Investment Thesis

Diageo (NYSE:DEO) operational and financial results look promising. Company’s strategy is into increasing premium drinks share, which will support revenue growth. Also, Diageo has convenient cost structure, which makes company safe on the margins side & free cash flow generation. Now it isn’t a bargain purchase, so we set a HOLD status on Diageo shares with positive outlook.

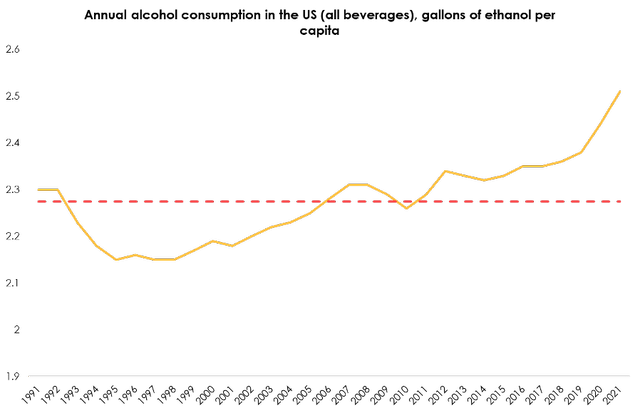

Alcohol consumption image

Alcohol, though isn’t an essential good, is typically referred to staples category. Historically alcohol consumption was rather stable (except for government intervention cases), and in the US for the last 3 decades was ~2.27 gallons of ethanol per capita with minor deviations.

Statista

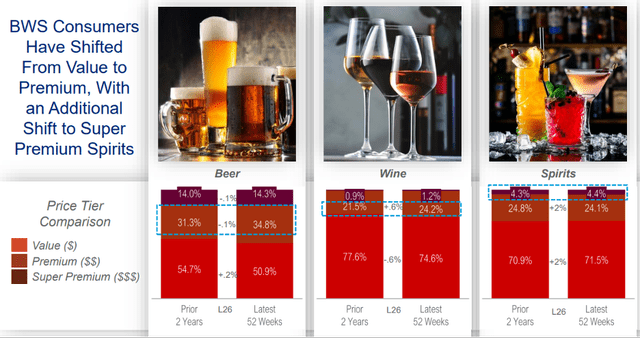

At the same time, we see a trend that in our opinion will likely to benefit Diageo, supporting its mid-term strategy. According to 2022 IRI research, in all the alcohol categories consumer shift to more premised drinks. As currently Diageo is growing its premium drinks portfolio, we believe the company is well-positioned on the market and will sustain from such trend in consumers preferences.

IRIWorldwide

Sales will be driven by premiumization effect

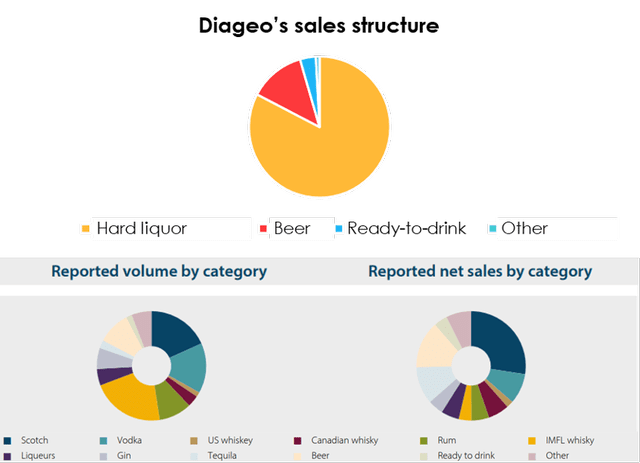

Diageo is a global producer and distributor of alcoholic beverages, with a presence in over 180 countries. The company owns more than 200 brands of alcoholic products.

Spirits make up the majority of sales (more than 80%), with beer making up more than 10%. Scotch and whiskey currently represent more than 50% of the company’s sales volume.

Diageo

About 40% of the company’s revenue comes from 6 international brands: Johnnie Walker, Guinness, Smirnoff, Baileys, Captain Morgan and Tanqueray.

However, the company also has a broad range of local brands for development in domestic markets (Crown Royal, Shui Jing Fang, Buchanan’s, Don Julio and so on).

Hard liquor will continue to be a key segment for Diageo, with the company’s focus now being on increasing the share of premium products in its sales structure.

Production facilities are spread out all over the world, which allows for stable logistics and distribution processes. The company has a total of 132 production sites.

