Both Main Street Capital (NYSE:MAIN) and SLR Investment Corp (NASDAQ:SLRC) are high-yield business development companies (i.e., BDCs) that pay out monthly dividends to shareholders. Many investors – especially retirees – love monthly dividend stocks because:

- Monthly dividend stocks make it easier to budget using passive income to meet living expenses.

- Monthly dividend stocks are easier psychologically to hold through market crashes because of the consistent rewarding feeling that they provide via their monthly payouts.

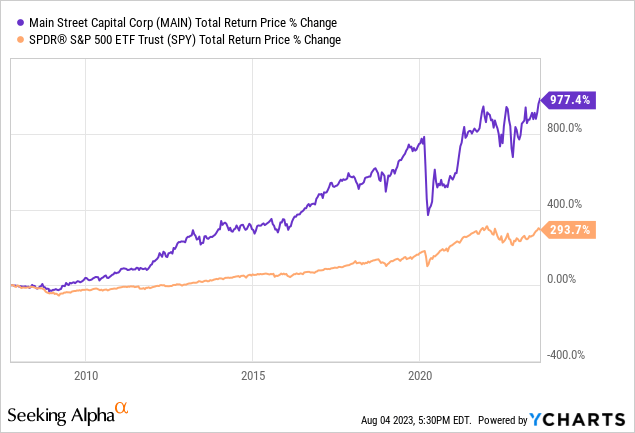

Internally-managed MAIN has a remarkable track record of delivering exceptional long-term total returns to shareholders:

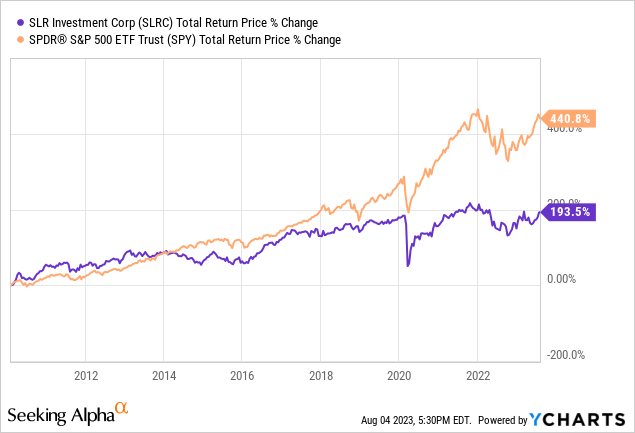

In contrast, SLRC has struggled to a much greater extent:

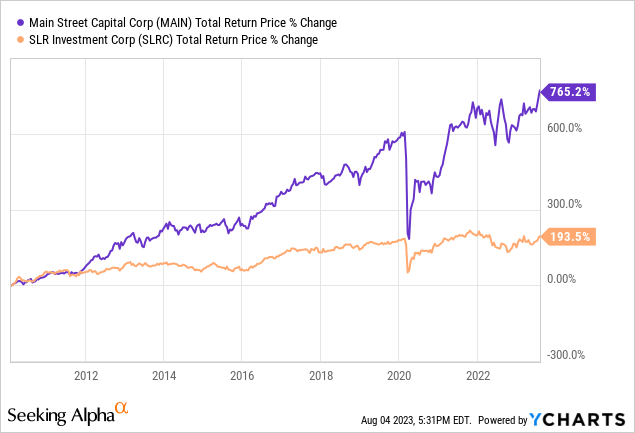

Putting their performances side-by-side makes this comparison clearer:

While some investors would stop reading immediately and simply conclude that SLRC is a bad investment and MAIN is an excellent investment based solely off of their dramatically different track records, we are focused on forward-looking analysis, with only a peak at the past to help inform that forward analysis. As a result, in this article, we will compare them side by side and offer our take on why SLRC is a better buy than MAIN right now.

#1. SLRC Is Dramatically Cheaper

First and foremost, when you are buying a BDC, you are effectively buying a closed end fund that consists of a broadly diversified portfolio of underlying investments, many of which are some sort of fixed income product. As such, each BDC publishes a monthly update to their net asset value, which is the sum of the fair market value of all their assets minus the fair market value of all their liabilities. On that basis – along with several other metrics – SLRC is hands-down far cheaper than MAIN:

| Valuation Metric | MAIN | SLRC |

| Price to NTM Normalized Earnings | 10.94x | 8.95x |

| NTM Dividend Yield | 6.5% | 10.9% |

| P/NAV | 1.57x | 0.83x |

What this means is that for every dollar invested in SLRC, you get – in addition to a 440 basis points higher dividend yield than at MAIN – $1.20 in underlying asset value compared to just $0.64 in underlying asset value at MAIN. This means that the market is currently assigning a near 2x premium to the value of MAIN’s underlying assets relative to SLRC’s underlying assets.

Moreover, SLRC’s historical mean P/NAV is nearly 1x (0.94x) whereas MAIN’s is 1.49x. This means that SLRC is trading at a substantial discount to its historical mean P/NAV whereas MAIN is trading at a meaningful premium to its historical mean P/NAV.

