High Voltage Electric Power Lines At Sunset

Introduction

NRG Energy (NYSE:NRG) is a mid-cap utility company specializing in retail electricity and natural gas sales. They power homes, businesses, and industrial sites across the U.S. and Canada. Besides energy sales, NRG is also involved in wholesale power generation (i.e., fossil fuel, nuclear, renewable) and other adjacent services. In this article, we’ll explore the investment opportunity at NRG, in light of recent developments from activist investors.

My outlook for NRG is moderately bullish. I believe that their cheap valuation limits downside risk for investors. In terms of strategy, I think that there is substantial upside if NRG can successfully spin off Vivint. Management’s claims about synergies from the deal appear quite flimsy to me. Regardless, company leadership has minimal experience in the home services market and previous failures should’ve been paid more attention to. Elliott’s active involvement could also serve as a catalyst for share price appreciation.

Background

As an integrated energy and utility provider, NRG’s core business is remarkably solid. From energy generation to distribution and sales, the company has previously demonstrated the ability to deliver strong returns to shareholders. However, NRG’s has lagged behind its peers in recent years due to operational and strategic mistakes.

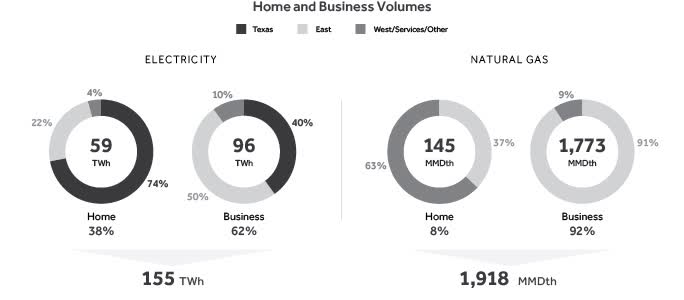

By segment, the vast majority of NRG’s revenue comes from retail energy sales, accounting for $29.7 billion out of $31.5 billion total. By geography, the East market accounts for the largest portion of total revenue, but the Texas market is actually the most profitable one for NRG by gross margins. This is likely due to the fact that NRG has generation facilities within Texas, enabling it to drastically reduce costs for energy purchases.

Some of NRG’s peers include OGE Energy (OGE), Pinnacle West (PNW), and Portland General Electric (POR). All these firms are mid-cap electric utilities, each focused on different geographic markets. Bigger players in the space include NextEra and Duke Energy, but those firms aren’t quite comparable due to the greater scale and complexity of their operations.

NRG’s customer base skews more towards businesses than consumers, perhaps making it more vulnerable to cyclical changes in the economy:

NRG’s Latest 10K

Strategy

The best way to describe NRG’s strategy is directly from management, “NRG’s strategy is to maximize stakeholder value through the safe production and sale of reliable electricity and natural gas to its customers in the markets it serves, while positioning the Company to provide innovative solutions to the end-use energy or service customer.”

For context, here are comparable statements made by the company’s peers:

- “Our strategy is to deliver shareholder value by creating a sustainable energy future for Arizona by serving our customers with clean, reliable, and affordable energy.” (Pinnacle West)

- “OGE Energy’s purpose is to energize life, providing life-sustaining and life-enhancing products and services, while honoring its commitment to strengthen communities. Its business model is centered around growth and sustainability for employees (internally referred to as “members”), communities and customers and the owners of OGE Energy, its shareholders.” (OGE Energy)

- “The Company exists to power the advancement of society. PGE energizes lives, strengthens communities, and fosters energy solutions that promote social, economic, and environmental progress. The Company is committed to being a clean energy leader and delivering steady growth and returns to shareholders.” (Portland General Electric)

While NRG’s strategy statement isn’t as fluffy as OGE’s or POR’s, it’s important to identify the key elements so we can better understand their approach:

- NRG takes a stakeholder-oriented view

- It is focusing primarily on the production and sale of electricity and natural gas

- It is looking to provide additional related services to its customers

We can also note what NRG didn’t state:

- It isn’t targeting any single geography

- It isn’t solely focused on generation via solar, wind, nuclear, etc.

What this means for investors is that NRG is essentially a bet on vertical integration in electric utilities for businesses. Current leadership wants to expand along the value chain from production to sales to add-on services.

