Assicurazioni Generali (OTCPK:ARZGF) offers a high-dividend yield that seems to be sustainable, but its current valuation is not warranted considering its growth and profitability profile, thus there are better income opportunities in the European insurance sector.

Company Overview

Generali is an insurance company based in Italy, being among the three largest insurance groups in Europe by total assets, which amounted to about €519 billion at the end of 2022. Its current market value is about $31 billion and trades in the U.S. on the over-the-counter market.

Its main business unit is the Life segment, even though the company also has sizable operations in the non-Life segment, plus some activities in asset and wealth management through its subsidiary Banca Generali.

Geographically, Italy, France, and Germany are its most important markets, representing about two thirds of its total written premiums, plus it also has some exposure to other Central and Eastern European countries.

It has a leading position in the Italian insurance market, holding the number one position both in life and non-life, a position that was further strengthened by its acquisition of Societa Cattolica di Assicurazione in 2021. Indeed, Generali’s growth strategy has been both focused on organic efforts, plus some acquisitions, even though large deals aren’t expected.

More recently, Generali agreed to buy Liberty Mutual Insurance’s operations in Portugal, Spain, Ireland, and Northern Ireland for some $2.5 billion, including mainly personal lines and small commercial business. This expands Generali’s presence in these countries, generating some $1.3 billion of premiums in 2022 (vs. nearly $84 billion for Generali as a whole). This means that this acquisition is relatively small, in-line with its strategy to perform small bolt-on acquisitions that make sense from a financial perspective.

Additionally, Generali has recently announced that it agreed to buy Conning Holdings, an asset manager with some $157 billion of assets under management, boosting Generali’s AuM’s to about $850 billion. Asset management is one of the segments where Generali is pursuing growth over the long term, thus this acquisition makes strategic fit, enhancing Generali’s position in the U.S. and Asian countries.

Beyond asset management, Generali also wants to grow in property & casualty lines, which usually have better business margins than compared to life insurance, which means Generali’s business mix is likely to gradually change over the next few years to a more balanced profile, even though life insurance is expected to remain the largest one in the near future.

Financial Overview

Regarding its financial performance, Generali’s track record has been somewhat stable, even though its financial performance was impacted in 2020 by the pandemic, which had a negative effect on its life business.

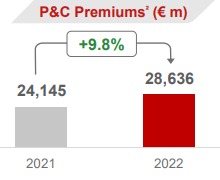

In more recent years, the company has reported a recovery on premiums and earnings growth, a positive trend that was maintained in 2022. During the last year, its total premiums increased by 1.5% YoY, on a like-for-like basis, supported by strong growth in the P&C segment (+9.8% YoY) to more than €28 billion in annual premiums.

P&C premiums (Generali)

In the life segment, Generali reported lower premiums both in traditional and unit-linked products, while on the other hand due to higher interest rates, Generali’s margin on new life business improved by more than 85 basis points (bps) in the year, to 5.35%. In the P&C segment, the company’s combined ratio increased to 93.2% (vs. 90.8% in 2021), which is negative for earnings growth.

Nevertheless, despite the mixed performance in both its life and non-life segments, Generali’s operating result was above €6.5 billion (+11% YoY), and its net profit increased by 2.3% YoY to €2.9 billion.

While its operating performance was positive, on the other hand, its investment result was affected by weaker capital markets during 2022, plus rising rates led to lower valuations in its bond portfolio, which in accounting terms is reflected on the company’s other comprehensive income line. This also had a negative impact on its solvency ratio, even though its ratio only decreased by seven basis points in the year.

Indeed, at the end of 2022, Generali’s Solvency II ratio was 221%, being therefore well capitalized and above the European insurance sector average. Thus, Generali has an excess capital position and can distribute a good part of its earnings to shareholders, providing a sustainable dividend over the long term, being one of its key financial goals.

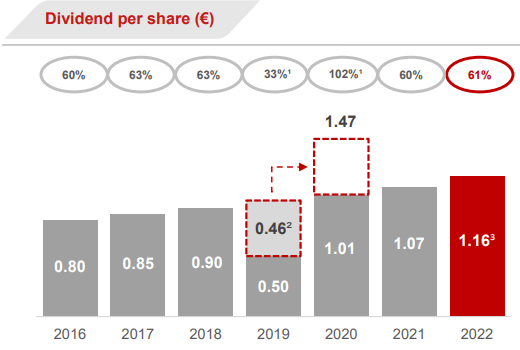

Its dividend history is quite good, given that it has delivered a growing dividend over the past few years, being the only exception 2020 due to the pandemic, which led to a more irregular dividend stream.

Dividends (Generali)

Its last annual dividend was €1.16 per share, an increase of 8.4% from the previous year, which at its current share price leads to a dividend yield of around 6.3% which is quite attractive for income investors. Moreover, its dividend payout ratio was 61% related to its 2022 earnings, in-line with its usual payout during normal years, which is an acceptable ratio for a stable company like Generali. This means that its dividend can be considered safe over the medium to long term, as it’s clearly supported by earnings and a strong capital position, allowing Generali to maintain its dividend policy over the coming years.

Indeed, according to analysts’ estimates, Generali’s dividend growth is expected to be close to its earnings growth over the next three years, given that its dividend payout ratio should remain at around 60% of earnings in the near future. Generali’s dividend per share is expected to grow at about 5.7% per year, over the coming three years, to €1.37 per share by 2025, which means Generali should maintain a high-dividend yield during this period.

Regarding its valuation, Generali is currently trading at around 1.7x book value, considerably above its historical average of about 1x over the past five years. While the company’s fundamentals have improved in recent years and its profitability has also increased, taking into account that its return on equity (ROE) ratio was above 12% in 2022, the highest level since 2007, this valuation seems too high and not supported by Generali’s profitability or growth prospects.

Indeed, assuming a sustainable ROE of around 12%, a risk-free rate of 3%, and the company’s historical beta of around 0.93x, I estimate its deserved price-to-book value multiple to be around 1.5x. This is above Generali’s historical average, but below its current valuation, which means that its current share price, Generali appears to be somewhat overvalued.

Conclusion

Generali has a stable business and a strong capital position, enabling it to offer a high and sustainable dividend yield. However, its growth prospects and valuation aren’t particularly impressive, while as I’ve covered in a recent article, ageas SA/NV (OTCPK:AGESY) has better growth prospects due to its exposure to Asia, offers a lower valuation and higher yield, making it a better income investment in the European insurance sector right now.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here