Keysight Technologies (NYSE:KEYS) is a leading provider of testing and measurement solutions for various industries, including commercial communications, aerospace, defense & government, automotive, and semiconductors. Keysight Technologies became an independent company separate from Agilent (A) in November 2014.

Keysight is currently leading the competition in 5G testing and measurement, with a market share of 25% according to the management team. As 5G technology continues to grow, Keysight has significant potential for further expansion. Additionally, software and services account for over one-third of Keysight’s revenue. I believe the company’s software-centric growth strategy allows for margin expansion and accelerated organic growth over time.

Considering their targets of 5-7% organic sales growth and double-digit EPS growth, Keysight’s projections seem reasonable to me. Moreover, I think the current downturn in communication spending presents a favorable opportunity for investment in Keysight.

Structural Growth Tailwinds

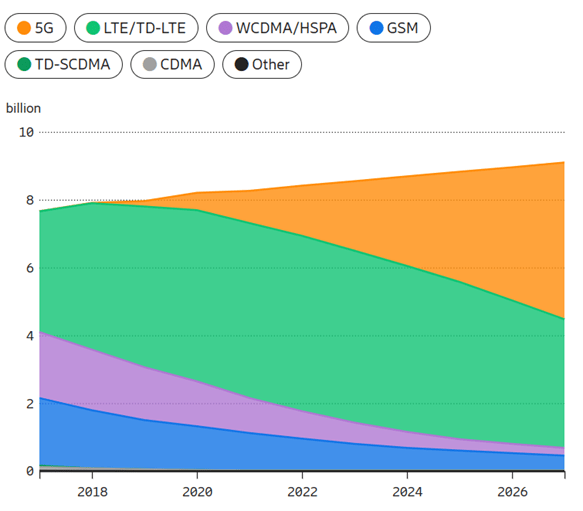

Capitalizing on 5G Expansion: If we consider the field of commercial communications, it is evident that the primary driver at present is the transition to 5G networks. We are currently in the commercialization phase of 5G, and even in countries and areas where 5G is actively being deployed, its coverage remains limited to major cities, with sporadic availability elsewhere.

According to Ericsson Mobility Report, due to delayed spectrum auctions in several countries and persisting challenging macroeconomic conditions, it is projected that global 5G subscriptions will reach 4.6 billion by the end of 2028, constituting more than 50 percent of all mobile subscriptions. By 2028, 5G is expected to become the predominant mobile access technology in terms of subscriptions. Therefore, there is a significant runway for growth ahead.

During the rollout of 4G, when Keysight was still part of Agilent, the company lagged behind the competition. Anritsu and Rohde & Schwarz held substantial market shares in 4G. However, since the spin-off from Agilent, Keysight has focused on R&D and engaged in mergers and acquisitions, which has positioned the company for success in the 5G space. Keysight is expanding its industry-leading 5G platform to support 5G-SA, mmWave, D2D, and UL improvements.

Ericsson 2023, Mobile subscriptions by technology, https://www.ericsson.com/en/reports-and-papers/mobility-report/dataforecasts/mobile-subscriptions-outlook

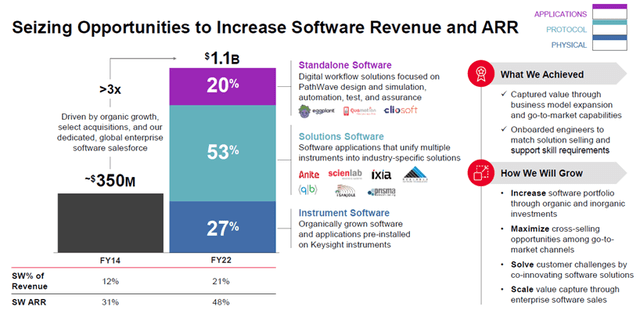

Increasing Software and Services: The growth of software and services revenue across business segments has remained steady and accounted for over one-third of Keysight’s total revenue. I anticipate that the growth of software and services will continue to outpace the overall company growth in the next three years. Combining software and services creates another pillar of P&L resiliency, particularly in more challenging macroeconomic environments, according to the company’s management team. They also state that software and services can constitute as much as 40% of the 5G solution package provided by Keysight.

Furthermore, software carries a higher gross margin for Keysight. Therefore, the increasing emphasis on software will contribute to expanding their margins. In the next three years, I expect their software order growth to continue surpassing the overall growth of Keysight.

Keysight 2023 Capital Market Day

Automotive Growth: Keysight began developing its automotive business in 2017 through organic growth and tuck-in acquisitions. As more cars become connected, there is an increasing need for testing and measurement in the automotive industry, benefiting both auto manufacturers and component makers. This growing market presents an opportunity for Keysight to leverage its existing technologies. It is worth noting that 54% of Keysight’s revenue is tied to R&D activities, 34% to manufacturing, and 12% to operational activities. Therefore, even if automotive volumes decrease, Keysight could still experience positive growth in this end-market, as more than half of their revenue is linked to R&D activities.