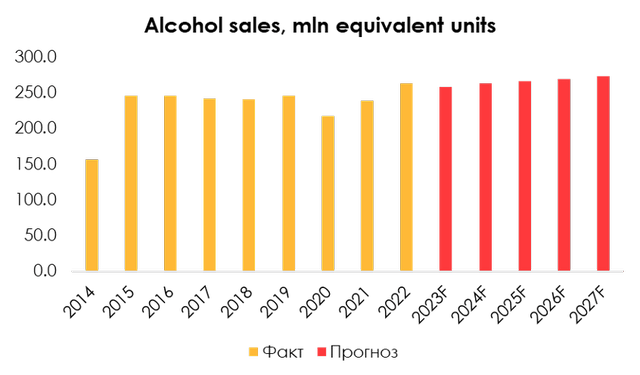

Diageo is a stable and well-established company whose growth strategy over the past 20 years has been to acquire and consolidate smaller brands, which means its production capacity is now not much dependent on organic capital investments and production expansion. From 2015 to 2019, the average sales volume was approximately 244 million equivalent units per year, showing little growth. The company completed several acquisitions in 2020-2021, including Aviation Gin, Davos and Chase, boosting its total sales volume to 263.0 million equivalent units in 2022, up 10% y/y. However, in the first half of fiscal year 2023, sales fell 4% y/y likely due to the normalization of inventory depletion, given the end of the COVID-19 epidemic, and the moderation of consumer demand.

We estimate current production capacity to be ~260 mln equivalent units a year and expect the company to grow very conservatively further down the road – by about 1.25% a year. We are forecasting that the volume of sales will reach 258 mln equivalent units (-2% y/y) in fiscal year 2023 and 262.9 mln equivalent units (+2% y/y) in fiscal year 2024.

Invest Heroes

The pricing of alcoholic products is heavily influenced by regulation and the size of excise duties. Excise duties vary between markets, making costs fairly volatile. That’s why we have decided to exclude excise duties from the pricing model and instead forecast net prices.

We believe this approach will not affect the accuracy of forecasting, as there is currently no reason to believe that there will be significant changes in the policies regulating alcohol sales. We assume that any potential changes in excise duties will affect the entire market, and producers will pass on the risk to consumers without sacrificing overall profitability.

Other than that, we base our price forecasts on the following factors:

- Inflation in the regions where the company operates

- The effect of premiumization of the product range

- The impact of FX rates in the medium term

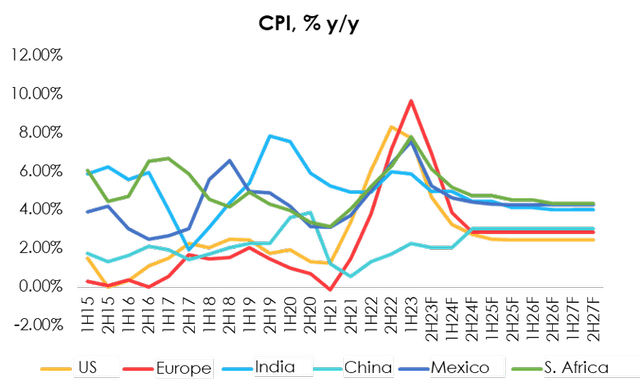

We believe that over the medium term inflation will remain elevated in key markets, which will have a favorable impact on Diageo’s pricing policy. For forecasting purposes, we use our own expectations for US inflation as well as inflation forecasts from research companies for the rest of the key markets.

Invest Heroes

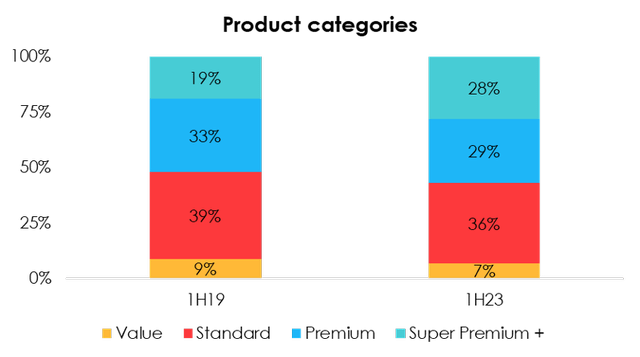

The effect from changing the product range will be a significant catalyst for price growth. Diageo’s strategy is largely focused on increasing the concentration of premium and super-premium brands in its sales structure, which raises the average selling price of its products. In the first half of 2023, the combined share of premium and super-premium segments totaled 57%, up from 52% in the first half of 2019, with the share of super-premium beverages increasing from 19% to 28%.

