When investing in energy companies like Plains All American Pipeline (NASDAQ:PAA), the unit distributions — loosely called dividends — are a big deal. And it’s not just about investment returns. Here’s why.

With all these electric vehicles cruising the streets, oil’s golden years seem numbered. A long-term view might not feel urgent in 2024, but it’s important for investors living off dividends.

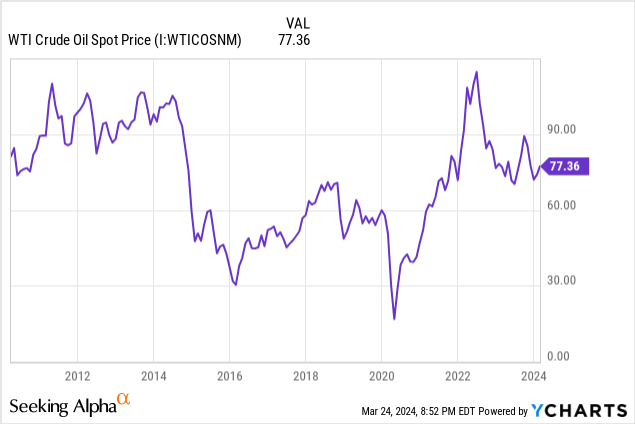

As I see it, crude oil demand will hold steady, increasing slightly throughout the next decade before it starts to fall. So, that’s ten years of crude oil running through PAA’s pipelines. But in these ten years, the way investors value the likes of PAA will take a hit in my view, as more people start imagining a future where a fixed number of pipelines compete for a shrinking oil market. Here’s my guess: PAA will be trading at a 5x PE ratio in ten years. That’s what happened to coal anyway, and why dividends are important. As the years pass, I think the chances of capital gains are slimmer.

PAA’s yield stands at 7.5% today, but for the past two years, the company has been boosting distributions. Last January, PAA hiked distributions by 19%. If this trend continues, you could potentially be getting back your initial capital in ten years. This is when I believe oil demand peaks, marking a perfect time to exit the pipeline market altogether. The bottom line is that with some planning, PAA can work well for “live-off-dividends” investors despite its challenges with the energy transition.

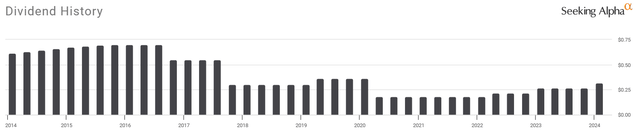

You might be thinking, ‘Can I really trust PAA to keep dividends steady after they’ve cut them in the past?’

PAA Distributions (Seeking Alpha)

In this piece, I argue that PAA today is not the same company it was in the past. After cleaning up their act, I see a compelling opportunity in the ticker. The company’s earnings and distributions seem more stable, and the low payout ratio increases the chances of further dividend hikes.

Pipeline Growth and Dividend Cuts

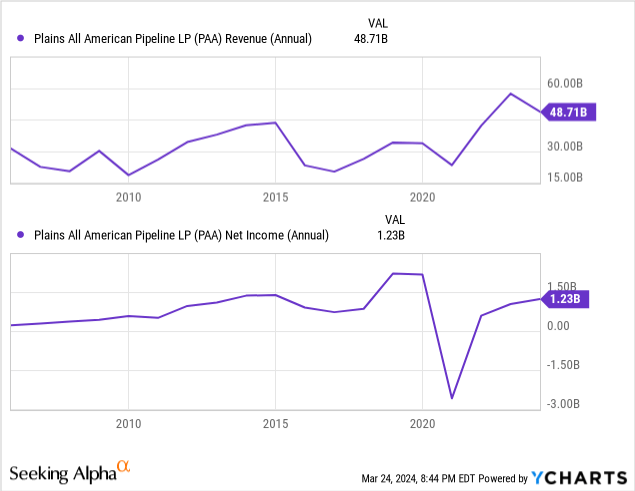

PAA’s revenue and net income charts make it look more risky than it really is in my opinion. The underlying demand for crude oil is much more stable than PAA’s financials suggest.

