A growing chorus is writing about the challenges to the U.S. dollar’s (USD) role as the world’s global reserve currency. The debate about the dollar’s demise is not new and reminds me of the Mark Twain quip that “the reports of my death are greatly exaggerated.” We have seen this movie before. In 2010, the Federal Reserve Bank of New York (N.Y. Fed) published a note that, at the time, was in response to a growing view questioning the sustainability of the USD as the reserve currency, like today. The N.Y. Fed wrote1:

Recently the U.S. dollar’s preeminence as an international currency has been questioned. The emergence of the euro, changes in the dollar’s value, and the financial market crisis have, in the view of many commentators, posed a significant challenge to the currency’s long-standing position in world markets.

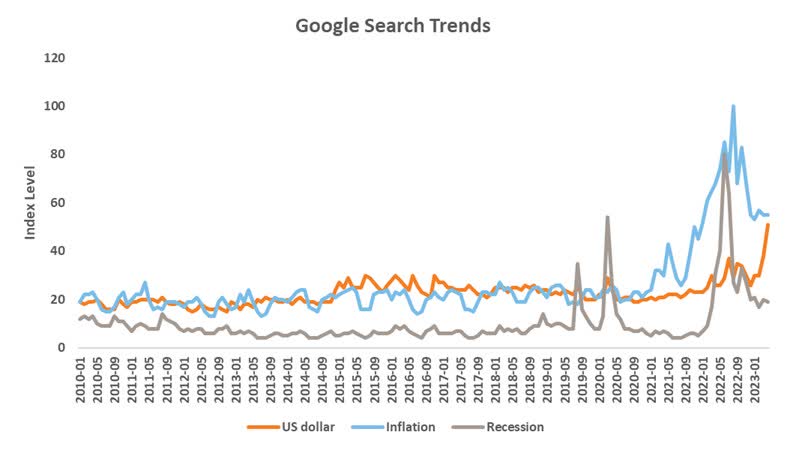

While the objections are more nuanced this time, the big difference is that the rise of social media means news travels faster, and narratives can perpetuate more easily. Indeed, based on Google Trends, searches for the “US dollar” have surged, surpassing inquiries related to inflation and recession. So why is there so much interest in the dollar now?

Chart 1

Source: Google Trends. As of April 2023.

A view gaining momentum centers around the challenge from China and other nations seeking to diversify their USD holdings and be less dependent on it for trade. There is increasing interest in establishing currency blocs that facilitate trade and commerce in respective local currencies to reduce their dependence on the U.S. dollar as the medium of exchange.2 Some of this is understandable, especially for many emerging economies. Swings in U.S. central bank policy can cause broad shifts in the USD. Based on Financial Stability Board3 data, roughly two-thirds of emerging economies’ external debt is denominated in the USD.

Therefore, in times of economic uncertainty and financial market volatility, the dollar strengthens due to its safe-haven appeal, raising the cost of financing dollar-denominated debt at the worst time. Moreover, reducing its dependence on the USD is a priority for a rising nation like China vying to exert more significant global influence. At the same time, some argue that the dollar’s centrality to international commerce allows the U.S. to use it as a weapon in the form of sanctions for geopolitical objectives. Whatever the cause, the de-dollarization narrative is gaining traction.

Historical perspective

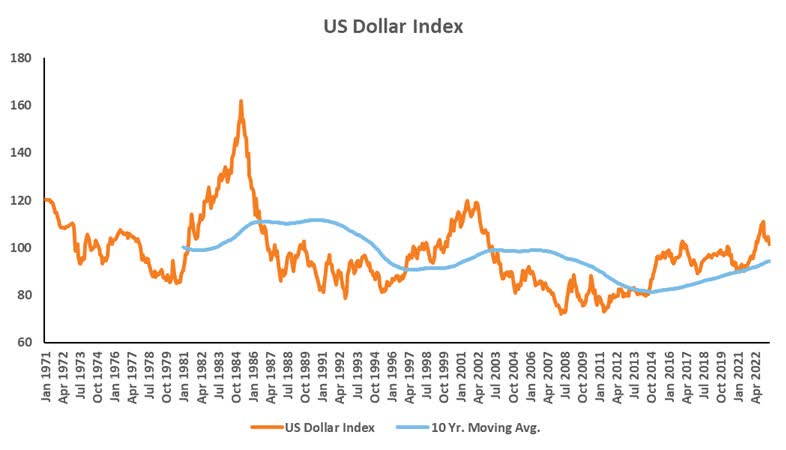

Like other asset classes, the USD is influenced by evolving macroeconomic and financial market conditions. Chart 2 shows the U.S. dollar tends to maintain a trend for several years, rising above and below the long-term 10-year average trendline. Over the most recent 10-year period, the dollar has strengthened, benefiting from aggressive interest rate hikes by the U.S. Federal Reserve (Fed) and more favorable economic growth than other developed economies.