As part of this strategy, NRG acquired Vivint Smart Home for $2.8 billion in December 2022. Vivint’s smart home products help clients with security, fire detection, and home automation. The primary rationale for the deal is that NRG and Vivint both target the same customers, so the combined firms may benefit from cross-selling and more efficient customer acquisition. Furthermore, NRG may be able to improve its core services by integrating data from Vivint’s suite of smart devices, potentially improving customer experience.

I think that this strategy is fundamentally flawed because smart home services are not closely related to the power business. If NRG was acquiring a company that built electric charging stations, then I could see some clear synergies. But the only overlap I could find in the company’s announcement is that households could benefit from automatically-adjusting thermostats. It remains unclear to me why a utility provider would even need to be involved in order for a smart home system to build such a feature. In the worst case, NRG could have simply partnered with Vivint, rather than spending billions of dollars to acquire them outright. But even if we accept management’s vision for a moment, how would these changes affect NRG’s top or bottom line performance?

A second stated benefit from the acquisition is the potential for “unmatched data and insights”, but there is no mention of what the new data could actually be useful for. In the case of autonomous vehicles, it’s plain to see that new data can directly improve the performance of the self-driving software. The ultimate purpose of that data is already clear. But in this case, there’s no obvious benefit or use case for this data, insofar as NRG’s utility business is concerned. If management actually does have a plan for how they’ll use this new data, then why have they failed to communicate it?

The Current Situation

In recent months, institutional investors like Elliott Management have publicly railed against deficiencies in NRG’s strategy and execution. Elliott, which currently manages about $55 billion in assets, is a hedge fund focused on unlocking value through shareholder activism. In particular, Elliott has criticized NRG’s recent acquisition of Vivint, and is again pushing for changes to leadership, operations, and strategy. Elliott’s current stake in NRG is reportedly around $1 billion, or 13% of the outstanding shares. Their plan involves:

