Investment Thesis

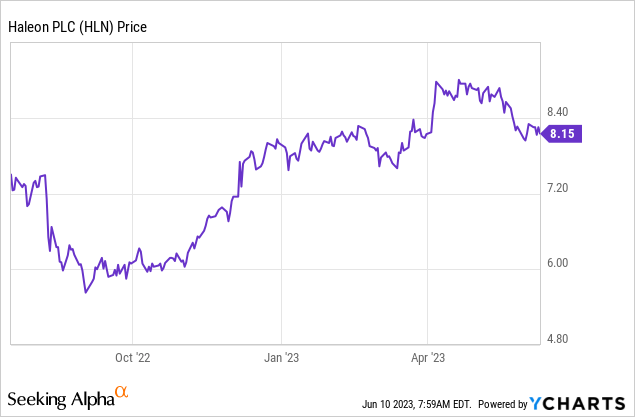

Haleon (NYSE:HLN) was spun off from GSK (GSK) in July last year and its stock price has performed very well after the initial dip in August amid the Zantac litigation. While the company is still relatively new and has little following, it is actually a leader in multiple consumer health markets.

The company has a strong moat thanks to its portfolio of leading brands and should continue to benefit from ongoing market expansions. The latest earnings were also strong with double-digit growth in both the top and the bottom line. Despite the solid fundamentals and growth, its valuation remains meaningfully discounted compared to peers. I believe the current price is compelling therefore I rate the company as a buy.

Strong Portfolio Of Brands

Haleon is a Brentford-based global consumer healthcare company recently spun off from GSK, with a primary focus on oral health, VMS (vitamins, minerals, and supplements), pain relief, respiratory health, and digestive health & others. The company has a strong portfolio of leading brands including Advil, Panadol, Sensodyne, and Voltaren. Thanks to these popular brands, it currently has a leading market share in 4 out of its 5 segments.

The strong branding and penetration give the company a formidable moat as customers are often reluctant to switch brands after they get comfortable with one, especially for health-related products. The stickiness of these products subsequently translates to much better pricing power as well, which helps the company steadily grow at above-market rates.

Haleon

Huge Market Opportunities

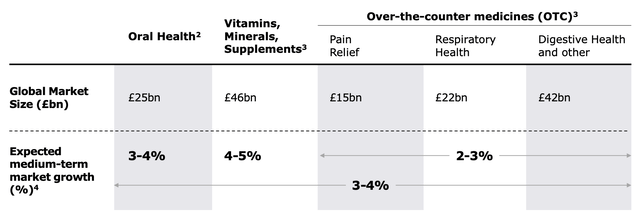

Considering the company’s leading portfolio and market position, it should be well-positioned to benefit from its large and expanding TAM (total addressable market). According to the company, the 5 segments combined present a TAM of £150 billion that is estimated to grow at a CAGR (compounded annual growth rate) of 3.5% in the medium term. Allied Market Research is even more optimistic and expects the market to reach $574.4 billion by 2032.

The market expansion should be very durable due to the aging population and increasing health awareness. For instance, the percentage of the world’s population over 60 years old is expected to grow from 12% in 2015 to 22% in 2050, according to the World Health Organization. Health awareness is also on the rise due to the outbreak of the pandemic in 2020. These catalysts should continue to help drive the demand for consumer health products.

Haleon

Solid Financials

Haleon announced its first-quarter earnings last month and the results are very solid considering the current macro backdrop. The company reported revenue of £2.99 billion, up 13.7% YoY (year over year) compared to £2.63 billion.

Organic revenue growth was 9.9%. The growth was driven by a 2.8% increase in volume and a 7.1% increase in pricing. The respiratory health segment was extremely strong amid the increase in cold and flu cases, with revenue up 39% from £367 million to £510 million. The pain relief segment also saw upbeat traction, with revenue up 14% from £635 million to £724 million.

The bottom line was also strong thanks to favorable price mix and lowered spending. Gross profit increased 14.3% YoY from £1.61 billion to £1.84 billion. The gross profit margin expanded 20 basis points from 61.4% to 61.6%. SG&A (selling, general, and administration) expenses as a percentage of revenue declined 330 basis points from 41.3% to 38%, as the company benefited from better operating leverage.

This resulted in the operating income up 34.5% YoY from £466 million to £627 million. The operating margin also increased 330 basis points from 17.7% to 21%. The diluted EPS was £4.2 compared to £3.7, up 13.5% YoY.

Discounted Valuation

Despite the rise in share price in the past few months, Haleon still looks attractively priced. The company is currently trading at a fwd PE ratio of 17.9x, which is more than justified in my opinion.

For instance, the multiple is lower than other notable consumer healthcare companies such as Kenvue (KVUE), Colgate-Palmolive (CL), and Procter & Gamble (PG). The peer group has an average fwd PE ratio of 23.1x, which represents a meaningful premium of 29.1%. Haleon’s latest revenue growth of 13.7% also vastly outpaced peers, which reported growth of roughly mid to high single digits. The sizeable valuation gap seems unjustified and I believe the company’s valuation should eventually catch up to peers.

Investors Takeaway

I believe Haleon has the potential to become a great compounder. Its strong portfolio of leading brands alongside the organic market expansion should drive durable and consistent growth in the long run. The company should also demonstrate great resiliency as most of its products are non-discretionary. This is important in the near term as the economy continues to slow down amid the rise in interest rates. While the company has strong fundamentals and growth, its current valuation remains meaningfully below peers.

There is risk regarding the litigation with Zantac but I am not concerned as GSK is the only defendant in the July trial and the company stated that they have never marketed the product. There should be ample upside potential if the company can catch up on valuation therefore I rate it as a buy.

Read the full article here