While the dollar may find support in a recessionary environment, the Fed did not pre-commit to additional hikes at its rate-setting meeting in May. This takes away a potent force that previously supported the USD. Put differently, the dollar may be transitioning, once again, from a multi-year period of strength to a multi-year period of weakness. That weakness, however, shouldn’t be misread as a signal for its structural downfall. Instead, it reflects the natural reaction to evolving economic conditions.

Chart 2

Source: Refinitiv DataStream. As of April 2023. The Dollar Index is a weighted aggregate measure of nominal exchange rates of US dollar against major developed market currencies, such as the euro, Japanese yen, Canadian dollar, British pound, Swedish krona, and Swiss franc.

Evolution of the USD’s share of foreign exchange reserves

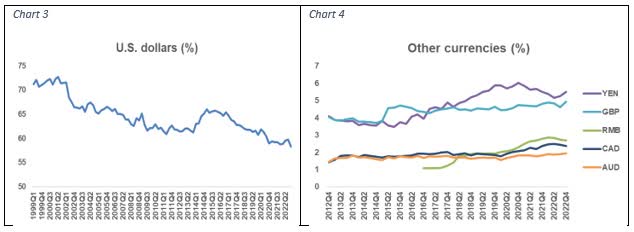

The US dollar’s ascent to global reserve currency status commenced after WWII. Its share of global foreign exchange (FX) reserves reached a high of 72% in 2001 and has declined to just under 60% as of Q4 2022, shown in Chart 3. Therefore, while the de-dollarization narrative is in today’s news cycle, it’s been occurring in the background for almost two decades as a broader effort by global central banks to diversify their foreign exchange reserves.

For instance, over the last decade, the basket of currencies central banks has increased their holdings of includes currencies of smaller open economies like Canada (CAD) and Australia (AUD). Their share of global reserve assets, interestingly, are around 2% and not too dissimilar to the Chinese renminbi’s (RMB) share. The renminbi received a boost since its inclusion into the basket of currencies in the International Monetary Fund (IMF)’s Special Drawing Rights4 in 2015, growing the RMB’s share of global FX reserves from around 1% to 2.7%. Moreover, China is the world’s second-largest economy, and its trend growth, albeit slowing, is higher than the U.S. Therefore, the renminbi’s share of global FX may continue to increase, but 2.7% is very different from the USD’s almost 58% share of global FX reserves.

World Currency Composition of Official Foreign Exchange Reserves

Source: Currency Composition of Official Foreign Exchange Reserves (COFER), International Financial Statistics (IFS); Data extracted from http://data.imf.org/.

The dollar’s role in global finance

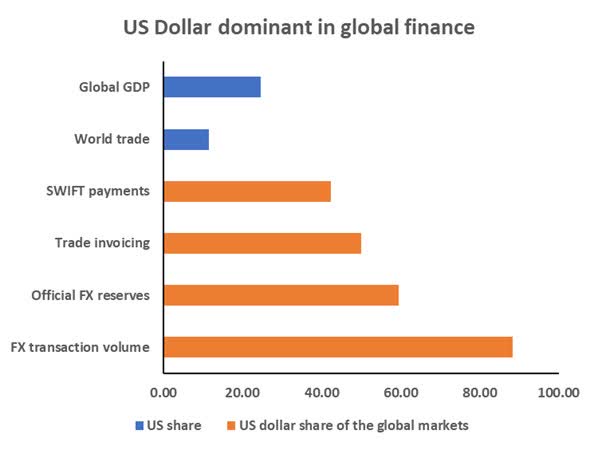

Despite the decline in the dollar’s share of official FX reserves, it remains central to international finance. Chart 5 shows that the USD punches above its weight. Although it represents about 25% of global GDP and 12% of global trade, the USD’s share of global markets is significantly more. For instance, the USD is involved in almost 90% of FX transaction volumes5, 50% of trade invoicing, and 42% of SWIFT payments. Despite a gradually declining share of global FX reserves, it will likely remain the primary medium for international commerce.

Chart 5

Source: BIS Quarterly Review, December 2022.

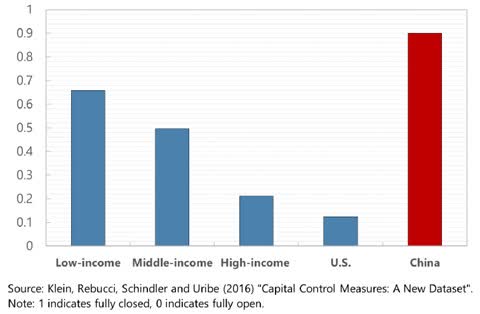

As highlighted in Chart 4, China’s share of global FX reserves is rising from a shallow base. However, a limiting factor for substantive internationalization of the RMB is that China mostly runs a closed capital account that restricts the flow of capital into and out of the country. A recent IMF working paper scored China’s capital account openness worse than even low-income economies. In contrast, the U.S. scores better than the average of high-income economies. This is illustrated in Chart 6. Succinctly, a restricted capital account slows the pace of internationalization. Still, China’s growing share of global GDP (gross domestic product) and increasing use of agreements between nations to settle trade in the RMB6 means its prominence will continue to increase gradually. However, talks of the renminbi de-throning the USD as the global hegemon may be premature.

