Stay informed with free updates

Simply sign up to the Sovereign bonds myFT Digest — delivered directly to your inbox.

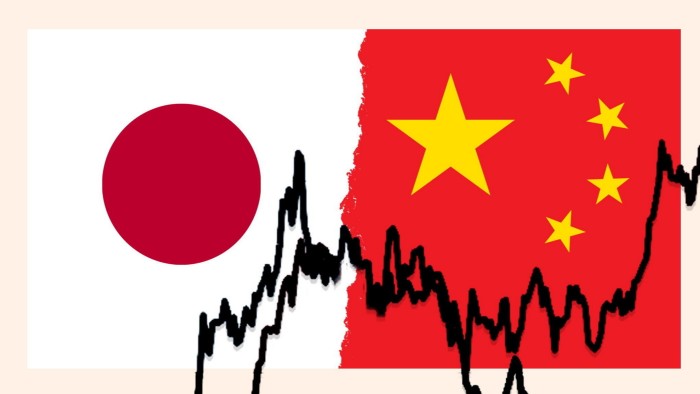

China’s long-term bond yields have fallen below Japan’s for the first time, as investors bet that the world’s second-biggest economy will become bogged down by the deflation that has long afflicted its neighbour.

A rally in 30-year Chinese government bonds has pushed their yield down from 4 per cent in late 2020 to 2.21 per cent on Friday, as Beijing cuts interest rates to boost its flagging economy and Chinese investors pile into haven assets.

Japan’s long-term bond yields, which for years were stuck below 1 per cent, have risen above China’s to 2.27 per cent, as Tokyo normalises monetary policy after decades of deflation.

The crossover in yields comes as Chinese authorities battle to try to support yields, warning that a sudden reversal in the market could threaten wider financial stability.

But some investors believe that deflation has become too entrenched in the Chinese economy to be easily fixed through fiscal and monetary policy, meaning yields still have further to fall.

“The inexorable direction of travel for Chinese government bonds is for yields to tick lower,” said John Woods, Asia chief investment officer at bank Lombard Odier, adding that he was “not entirely sure” how the authorities could hold back deflation.

“China is set to become — and possibly remain — a low-yield environment,” he said.

Some investors believe certain conditions in China’s economy echo those seen in Japan in the 1990s, when the bursting of a real estate bubble led to decades of stagnation.

Core inflation in China, excluding fuel and food, was running at an annual rate of 0.2 per cent in October. In Japan, core inflation hit a six-month high of 2.3 per cent, strengthening the case for further rate rises.

US president-elect Donald Trump’s promise to increase tariffs on Chinese exports to the US by 10 percentage points is also seen as a threat to growth.

China’s monetary policy was likely to “remain accommodative for some time to come”, said Zhenbo Hou, an emerging-market sovereign strategist at RBC BlueBay Asset Management, even if measures to boost the housing and stock markets provided a temporary fillip to yields.

“Nineties Japan remains the playbook,” he added.

Beijing has long fought against the “Japanification” of its economy, and has made huge investments in its high-tech, green and electric vehicle sectors with the goal of boosting long-term growth.

Authorities also recently intervened in its sovereign bond market to try to push up longer-dated bond yields and have warned local banks about a “bubble” in long-term debt that could lead to a liquidity crisis in the financial system.

“Some [Chinese] policymakers appear to view low long-term yields as a sign of low expectations for domestic growth and inflation expectations, and would like to push back against this pessimistic sentiment,” analysts at Goldman Sachs wrote in July.

But deflationary pressures have only intensified this year, with weakening economic data leading to calls for a big stimulus package to lift the economy.

Despite launching the biggest monetary stimulus since the Covid-19 pandemic and a Rmb10tn ($1.4tn) fiscal package, bond yields have continued to fall as domestic investors look for alternatives to China’s battered equity or property markets.

“It’s consistent with this new reality in global financial markets, due to US-China decoupling and China’s deflationary risk,” said Ju Wang, chief China FX and rates strategist at BNP Paribas. “The rest of the world is seeing an inflationary risk . . . and in China there is not enough demand for excess capacity.”

Many investors believe the government will need to do more to change the narrative in the bond market.

“It will be hard to escape deflation pressures unless consumption is boosted and investment is reduced,” said Andrew Pease, chief investment strategist at Russell Investments. “That’s a big policy shift for [Beijing].”

Read the full article here