-

Appointing a new CEO and new directors with relevant industry experience

-

Reviewing the Vivint transaction and consider new options

-

Improving operating efficiency by working on reliability and cost savings

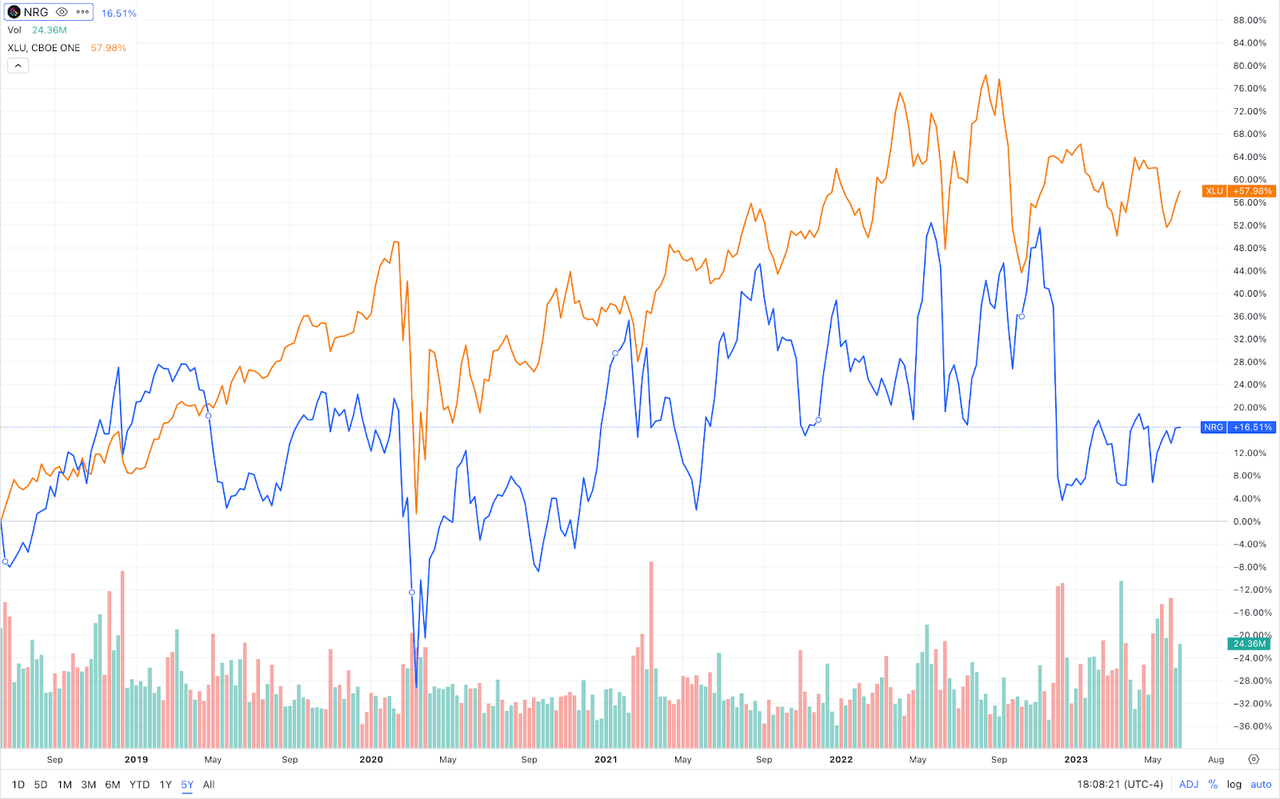

Elliott has a bone to pick with NRG, and it shouldn’t come as much of a surprise. Back in 2017, the firm had amassed a ~7% stake and demanded improvements in the company’s operations and efficiency. They eventually settled with the board and replaced a couple directors, leading to a boost in profitability and shareholder returns. Unfortunately, NRG’s performance didn’t maintain its momentum for very long. Over the past five years, returns have been subpar:

Seeking Alpha Price Chart Comparison

Total shareholder returns for NRG have lagged the industry benchmark, coming in at a meager 16%, versus 58% for the index (NYSE:XLU). To be fair, a good deal of this underperformance can be attributed to the wake of the Vivint acquisition. However, the company must soon demonstrate strong growth if they are to maintain investor confidence in their vision.

Investors have also pointed out that NRG’s operational execution has been weak, with significant disruptions resulting from weather-related outages. In 2021 and 2022, four major events negatively impacted results:

Some SA analysts were more optimistic about the NRG-Vivint deal at the time, but I’d be curious to get their thoughts as we approach the one-year anniversary later this year. Elliott highlighted several flaws to the Vivint acquisition:

-

NRG’s previous failure in home services

-

Various other power, telecom, and cable companies have entered and left the home security market with minimal success

-

Vivint’s geographic overlap and sales proposition do not actually align with NRG’s (this especially makes sense considering that Vivint primarily offers consumer products while NRG’s sales mostly go to businesses)

-

Investor sentiment following the deal has remained poor

They also argue that the Vivint acquisition will effectively cost NRG something on the order of $6 billion, rather than the company’s stated figure of $2.8 billion. The $6 billion tag includes costs related to financing and execution, some of which the company did note (but didn’t highlight) in its original announcement.

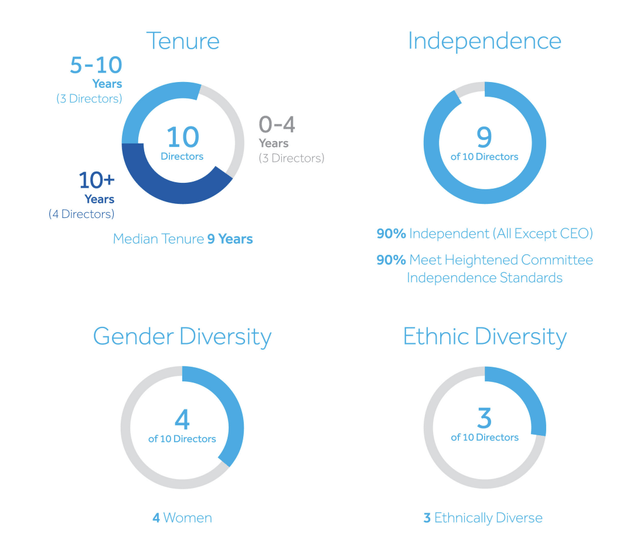

NRG just had its annual shareholder meeting this past April, so their next AGM won’t come for another 9 months or so. However, changes could materialize sooner if Elliott garners the support of other investors and approaches the board in the meantime. It’s not clear to me who on NRG’s board would be replaced in a potential proxy fight, particularly given that all directors (except the CEO) are already independent:

NRG’s 2023 Proxy Statement

Elliott is poised to pursue a proxy fight with NRG’s board and may consider taking matters to the voting markets if they want to. They noted that they have already identified 5 individuals who they deem to be qualified to serve on NRG’s board. The situation has ratcheted up in recent days, with Elliott now calling for the removal of NRG’s CEO. The company responded with an announcement of a $2.7 billion share buyback plan, which handily surpasses its previous $1 billion program. The company also said that it’s considering refreshing its board.