Diageo

We assume that the trend will continue in the future and expect the share of premium and super-premium products to steadily climb to 62% of the total by 2027.

Invest Heroes

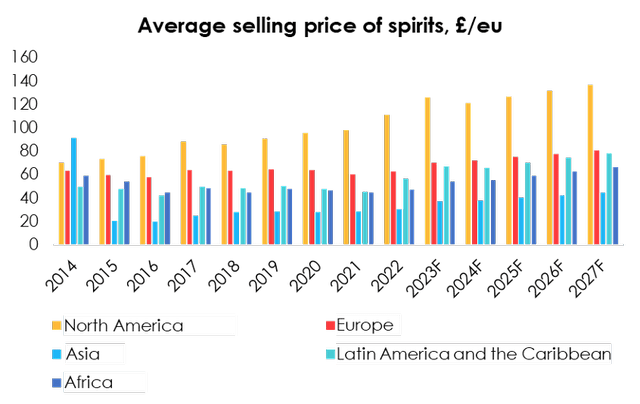

Because Diageo is a British company and its financial statements are denominated in pounds, an increase in GBP against other currencies will have a negative effect on prices and revenue. For forecasting purposes we use consensus estimates for FX rates for 2023-2027 and expect revenue to be subjected to a weak negative impact in the medium term.

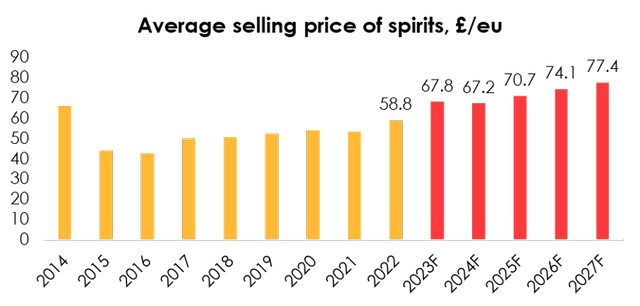

We forecast that the average selling price of spirits will reach £67.81/equivalent unit in 2023 (up 15.4% y/y), but will drop to £67.23/eu in 2024 (down 0.9% y/y) due to the negative impact from the pound’s rising FX rate and the trend for sales in the markets with lower prices to outpace sales in markets with higher prices. We anticipate that price growth will average 4.8% per year in fiscal years 2025-2027.

Invest Heroes Invest Heroes

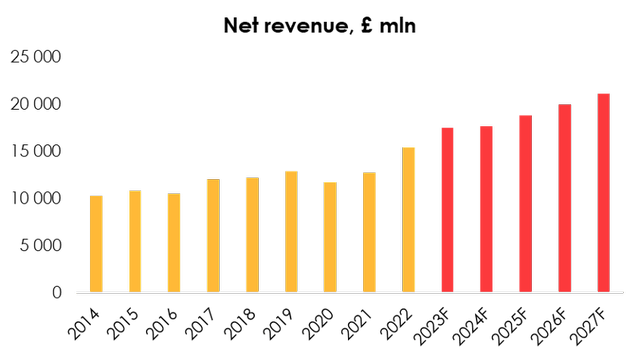

Therefore, we are forecasting that Diageo will earn a net revenue of £17 495 mln (+13.2% y/y) in 2023 and £17 678 mln (+1.0% y/y) in 2024. We expect revenue will grow at an average pace of 6.1% a year from fiscal year 2025 to 2027.

Invest Heroes

Cost structure is convenient, margins are safe

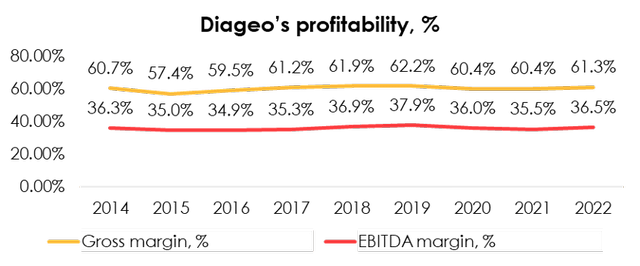

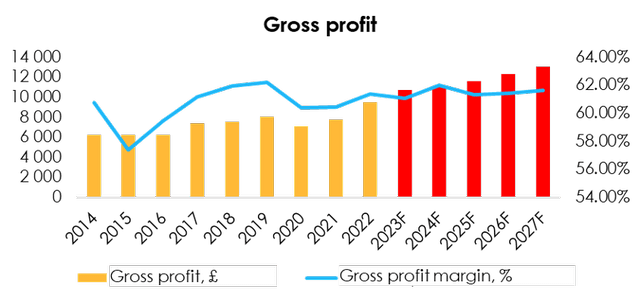

As has been said higher, Diageo’s production is spread out across the world, so the company’s production chains are stable. The gross profit margin of production has always been quite stable, at 60-61%, and even inflationary pressure and the energy crisis of 2022 did not affect the company’s margins.

