Recap

We have covered SmileDirectClub (NASDAQ:SDC) since October of last year, and we have maintained a negative sentiment on the stock through the initial coverage article and the earnings update in January of this year. Our pessimistic outlook largely stems from the burn in cash flow and the meagre growth metrics that appear to endanger the company’s balance sheet as a consumer-led recession looms on the horizon. We will assess the company’s most recent earnings report this month, and re-evaluate our thesis to see if the company deserves another look by investors.

Q1 ’23 Update

Earnings Report

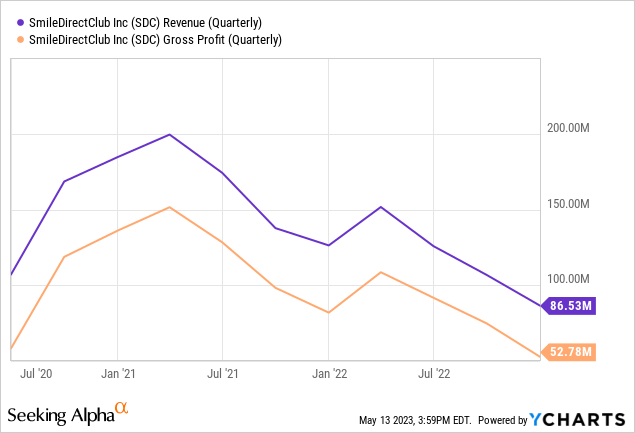

At a first look, the Q1 2023 financial results were positive, as the company reported a solid top line growth of 38.4% and a gross profit growth of 64.6% on a QoQ basis for the first quarter of 2023. Though these growth metrics sound robust, when actually looking at the reported revenues compared to a more seasonally adjusted YoY (year-over-year) metric, the results tell a whole different other story. The company reported $120 million in total revenues for Q1 2023, but in Q1 2022, the company reported more than $150 million in total revenues. Meanwhile, the company reported a $87 million gross profit in Q1 2023, but the company had a higher gross profit of $109 million in Q1 2022. In other words, on a YoY basis, the company’s top-line shrunk around 25% and gross profit declined by 20%. As seen in the chart below, the company’s financial results are nose-diving from its relative highs in 2021 on a quarterly basis. One positive from the financial results to note is that the management does appear to hold true to its efforts to cut costs, as the company’s SG&A and operating expenses both declined ~20% on a YoY basis.

YCharts

Management Discussion

Management has continued to emphasize its efforts to cut cost and deliver better margins in the most recent earnings call. Management also acknowledged the changing macroeconomic conditions and their impact on the business, which is in-line with our predictions set forth in our previous coverage articles. Specifically, the CFO Troy Crawford stated:

The year-over-year revenue decline was primarily driven by continued challenging macroeconomic conditions driven by high inflation, which has been particularly difficult for our current core customer.

This admission by the CFO further supports our thesis that the weakening consumer in the U.S. economy is likely to continue to translate to deteriorating financial performance of SDC. During the Q&A calls, management stated that the market is still “tough”, that the low unemployment hasn’t really helped, and that they don’t “plan for anything to improve dramatically in the back half”. These honest assessments of the economic realities and the exposure of the company to these very circumstances add to the uncertainties to the company’s viability in the near-term as it is unclear how worse the economy will get.

Balance Sheet and Shareholder Value

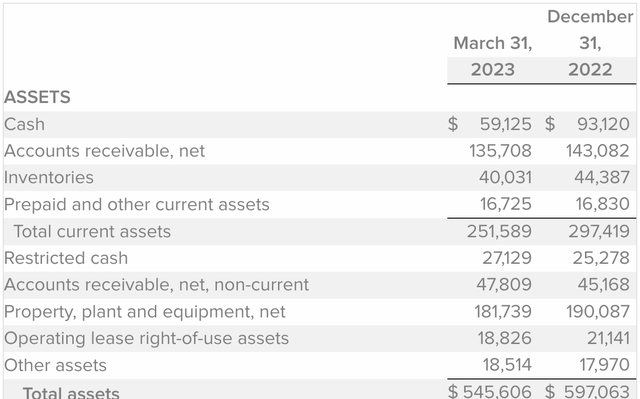

Our focus on this company largely centers around the weakening balance sheet and the risk-reward proposition that the company provides. We maintain the risk-reward is skewed to the downside even at these price levels as we believe that the economy is likely to get worse before it gets better. However, looking at the recent balance sheet, the company’s cash position has declined even further and at an alarming pace. $93 million in cash that the company held at the end of 2022 now stood at $59 million at the end of Q1 2023. Within a quarter, the company’s cash position declined by more than a third. At the same time of a weakening balance sheet, the company’s shares outstanding continues to rise, as the company’s weighted average shares outstanding increased by nearly 10 million over a quarter. Our bearish thesis continues to hold true as the company’s balance sheet deteriorates and as shareholder value continues to decline in a worsening macroeconomic environment.

Q1 2023 Balance Sheet

Risks to Thesis and Conclusion

We maintain our bearish outlook on SDC and we believe that investors should stay away as the risk/reward proposition continues to be skewed to the downside. There are some potential risks to the thesis, most notably a potential acquisition or merger announcement that could take the stock price higher in a short-term basis and if the economy were to bounce back quickly and consumption to rise to 2021 levels. Nevertheless, we believe these are unlikely scenarios due to the continued financial concerns in the banking sector, the lagging impact of the rate hikes, and the continued headline news of layoffs and decline in economic activity. In sum, there are too many uncertainties surrounding the economy and the company’s deteriorating financial position does not lend confidence at the current time. We maintain our “Strong Sell” rating in light of the Q1 2023 earnings report.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here