These escalations are classic signs of an emerging proxy fight:

-

the activist states its plans (which threaten incumbent leaders),

-

management attempts to curry favor via buybacks/dividends,

-

and now the activist must decide whether or not there remains enough upside to justify a proxy contest.

It seems all but certain that Elliott will go the distance in this case, given that Elliott published a new letter today stating that, “Elliott believes there is a readily actionable path to create more than $5 billion of value at NRG; however, it is clear that the realization of this value will require management and Board changes.”

This development is a win-win for shareholders, which is likely why the stock rose 1.89% for the day (June 27, 2023). If Elliott wins out, then their plan is probably going to be a positive catalyst, and if management wants to win then they’ll need to make more concessions. Either way, some kind of change is already happening at NRG, and the question now is a matter of just how much.

Financial Analysis

Looking over the past 10 years or so, NRG’s bottom-line results have been far worse than peers. In fact, if you add up the company’s Net Income over the past decade, you’d find that they’ve actually lost money in aggregate. Beyond the cumulative total, NRG has reported negative net income in 5 of the past 11 reporting periods, making for high volatility in what’s supposed to be a relatively stable industry (utilities):

NRG Cash Flow (Seeking Alpha)

This level of variability is not to be found in any of NRG’s peers (OGE, PNW, and POR). Of all three competitors, only OGE has reported an annual loss in the past decade. Even still, the loss only occurred once and was relatively small. NRG’s profitability is abysmal. Do not be deceived by SA’s Quant rating system, which places NRG at a “D” and POR” at a “D+”. The disparity in the actual financial metrics is far worse than it might seem at the surface:

|

Gross Profit Margin (TTM) |

Net Income Margin (TTM) |

Return on Total Assets (TTM) |

|

|

NRG |

0.24% |

-5.90% |

-6.23% |

|

OGE |

36.47% |

12.70% |

3.32% |

|

PNW |

38.09% |

10.33% |

1.96% |

|

POR |

47.96% |

8.92% |

2.43% |

As things stand at the moment, NRG is a pure value play. Across a host of valuation measures, the company bests its peers in this regard:

|

P/E Non-GAAP |

EV/Sales (TTM) |

Price/Sales (TTM) |

|

|

NRG |

5.3 |

0.7 |

0.3 |

|

OGE |

18.2 |

3.6 |

2.2 |

|

PNW |

20.2 |

4.3 |

2.1 |

|

POR |

17.9 |

3.1 |

1.6 |

If NRG’s valuation multiples were to move in line with their competitors’, then the stock could see significant upside (north of 100%). However, such a sharp move is unlikely in the near term and market sentiment will need time to adjust. The company would probably need to deliver consistent results for 3-5 years before such a turnaround in sentiment could be achieved.

The utility sector is by no means a growth market, but companies are expected to provide safety and stability to investors (as well as to consumers). NRG’s cheap valuation, combined with poor financial performance, makes it an attractive candidate for investor activism. I would attribute the majority of the company’s problems to some combination of bad management, operations, and strategy. If Elliott can successfully clean up the problems at the firm, they may be able to unlock significant value and create long-lasting growth.

Risks

My primary concern with NRG right now is that even if Elliott is eventually successful in its bid, it may take too long to deliver results. I’m not proactively looking to make a quick buck in the next 3 months, but I would like my capital to be deployed in opportunities that are actively materializing. I don’t exactly want to wait around for some convoluted turnaround plan that’ll take 5 years.

As a caveat to this concern, I actually think that the plan here is fairly straightforward and can deliver immediate results once put in motion. In particular, if the company sells off the Vivint assets, then shareholders should see short-term gains. Furthermore, if incumbent leadership can be replaced with individuals who have better operating experience, then investor sentiment for the company may begin to improve. A clear announcement in a strategic shift wouldn’t hurt either, as that would let the markets know that NRG is no longer seeking to make unprofitable or irrelevant acquisitions.