Invest Heroes

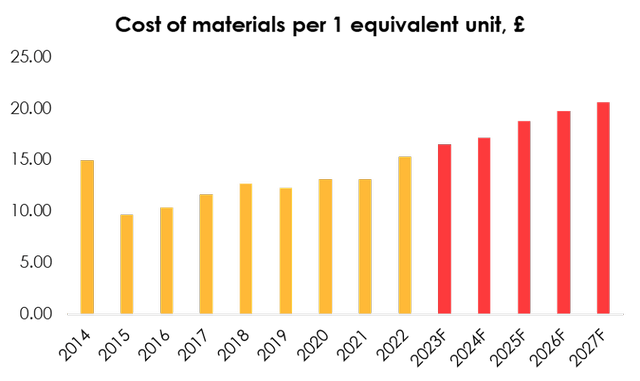

The production of alcohol involves sugar, water, fruits and vegetables, crops, flavorings, and many other food products and by-products, as well as various types of packaging. Due to the extensive product range, it is difficult to establish a close-to-reality cost structure, so we use food price index expectations for forecasting gross costs. However, Diageo’s production costs will tend to outpace the costs of the broader market due to the gradually rising proportion of premium drinks in its product range, which require more expensive inputs.

We expect the average cost of materials used in production to increase by 6.2% per year over the period from 2023-2027. However, we anticipate that costs will rise at a slower pace in fiscal year 2024 as prices are expected to compress as a result of a global recession.

Invest Heroes

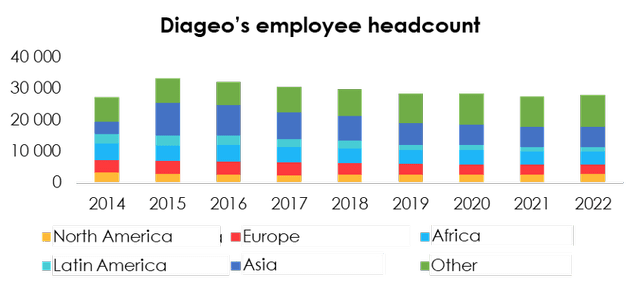

As of 2022, the company employed 27 987 people, of whom more than 43% were based in developing countries (Asia, Latin America, Africa).

Company data

Automation of production has allowed the company to significantly reduce the number of employees compared with the years 2015-2016, and we don’t expect much hiring in the future. We estimate the headcount to rise proportionally to the expansion of production, and expect that the workforce will reach 29 590 by 2027.

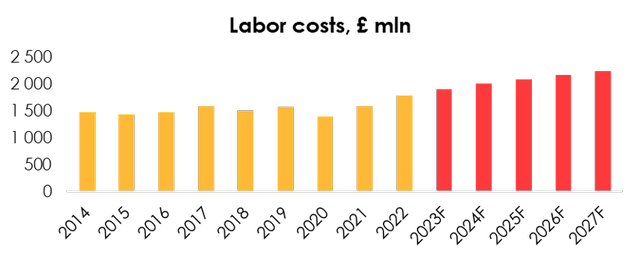

The high proportion of employees that are based in developing markets has a positive effect on the wage situation. Diageo paid an average wage of £55.6 thousand in 2022. We expect that metric to climb to £59.0 thousand (+6.0% y/y) in 2023, and to 61.5 thousand (+4.2% y/y) in 2024. Therefore, labor costs will total £1 904 mln (+6.1% y/y) in 2023, and £2 011 mln (+5.6% y/y) in 2024. Going forward, we see the budget for wages growing at an average rate of 3.7% a year.

Invest Heroes

Advertising is one of the most important aspects of Diageo’s costs. The company regularly conducts major marketing campaigns, stimulating consumer demand and distributor interest.

