The sudden weakness in electric vehicle (“EV”) demand has knocked down lithium stocks, but a company like Lithium Americas Corp. (NYSE:LAC) is ultimately poised to bring a lithium mine online when demand is expected to return. The long-term EV story hasn’t been altered as some range anxiety and buyer incentives are resolved over time. My investment thesis is ultra-Bullish on the stock trading at the lows and de-risked with a DOE loan to fund mine development.

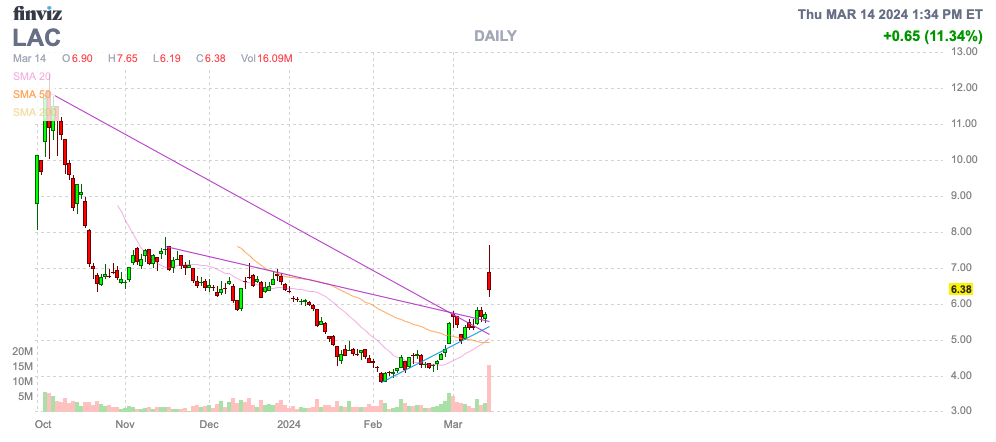

Source: Finviz

Key Loan Approval

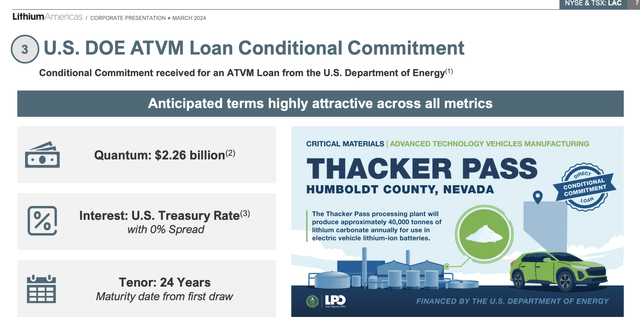

Lithium Americas spun off from Lithium Americas (Argentina) (LAAC) in order for the mine development project at Thacker Pass to obtain U.S. DOE funds and an investment from General Motors (GM). The company just announced the tentative approval of a $2.26 billion loan from the U.S. DOE Advanced Technology Vehicles Manufacturing program.

Source: Lithium Americas March ’24 presentation

Along with the GM investment, Lithium Americas will have the vast majority of the cash on hand in order to fund the projected capital spending to construct the Thacker Pass lithium mine. The estimated capital cost is now $2.93 billion, up from the original estimate of only $2.27 billion.

Along with the DOE loan, Lithium Americas should collect the Tranche 2 investment from GM of $320 million. In total, the company will collect $2.58 billion from these funding sources during the construction period.

Lithium Americas spent $194 million on mine construction during 2023. The company ended the year with a cash balance of more than $200 million, though the corporate update didn’t provide any financial details.

The loan will accrue interest at U.S. Treasury rates during the construction period, with an estimated cost of $290 million over the 3-year period. The goal remains to start lithium mining in 2027 with full capacity of 40,000 tonnes LCE achieved in 2028 about a year after mining starts.

Lithium Americas will still have the option of pursuing Phase 2 with another 40,000 tonnes LCE.

Lithium Prices

Despite Lithium Americas remaining on track with producing enough lithium to cover 800,000 EVs, the stock is now at the lows due to weak lithium demand. Lithium prices have fallen all the way to below $15,000 per ton.

The lower prices are causing high cost miners in China to close mines and cut back on new projects. These lepidolite mining projects in China have LCE production costs of 80,000 yuan ($11,120) to 120,000 yuan to process a ton of LCE, much higher than the Thacker Pass.

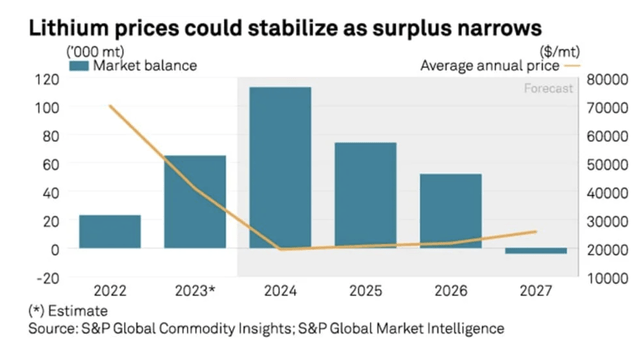

In the case of Lithium Americas, the real question is the price of lithium come 2027/28 when the Thacker Pass mine starts production. S&P Global estimates lithium prices start rising again in 2025 when any surplus narrows from the market with growing EV demand.

Source: S&P Global

The investment appeal is that a lot of the long-term demand drivers for lithium will be sorted out over the next few years. EV demand around the globe remains strong, and U.S. consumers will eventually become more comfortable with charging issues as EV charging stations expand.

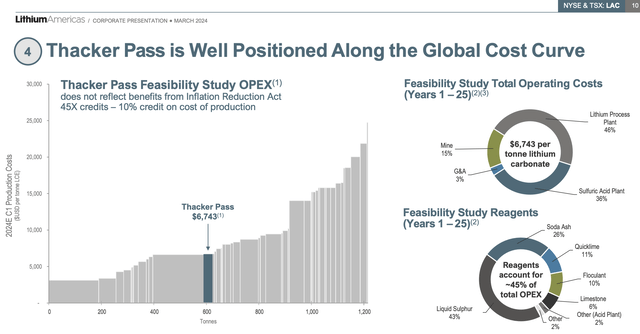

The great part of the Thacker Pass project is the total operating costs are in the mid-range of costs on the global cost curve. The Nevada mine is estimated to have a cost of only $6,743 per tonne LCE.

Source: Lithium America March ’24 presentation

The real question is how much cash flow can Lithium Americas generate with operating cost this low. The company forecasts $171 million in baseline EBITDA during Phase 1 from $12,000/LCE prices. Ultimately, though, $24,000/LCE prices (similar to S&P Global estimates) will produce $1.15 billion in annual EBITDA following completion of Phase 2 construction.

The stock has a market cap below $1 billion now for a company with the potential to generate annual adjusted EBITDA in excess of the market cap. Based on recent lithium prices and the potential for supply shortages towards the end of the decade when mining starts, Lithium Americas has the potential to produce adjusted EBITDA approaching $2 billion annually based on $36,000/LCE.

Takeaway

The key investor takeaway is that Lithium Americas is far more de-risked now with construction of the Thacker Pass under way and the DOE loan in hand. The major risk now is just market dynamics for lithium, which only appear to become more favorable as the new mine comes online in 3 years.

Investors probably shouldn’t chase the 10% rally in the stock today, but Lithium Americas Corp. is an attractive investment at the current valuation. Lithium prices will likely trade volatile over the next decade as demand and supply ebbs and flows, and investors should use weakness to invest in the long-term positive thesis.

Read the full article here