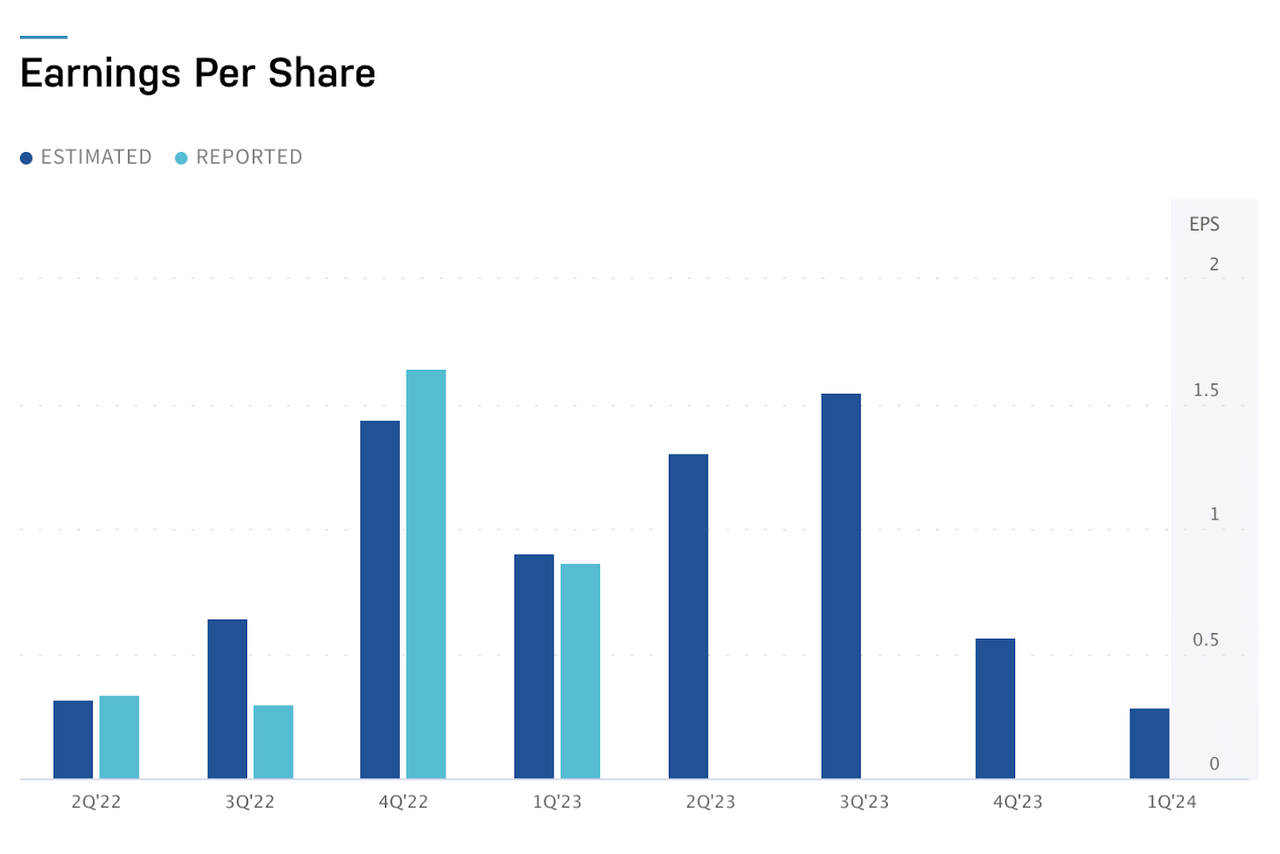

The second risk I’d look out for is bad earnings over the next few quarters. The company missed on EPS for Q1 this year. But future projections are also dismal, with an estimated EPS of $0.56 for Q4/23 (versus $0.86 most recently):

Nasdaq

Overall, I think much of the downside has already been priced in. Recent performance has been poor and the current valuation is quite cheap. Elliott claims that their plan could deliver 67% upside on the equity (up to a target of $55 per share), but I wouldn’t be surprised if the longer-term returns allow for additional gains. The utility sector is not one of great disruption, so a well-run company in the space should be able to deliver decent returns by simply “sticking the course.”

Conclusion

The optimal path forward for NRG is simple: focus on the core business and don’t waste resources by getting distracted in unfamiliar terrain. I’m confident that this pivot would generate strong returns for shareholders, but it remains to be seen if or when change will occur.

Another settlement between Elliott and management (as in 2017) may not be enough. Elliott may need to “go the distance” to effect the changes that it’s advocating for. However, I think they have credibility in this situation and will be able to leverage their prior experience to their advantage.

Given Elliott’s plan and involvement, I’m optimistic on NRG. The current activist situation creates positive asymmetry, which is slowly beginning to be priced in as Elliott’s chances of success improve. NRG’s valuation is still cheap however, earning a Valuation Grade of “A” according to Seeking Alpha’s factor model.

Read the full article here