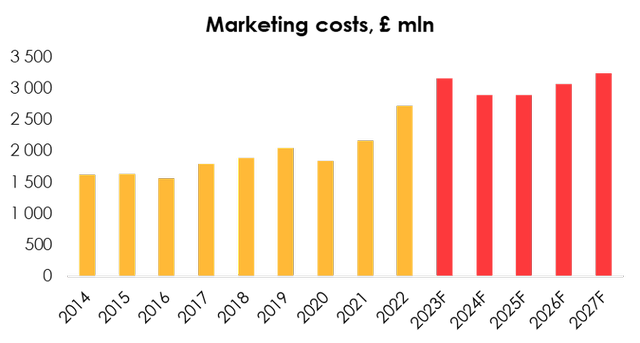

Diageo spends an average of 15.8% on marketing, but the proportion climbed to 17% and 17.6% in 2021 and 2022, respectively. We expect that the marketing budget will remain slightly elevated in 2023 (given the trend of the first half, we assume that the company is now in the middle of a major marketing campaign), but will start to come back to normal from 2024.

Therefore, we anticipate that marketing costs will total £3 153 mln (+15.8% y/y) in 2023, and £2 891 mln (-8.3% y/y) in 2024.

Invest Heroes

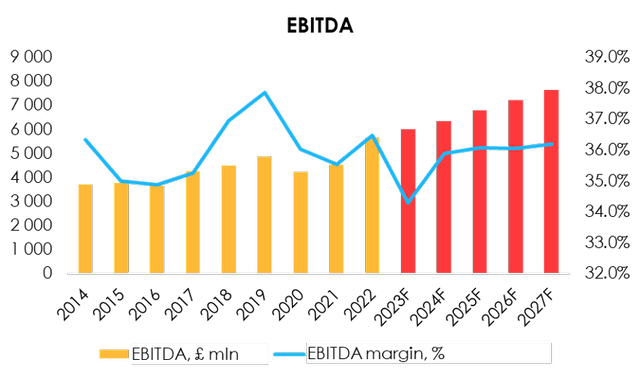

Given the trend for the cost of materials and labor, we expect gross profit to total £10 677 mln (-0.5% y/y) in 2023 and £10 955 mln (+1.54% y/y) in 2024. Gross profit margin is poised to remain stable, at an average of 61.5%, over the period from 2023-2027. Turning to EBITDA, we are forecasting it to reach £6 001 mln (+6.5% y/y) in 2023 and £6 344 mln (+5.7% y/y) in 2024. EBITDA margin will remain stable, at an average of 36.1%, over the period from 2025-2027.

Invest Heroes Invest Heroes

Cash flows are stable, leverage is comfortable, so dividend raises are incoming

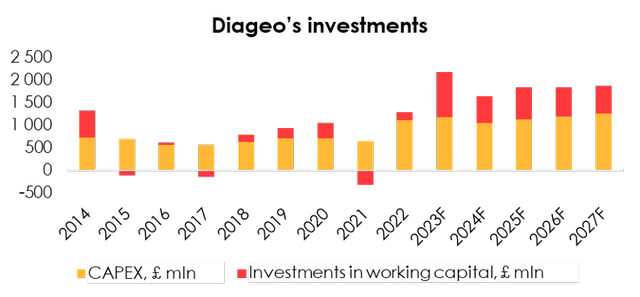

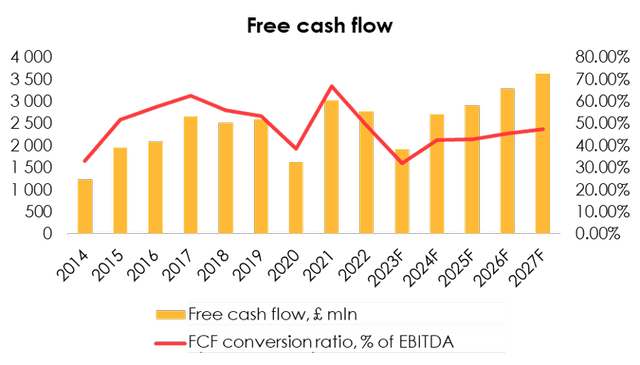

Diageo doesn’t seem to have to go through a lot of effort to generate free cash flow. Historically, the FCF/EBITDA conversion ratio has averaged ~52%. Working capital has a fairly high turnover rate, and capital expenditures do not exceed 7% of revenue.

We expect Diageo’s ratio of capital expenditures to revenue to continue to be 5.9%, totaling £1 051 mln in 2023 and £1 120 mln in 2024.