The majority of Keysight’s automotive business focuses on the development of next-generation technologies in areas such as electric vehicles, autonomous vehicles, V2X communication radar, as well as EV charging. For instance, Keysight’s comprehensive solutions enable customers to develop batteries with improved range and faster charging times, while efficiently testing their interoperability against global infrastructure standards under real-world conditions.

As electric vehicle penetration continues to increase, I believe Keysight will maintain strong growth in this area. In Q2 FY23, they achieved robust double-digit revenue growth in their automotive business. While they do not provide a specific breakdown of their automotive sales, I estimate that it currently accounts for a single-digit percentage of the company’s overall revenue.

Key Headwinds and Risks

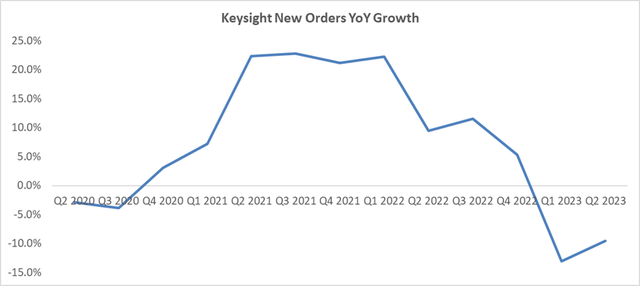

Commercial Communications: Accounting for 45% of Keysight’s revenue, the commercial communications segment experienced a 7% decline in Q2 FY23, reflecting a normalization of the demand environment. The communication industry is currently witnessing a cautious spending pattern, especially in the smartphone and PC computing markets, as customers navigate through post-pandemic inventory dynamics and macroeconomic uncertainties. Keysight’s new order growth declined by 13% in Q1 FY23 and 9.5% in Q2 FY23.

Keysight Quarterly Results, Author’s Calculation

Some commercial communication customers are still in the process of clearing inventories. Specifically, in the 5G segment, R&D activities and base stations continue to perform well. However, Keysight is facing some pressure on the networking side. I believe that the overall weakness in the commercial communication space may persist in the coming quarters. However, over time, the inventory situation is expected to normalize in my opinion.

China trade restrictions: Huawei accounted for 4% of Keysight’s group revenue in FY20. When the trade restrictions with China were implemented, Keysight faced significant challenges. Going forward, Keysight does have some products that it will continue to sell to Huawei, but these represent a very small portion of its overall portfolio. They do not anticipate Huawei being a significant customer in the future. I estimate that Huawei will account for approximately 1%-2% of Keysight’s customer base going forward, making the associated risk negligible.

Financial and Valuation

Despite the challenging macro environment, Keysight expects to achieve better earnings performance than previously anticipated, with a projected strong mid-single-digit EPS growth for the full year. This positive revision is attributed to the easing of supply chain constraints and the impact of cost inflation on their EPS growth.

Over the long term, Keysight maintains its targets of achieving 5-7% organic sales growth, a 31%-32% adjusted operating margin, and double-digit EPS growth.

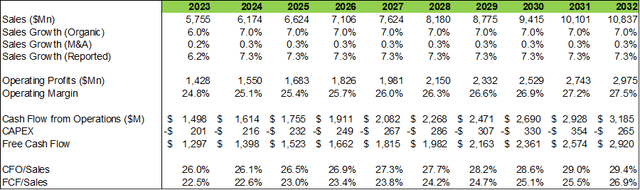

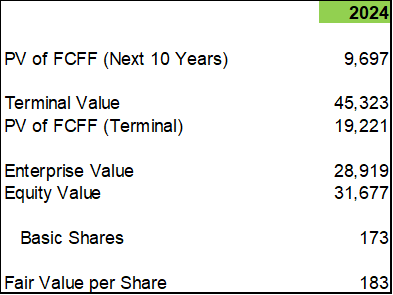

In the DCF model, I assume 7% of normalized organic revenue growth, 30bps margin expansion per year, 10% of WACC, 4% of terminal growth rate, and 12% of tax rate. The free cash flow conversion is calculated to reach 26.9% in FY32 in the model. The key metrics can be founded in the table below.

Keysight DCF Model – Author’s Calculation

With all these assumptions, the present values of FCFF over the next 10 years and terminal are $9.7 billion and $19.2 billion, respectively. Adjusting debt and cash, the fair value is $183 per share as per my estimate.

Keysight DCF Model – Author’s Calculation

When considering the multiples, the stock is currently trading at around 16 times EV/EBITDA and 20 times free cash flow. This valuation appears to be quite reasonable for a company that is expected to achieve double-digit bottom-line growth.

Conclusions

The current macro environment, with weak demand in commercial communications, presents a favorable entry point for this stock, in my opinion. Keysight’s leading technology in the 5G sector indicates significant potential for future growth. Furthermore, the company’s software-centric growth strategy allows for margin expansion and accelerated organic growth over time. Based on these factors, I assign Keysight a ‘Strong Buy’ rating.

Read the full article here