Investment Thesis: I expect Air Canada to continue to see upside from here, on the basis of strong growth in passenger revenue per RPM.

In a previous article back in January, I made the argument that Air Canada (TSX:AC:CA) could see further upside from here, on the basis of growing demand in the face of higher ticket prices as well as a codeshare agreement with Emirates providing an additional source of revenue growth.

Since then, the stock has ascended to a price of $24.88 at the time of writing:

TradingView.com

The purpose of this article is to assess whether Air Canada has the ability to see continued growth from here taking recent performance into consideration.

Performance

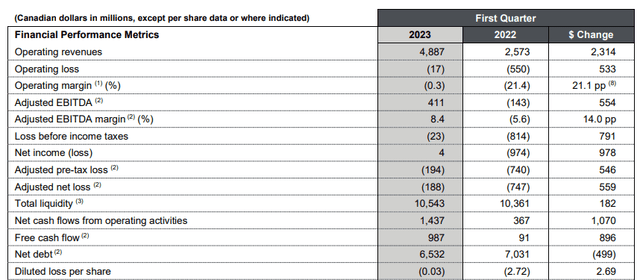

When looking at Q1 2023 financial results for Air Canada, we can see that operating revenues saw an 89% rise on that of Q1 2022 – while diluted earnings per share is almost back into positive territory at -$0.03.

Air Canada: First Quarter 2023 Financial Results

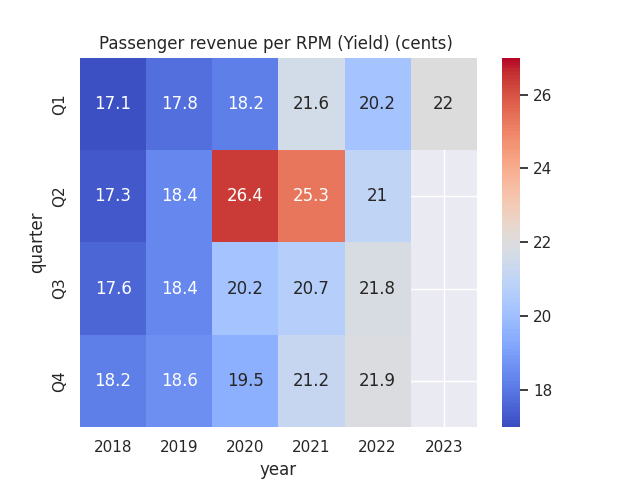

To get a better sense of what is driving revenue growth, I would like to analyse passenger revenue per RPM in more detail. From analysing this metric – which measures the revenue earned from a passenger for every mile flown – we can see that the same remains significantly above that of pre-COVID levels.

Figures sourced from historical Air Canada News Releases (Q1 2019 to the present). Heatmap generated by author using Python’s seaborn library.

Q2 2020 and 2021 showed abnormally high passenger revenue per RPM – which was influenced by the fact that overall revenue passenger miles were vastly lower than usual levels due to COVID. However, we have seen that passenger revenue per RPM of 22 cents for Q1 2023 was significantly higher than that of 17.8 cents recorded for Q1 2019.

Additionally, total revenue passenger miles for Q1 2023 came in at 18,578, nearing that of 21,293 seen in Q1 2019. Notably, revenue passenger miles of 22,118 in Q3 2022 exceeded Q1 2019 levels and passenger revenue per RPM still came in at 21.8 cents.

Overall, we can see that passenger traffic has rebounded to that of pre-COVID levels but passenger revenue per RPM continues to remain higher than that seen pre-COVID, which is quite encouraging.

From a balance sheet standpoint, we can also see that the company’s long-term debt and lease liabilities to total assets ratio in March 2023 – while still remaining substantially above 2019 levels – is down from that of September 2022:

| September 2019 | September 2022 | March 2023 | |

| Long-term debt and lease liabilities | 8116 | 15799 | 14901 |

| Total assets | 27497 | 29754 | 30476 |

| Long-term debt and lease liabilities to total assets ratio | 29.52% | 53.10% | 48.89% |

Source: Figures sourced from Air Canada Q3 2019, Q3 2022, and Q1 2023 Condensed Consolidated Financial Statements and Notes. Figures provided in Canadian dollars in millions (except long-term debt and lease liabilities to total assets ratio). Long-term debt and lease liabilities to total assets ratio calculated by author.

My Perspective

As regards my take on the above results and the implications for the growth trajectory of the stock going forward, the fact that Air Canada has been able to continue increasing passenger revenue per RPM in spite of higher prices indicates that demand has been remaining buoyant.

Additionally, the fact that long-term debt relative to total assets has been decreasing is an encouraging sign – as it indicates that Air Canada is now generating sufficient revenue to pay back debt loads incurred during the pandemic.

With regard to my previous point concerning Air Canada’s codeshare agreement with Emirates potentially resulting in higher revenue growth, the company has since gone on to also strike a codeshare agreement with flydubai – which further opens up Air Canada’s network in the Middle East to countries including Saudi Arabia, Oman and Bahrain.

When looking at the revenue breakdown across geography, we can see that even though overall passenger revenues are up by over 7% since March 2019 – revenue for Canada is actually down during this period and Atlantic revenues (which includes the Middle East) is up by over 20%.

| March 2019 | March 2019 (% share) | March 2023 | March 2023 (% share) | |

| Canada | 1104 | 28.93% | 1064 | 26.03% |

| U.S. Transborder | 947 | 24.82% | 966 | 23.63% |

| Atlantic | 767 | 20.10% | 924 | 22.60% |

| Pacific | 535 | 14.02% | 492 | 12.04% |

| Other | 463 | 12.13% | 642 | 15.70% |

Source: Figures sourced from Air Canada Q1 2019 and Q1 2023 Consolidated Financial Statements and Notes. Percentages calculated by author.

In this regard, I take the view that international passenger revenue is likely to account for a greater share of revenue going forward – and establishing codeshare agreements with major airlines in the Emirates is likely to prove a good strategic move for Air Canada as this region continues to grow in importance in the context of the global air passenger network.

Risks

In terms of the potential risks to Air Canada at this time, we have seen that while long-term debt to total assets has been decreasing – the same still remains substantially higher than levels seen in 2019. While it is encouraging that long-term debt has started to decrease, debt levels still remain elevated and there is the risk that we could see revenue growth start to plateau before Air Canada is able to deliver a substantial decline in long-term debt.

Moreover, while the rebound in revenue growth has been encouraging – diluted earnings in the last quarter were still technically negative. There is also the risk that revenue growth starts to plateau as the rebound in air passenger traffic post-COVID reaches saturation, while costs continue to rise in line with inflationary pressures. Should this happen, then this could place further pressure on earnings growth.

Conclusion

To conclude, Air Canada has seen strong growth in passenger revenue per RPM, indicating that consumers are willing to pay higher prices to travel. Additionally, the company has continued to expand its revenue across the Atlantic region – driven in part by codeshare agreements with major airlines in the Emirates.

In spite of the potential risks with respect to a potential plateau in revenue growth and the associated impact on debt levels and earnings growth, I take the view that Air Canada is in a good position to overcome these risks and continue to take a bullish view on the stock.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here