’s also paying an EV to EBITDA multiple of 3.4. By comparison, ArcelorMittal on its own is trading at a price to adjusted operating cash flow multiple of 3.9 and at an EV to EBITDA multiple of 3.7. Given how cheap these shares are, management could easily justify taking on debt in order to make the transaction happen. But there is no need for that. While ArcelorMittal does have net debt of $2.90 billion, the gross cash that it has on hand totals $7.78 billion.

Author – SEC EDGAR Data

Takeaway

Down the road, who knows what will transpire between ArcelorMittal and Vallourec. I will say that an eventual purchase of the company in its entirety would probably be a wise decision. But even if that does not come to pass, this is an interesting purchase that increases ArcelorMittal S.A.’s market share in the two countries that it generates the most revenue from. I would argue that shares of both firms are very cheap at this time. But there is no denying that ArcelorMittal is paying a discount relative to what its own shares are trading for. When you add all of this together, I see this as a bullish development that investors should be excited about.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here