Data by YCharts

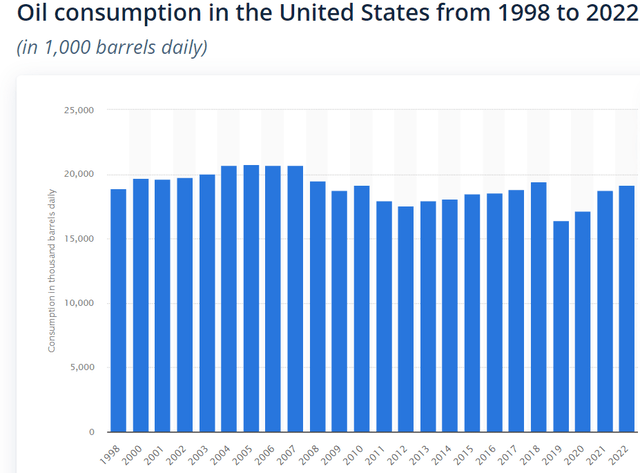

Even with a seismic disaster the size of the COVID-19 pandemic, consumption only declined 12% in the US. The impact of oil prices on demand is even smaller and more gradual. We’ve seen this between 2011 and 2014 when oil prices were flirting with the $100 mark. That’s $130 -$140 in today’s prices (calculated using FRED’s CPI data.)

Statista

There’s a good reason for this stubborn and invisible consumption floor. Oil plays a vital role in our everyday lives. We need it to travel, heat, and power our homes. We might drive less when gas prices are high, but we still drive to work, to the grocery store, and drive the kids to school.

Data by YCharts

So, the question is, how does a company in a stable industry show such volatility? Here’s why the three most followed financial accounts don’t represent PAA.

GAAP Revenue

PAA generates its income from transporting crude oil (and, to a lesser extent, NGLs) through its pipeline infrastructure, but in accounting terms, PAA makes money on the difference between buying oil and selling it after transport. That’s because of how its business contracts are written. Sales are calculated as crude oil volumes passing through its pipelines multiplied by oil prices. This means its revenue goes up and down with energy prices, but so do its costs, keeping profit margins steady.

Product sales revenues and purchases and related costs will fluctuate with market prices; however, the absolute margins related to those sales and purchases will not necessarily have a corresponding increase or decrease. Source: Page 71, PAA 10-K SEC Filing

EBITDA/Net Income

EBITDA includes many extras that don’t directly mirror PAA’s performance. For example, oil stuck in PAA’s pipelines (linefill) can fill 15 million barrels of crude oil (as noted on PAA 10-K, page 12), valued at billions. Oil price movements can bring big write-offs and gains in the books, but this doesn’t affect the day-to-day business since that oil stays in the pipelines as long as they’re running and are owned by PAA.

Adjusted EBITDA

Adjusted EBITDA filters out most of the noise to give a clearer picture of PAA’s performance. But historical EBITDA figures don’t give a good proxy of what to expect from PAA going forward.