Yes, MAIN has a superior long-term track record and is internally managed. However, is SLRC really so bad that its assets should have a near 50% discount applied to their fair market value relative to MAIN’s assets? We will explore this question further in our next two points…

#2. SLRC Is More Defensively Positioned

Given that we could very possibly be on the verge of a recession, investing in a defensively positioned portfolio is more important than ever. When comparing MAIN and SLRC in this area, we find that SLRC is actually more defensively positioned.

Yes, MAIN has 70.7% exposure to 1st lien senior secured loans. However, it also has the remaining 29.3% of its portfolio invested in equity investments. Meanwhile, SLRC appears inferior with just 48.5% of its portfolio invested in 1st lien senior secured loans, 1.5% in 2nd lien senior secured loans, and 10.3% invested in unsecured/subordinated debt, with the remaining 39.5% invested in equity investments and cash.

However, these headline numbers/classifications are misleading. The reality is that SLRC’s portfolio is very different in composition from most other BDCs like MAIN. Only 23.3% of its portfolio is invested in senior secured sponsor finance investments. Meanwhile, 11.1% of its portfolio is invested in specialty life science loans that are secured by cash on the balance sheet where SLRC has the ability to sweep cash and call the loans. They are very conservatively underwritten, with a target loan to value of 15-20% and the company has stated that these are the best risk-adjusted returns found in their whole portfolio.

Moreover, its asset-based loans – which make up another 33.3% of the portfolio – are also considered to be more conservative than the senior secured sponsor backed loans. This puts SLRC’s portfolio total at ~68% in loans that are either as conservatively underwritten or more conservatively underwritten than MAIN’s 1st lien senior secured loans.

Finally, the remaining 32.1% of SLRC’s portfolio is invested in equipment financings. While these are not as conservative as some of SLRC’s other product offerings, they are still backed by hard assets with attractive valuation coverage ratios. Therefore they are generally much more conservative than many of MAIN’s equity investments. In aggregate, SLRC’s asset exposure appears to be considerably more conservative than MAIN’s.

#3. SLRC’s Poor Track Record Is Misleading

Finally, SLRC’s poor track record – especially relative to MAIN’s – is a bit misleading for the following reasons:

- Given that SLRC’s business model is more defensively positioned than MAIN’s, during economic expansions such as we have experienced over the past decade plus, MAIN will likely outperform SLRC. However, during a downturn, SLRC’s more conservative asset positioning should outperform relative to MAIN’s more aggressively positioned portfolio.

- MAIN’s stock was buoyed by the strong macroeconomic tailwind to trade at a large premium to NAV over a long period of time. It was then able to leverage this premium to issue stock at a highly accretive valuation, thereby driving long-term shareholder book value per share and dividend per share growth. SLRC, in contrast, was locked out of this for large portions of its history. This makes its book value and dividend per share track record appear to be worse relative to MAIN’s than it would otherwise have been.

- A meaningful bite has been taken out of SLRC’s total return performance due to its shrinking price to NAV multiple, whereas MAIN’s total return performance has been padded by its expanding price to NAV multiple.

- SLRC’s book value is likely meaningfully understated at the moment. Since December 31, 2019, the net asset value of the company has decreased by a little over $3 per share. This decline has affected the company’s performance as business development companies typically trade at a multiple of their NAV. Despite performing well in credit management, the decline in NAV was primarily caused by two factors: approximately $60 million in losses and a 60 cents per share decline due to over-distributing dividends compared to net investment income, as the company was underleveraged at the time. However, at the time the company saw a path to recover and maintain their dividend at 41 cents per share, so they chose not to cut dividends. They have since achieved that goal, restoring NII per share to a level above that $0.41 quarterly dividend level (though paid out monthly in increments that are one-third of the quarterly level). Additionally, there are about 60 to 70 cents per share of NAV declines in their current portfolio that are marked to market, but they expect these to improve over time. Finally, the biggest factor contributing to the NAV decline was the market valuations of their commercial finance companies, influenced by rising interest rates and the general valuation of financial companies. They believe that part of their NAV will recover over time. Combining the recovery of lost NAV and driving further earnings growth, they expect their discount to NAV to decrease significantly in the coming years, leading to very strong total return outperformance.

MAIN Stock Vs. SLRC Stock: Investor Takeaway

MAIN is without a doubt an exceptional BDC and if the valuation gap between MAIN and SLRC were far narrower, we would likely favor MAIN over SLRC. However, the current premium being assigned to MAIN’s underlying assets seems excessive in our view, especially given where we are in the economic cycle;. Meanwhile, the discount being applied to SLRC’s underlying assets seems excessive, especially given their conservative nature and the potential for remarkable recovery in SLRC’s NAV moving forward.

As a result, we rate SLRC a Buy and MAIN a Hold at the moment and hold SLRC as one among several BDCs in our portfolio at the moment.

Read the full article here