Investments in working capital will be slightly elevated in 2023 due to a sharp increase of receivables in the first half of the year, but will normalize to 3-3.5% of revenue in 2024-2027.

Invest Heroes

Therefore, we are forecasting that Diageo’s free cash flow will total £1 923 mln in 2023 and £2 710 mln in 2024.

Invest Heroes

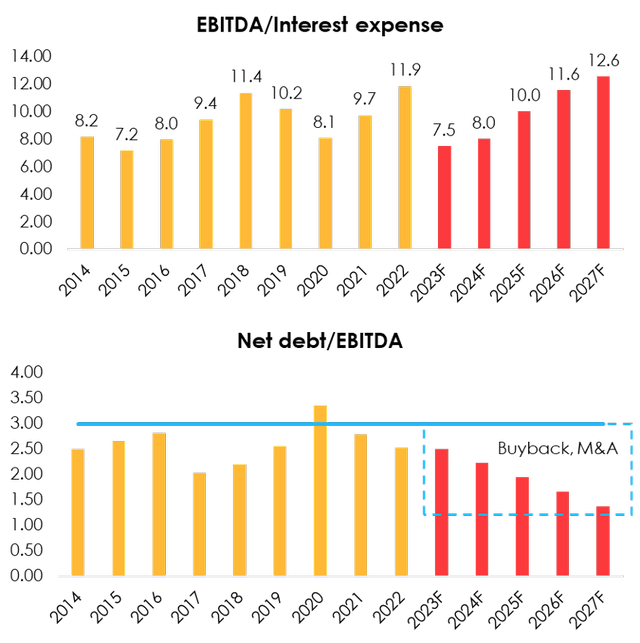

Diageo has a comfortable bond debt repayment schedule, with $500 million due in 2024, $600 million due in 2025, and $1 250 million due in 2027.

The company’s current net debt to EBITDA ratio is ~2.5x. Going forward, the management plans to maintain the debt burden at the same level (2.5x – 3х).

We see no significant credit risks for Diageo: The company does not require large capital expenditures, has high inventory turnover, a comfortable repayment pace and interest burden.

Invest Heroes

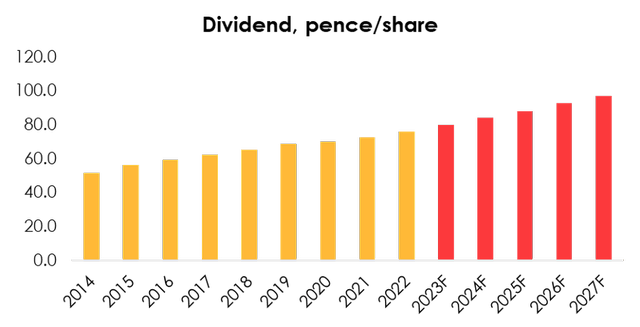

Given the company’s strong capability to generate free cash flow and comfort leverage level, we believe investors could count on dividends growing at a steady rate of 5% every year. That would still leave the company with enough cash to repurchase shares or engage in M&A deals. We estimate that Diageo will pay out a dividend of £0.80 (+5% y/y) for the year 2023 and £0.84 (+5% y/y) for 2024.

Invest Heroes

Valuation

While Diageo is the leader in the market of alcoholic beverages, making it hard for the company to expand its market share organically, we believe its financial results will continue to grow steadily due to the following:

- The average price of sold beverages and the pace of revenue growth will be rising, supported by the increasing share of premium products. Even if sales volume expands only modestly, we believe Diageo’s organic growth of revenue could average 5-6%.

- The company has a convenient production chain and cost structure: Its production is decentralized, which removes the risk of volatility in logistics costs, while most of its workforce is based in developing countries, where expected wage increases will not have a significant impact on profitability.

- Diageo has extensive experience in acquisitions and promotion of local brands, which in the long term will support the company’s position in domestic markets.

We are evaluating Diageo fair value price based on FTM EV/EBITDA multiples and pegging the fair value of the company’s shares at £41. We are assigning a HOLD rating to the stock.

Invest Heroes

Conclusion

We’re pleased with the development of Diageo plc: despite leadership positions, company still finds the ways to grow. Increasing premium drinks share in sales structure will be a strong support for financials & share price. Also, we don’t see significant risks related to production inflation as company’s cost structure is rather convenient.

To manage the position, we suggest keeping an eye on financial statements of DGE and its competitors and industry research (e.g. Nielsen, SVB, IRIWorldwide).

Read the full article here