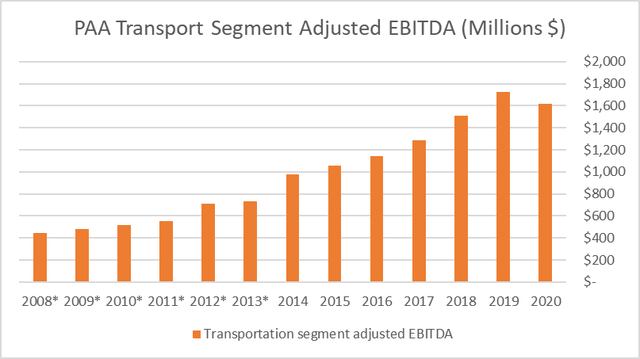

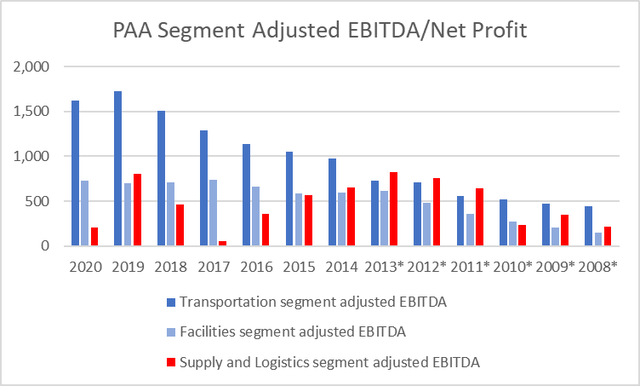

In the past, PAA made a lot of money from activities beyond transport and storage, which muddied the picture of its transport business.

By separating the transport-related earnings (Transport Adjusted EBITDA) up to 2021 (when PAA axed its non-transport/storage business), we get a stable earnings picture, matching the sector’s stability. Transport Adjusted EBITDA barely budged during the pandemic and was resilient during the 2015 shale bust and the 2007-2009 great recession.

It is worth noting that PAA changed the way it presents its earnings, and now its reports show only two segments; Crude Oil and Natural Gas Liquids.

Transport Segment Adjusted EBITDA (PAA, Author’s estimates)

PAA’s transport business benefits from long-term contracts that stabilize its earnings. The company owns thousands of miles of ‘gathering’ pipelines that collect oil from wellheads to its long-haul lines. These pipelines are built with specific customers in mind, who in turn dedicate millions of acres of oil-rich lands to PAA’s infrastructure

The table below shows PAA’s and its customers’ 2024 commitments to buy and sell crude oil, NGLs, and other products. This commitment represents roughly half of PAA’s 2023 purchase expenditure, highlighting a significant portion of their secured revenue.

PAA Crude, NGL, and other products Purchase Obligations (PAA)

Another source of stability is PAA’s customers’ Minimum Volume Commitments ‘MVC,’ where drillers guarantee a minimum amount of oil to be transported through PAA’s pipelines. While the dollar value of MVCs might be lower than the total oil purchase commitments, it represented the guaranteed net tariff income PAA expects from transporting the contracted amount of barrels. For example, PAA’s $609 million MVC this year is roughly 20% of 2023 Adjusted EBITDA.

Minimum Volume Commitments (PAA)

Here’s another reason why historical adjusted EBITDA is not a reliable proxy of what to expect from PAA going forward. During the shale boom, PAA ran on the idea: ‘if you build it, they will come,’ building pipelines for its customers to grow into. This mirrored a sense of partnership and confidence in the market. But after the shale bust, PAA found itself sitting on big but empty pipelines after its customers put the brakes on new drilling plans. Here’s how PAA’s CEO described the situation in 2020

For the last 10 years, the midstream segment really spent a lot of time focused on trying to stay ahead of our E&P and upstream brothers and sisters as far as production – Willie Chiang, PAA’s CEO, S&P Global

Data by YCharts

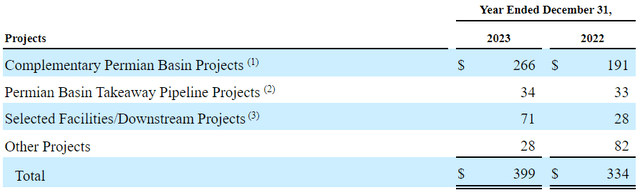

One might ask, ‘How do we know this won’t happen again? isn’t management building new pipelines?’ Well, most of the company’s new projects are in the Permian basin, where they’re building gathering pipelines with MVCs and other commitments.