Chart 6: Index of capital controls

Additional source: IMF working paper, March 2023.

How does gold fit into this conversation?

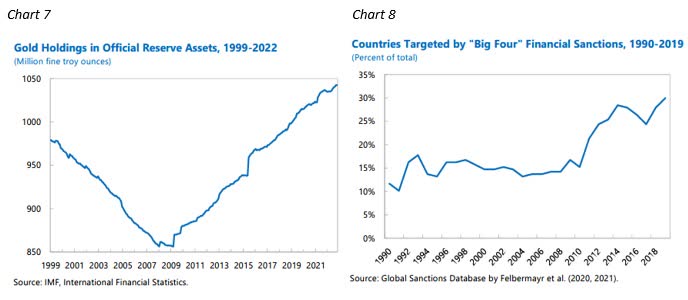

Chart 4, above, which shows how central banks are diversifying their FX reserves, doesn’t include gold. Even though gold is no longer a currency in a traditional context, its use as a store of value and a medium of exchange over the millennia makes it a core reserve asset. Chart 7, taken from a recent IMF working paper, illustrates that gold holdings in official reserve assets steadily rose after the Global Financial Crisis of 2008/09. Interest in gold as a reserve asset has grown as more stories circulate about the U.S. weaponizing the dollar by using sanctions.7

There may be something to that narrative. Chart 8 shows that coincidentally, countries targeted by sanctions from the Big Four nations have been increasing their share of gold as a reserve asset since 2010. The countries that have contributed the most to this increase are Russia and China. However, other emerging economies, like India and Turkey, have also been increasing their share of gold reserves.

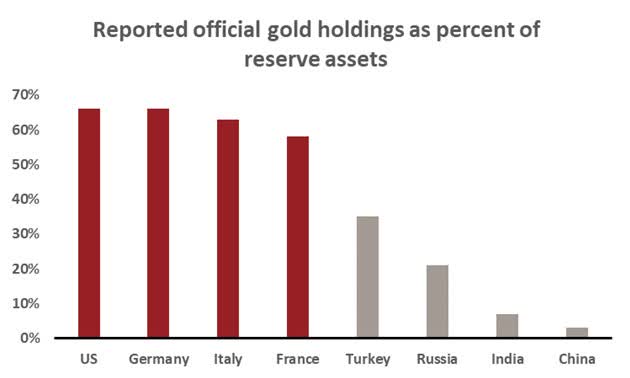

It’s worth noting that emerging economies like Russia and China have a much smaller allocation to gold as a percent of their reserve assets versus advanced economies like the U.S. and Germany, as shown in Chart 9. Therefore, while sanctions may be a contributing factor, the more significant takeaway is that a rising allocation to gold is part of the broader trend of diversifying reserve assets, along with allocating to the AUD, CAD, and RMB.

Source: IMF, Gold as International Reserves: A Barbarous Relic No More?, 2023. Big Four refers to the US, EU, UK or Japan.

Source: IMF, Gold as International Reserves: A Barbarous Relic No More?, 2023. Data based allocation at end-2021. Big Four refers to the US, EU, UK and Japan.

Keeping perspective

It’s important to keep perspective but also appreciate developing trends. The US dollar is the global reserve currency today and may continue for many years or decades. But nothing is forever. Before the U.S. dollar, it was Great Britain’s pound sterling as the global reserve currency. Before the sterling, it was the French franc. Before the franc, it was the Dutch guilder, and so on. As discussed above, a broader effort is underway to diversify global reserves away from the USD, whether by increasing exposure to currencies like the AUD, CAD, or RMB or expanding a nation’s gold holding. However, and crucially, Chart 5 illustrates that the USD dominates global finance activities. Therefore, while it is reasonable to assume that the USD may gradually lose its preeminence, it will likely remain one of the dominant currencies for some time.

1 https://www.newyorkfed.org/medialibrary/media/research/current_issues/ci16-1.pdf

2 https://www.theglobeandmail.com/world/article-brics-expansion-membership/

3 Financial Stability Board, April 2022. Statistic indicated does not include China.

4 Special drawing rights (SDR) are international reserve assets created by the IMF and are based on a basket of five currencies: USD, EUR, JPY, GBP and RMB.

5 As two currencies are involved in each transaction, the sum of shares in individual currencies will total 200%

6 China’s small steps on offshore use of yuan are starting to add up

7 https://www.bloomberg.com/opinion/articles/2018-09-06/how-the-u-s-has-made-a-weapon-of-the-dollar?sref=2I7V236A

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This material is not an offer, solicitation or recommendation to purchase any security.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment. The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the “FTSE RUSSELL” brand.

The Russell logo is a trademark and service mark of Russell Investments.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

UNI-12238

Original Post

Read the full article here