Consolidated and Unconsolidated Investment Capital Projects (PAA )

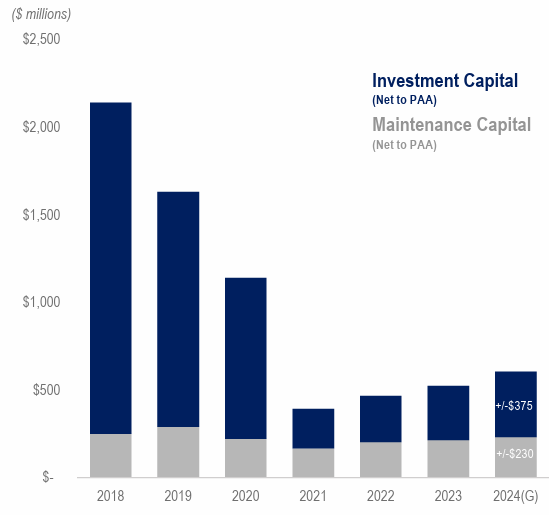

Also, these projects are too small to make a meaningful difference, even if they don’t perform well.

Last month, PAA’s CEO said that investors should expect $375 million in growth capex and $230 million in maintenance. That’s a bit higher than last year but still way lower than what we’ve seen in the past. These projects can easily be funded using cash on hand. So we don’t have to worry about dilution or debt.

The chart below gives a hint: the era of high-growth capex is over, and I think this makes distribution more stable.

Capital Expenditures (PAA)

Leverage and Dividend Cuts

PAA’s history of cutting payouts also ties back to how much debt it was carrying. They borrowed to fund pipeline projects that didn’t go as planned. Credit rating agencies weren’t happy with a debt pile without a corresponding increase in earnings. When Moody’s started calling their debt junk in 2017, PPA reduced the distribution, cutting it down to $0.3 per unit and redirecting its earnings to paying down debt.

PAA’s Unsecured Notes Rating History (Moody’s)

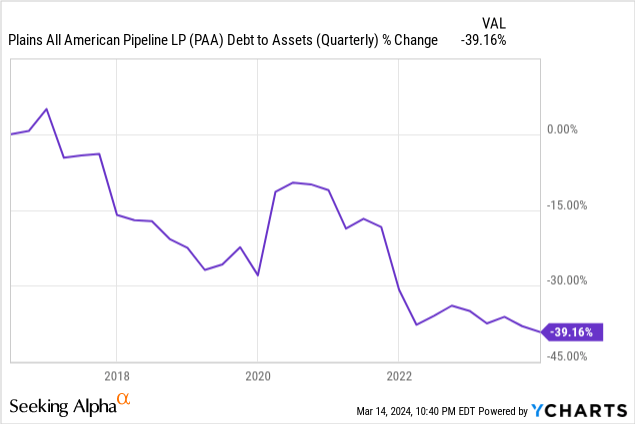

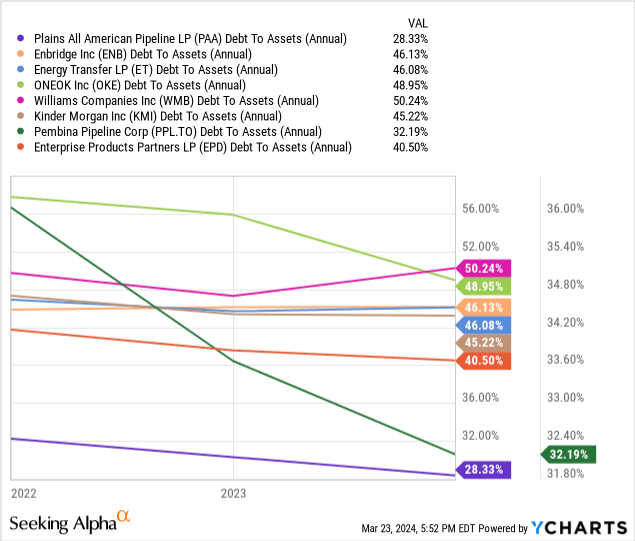

Today, things are different. PAA has an investment grade rating after reducing debt-to-assets by 40%. It now holds one of the lowest leverage ratios in the Midstream sector.

Data by YCharts

In November 2023, PAA promised to keep their debt between 3.25 and 3.75 times their Adjusted EBITDA. Credit rating agencies liked this move. By December 2023, Fitch raised PAA’s credit from BBB- to BBB, while Moody’s upgraded PAA’s outlook from Stable to Positive.

In 2023, PAA cut its debt by roughly $900 billion. Its leverage ratio is now below target, at 3.1x. The goal is complete, and we should see more cash going to unitholders instead of repaying debt.

We lowered our long-term leverage ratio target range to 3.25x to 3.75x and we ended 2023 with a leverage ratio of 3.1x. Willie Chiang, PAA’s CEO. Q4 2023 earnings call.

But this situation is also interesting because MLPs with leverage close to that of PAA have pretty good ratings. For example, Enterprise Products Partners (EPD) has a Moody’s rating of A3, multiple grades above that of PAA. I think MLPs with the same leverage should have the same credit rating. It makes sense to assume that rating agencies will increase PAA’s rating further. But what if this doesn’t happen? Wouldn’t that mean Moody’s thinks its business isn’t as good as EPD? I think so. So, this year will tell us a lot about PAA and how Wall Street institutions think about their assets and market position.

Rating

Leverage Target

Actual

Plains All American (PAA)

Baa3

3.25x – 3.75x

3.1x

Enbridge (ENB)

Baa1

4.5x – 5.0x

4.1x

Enterprise Products (EPD) ‘Op. LLC’

A3

2.75 – 3.25x

3x

ONEOK (OKE)

Baa2

3.5x

4

Energy Transfer (ET)

Baa3

4.0x – 4.5x

3.8

The good news is that PAA’s leverage is below its target range, so the days of cutting distribution to pay down debt are now behind us.

The Supply & Logistics Segment

PAA used to have a segment called’ Supply and Logistics’, whose primary role was to leverage PAA’s pipeline and storage assets to trade oil and Natural Gas Liquids ‘NGLs.’ For example, they traded oil between different regions; buying oil in low-price areas and selling it in States where the price was high, using pipelines, trucks, and rail for transport, profiting from base differentials.

PAA

At one point, the Supply & Logistics division was making a third of PAA’s income. Despite that, the segment’s income was unpredictable. It trended up and down, unlike income from Transport and Facilities/Storage services.

I’m not sure how much PAA is still into commodity trading or how much its dividends still depend on this revenue stream, but they did give the impression that they reduced their exposure.

When PAA first changed its reporting segments in February 2022, it alluded to ‘structural shifts’ in the market that made trading opportunities within the Supply & Logistics segment scarce. Unless these ‘structural changes’ have reversed in the past 24 months, I think it is safe to assume that PAA’s trading activities’ contribution to earnings is low.

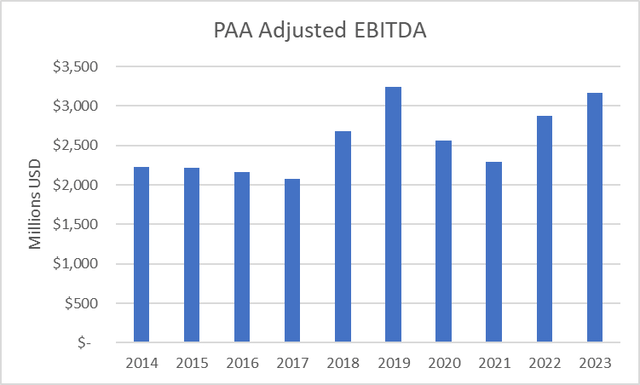

PAA’s Adjusted EBITDA (PAA. Author’s estimates)

Q4 Results

PAA’s Q4 earnings seem decent. Adjusted EBITDA was up 15% YoY in Q4. With the ‘bolt-on’ acquisitions, growth capex, and inflation price escalators, I think we should see similar growth in 2024.

Management also says oil production in the Permian basin is bound to increase. Last year, two-thirds of their total (consolidated & unconsolidated) growth capex went to projects in the Permian region. That was up from 58% in 2022. So, we should see the fruits of these efforts in the coming quarters.

Total Growth Capital Expenditures (PAA)

For the year, PAA generated $1.97 billion in Distributable Cash Flows ‘DCF,’ which measures cash generated, adjusted for maintenance capital. The company distributed $241 million to preferred unitholders and $748 to common unitholders, leaving $978 at the bank. It will likely use some of this money to fund its $375 million for growth projects and perhaps some more on ‘bolt-on’ acquisition opportunities. The thing is, DCF grew by 10% last year, and the payout ratio is already low (50%, including preferred distributions.) So, PAA can comfortably raise its dividends on top of the 19% hike earlier this year.

How I Might Be Wrong

I think the energy transition is the biggest risk to PAA. Our ‘Buy’ rating assumes that peak oil demand is still ten years ahead. But when I hear General Motors say that by 2035, they’d probably be 100% electric, our assumption seems less conservative than one might wish for.

Then you have PAA sitting on some really old pipelines, which are getting more rusty by the day. In 2015, one of these pipelines burst, causing a disaster. Replacing these pipelines, even if PAA wanted to, is really hard, not only because of cost and economic feasibility as we approach peak oil but also because of all the licenses PAA needs to undergo such a project. Enbridge faced a lot of resistance when it was replacing its Line 3 pipeline.

Summary and Final Thoughts

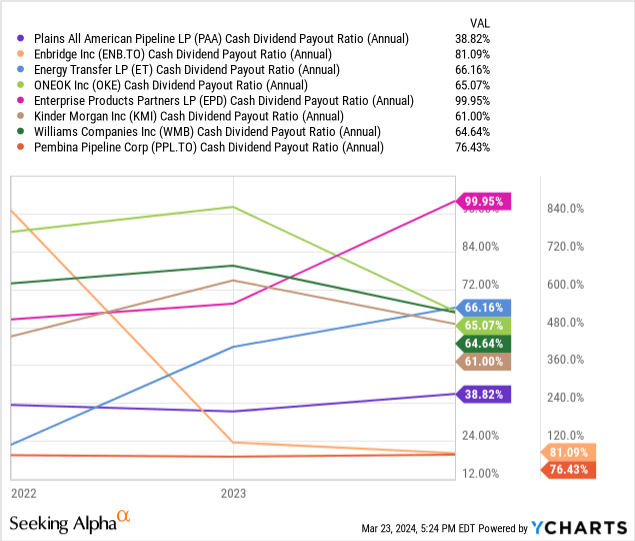

PAA’s distribution chart gives one the chills. But this is a story of a successful turnaround. Not only will the distribution likely stay stable, but it will most likely increase. Look at the chart below. Their cash payout ratio is the lowest in the sector. PAA already raised its distribution by 19% earlier this year, and I think this is just the start.

Data by YCharts

Then you have PAA’s solid balance sheet, holding one of the lowest leverage ratios in the sector, which earned them the approval of credit rating agencies. Again, they are at the bottom of the Debt-to-Asset ratio chart below.

Data by YCharts

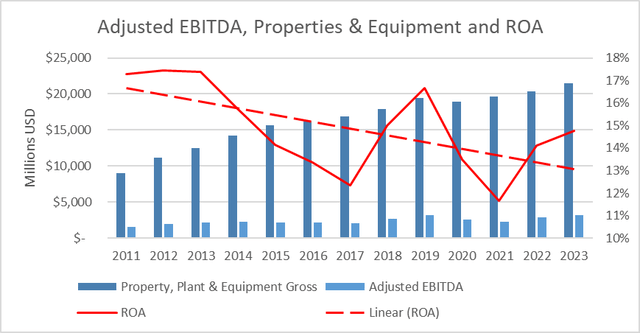

Then, they decreased reliance on trading revenue, shutting down the Supply and Logistics segment. Sure, their return on assets trended downwards (Adjusted EBITDA/Properties & Equipment). But with all the income stability this move brings, it is certainly worth it.