We’re halfway through the Q2 Earnings Season for the Gold Miners Index (GDX) and it’s been a mixed reporting period overall, with the higher gold price being offset by increased operating costs for most miners and one-time headwinds that have affected production (weather, wildfires) in some jurisdictions. Fortunately, Kinross (NYSE:KGC) was one of the few million ounce producers to put up strong results, with production up 22% year-over-year on a continuing basis (albeit down if not adjusting for the sale of Chirano and Kupol) at lower costs. The result was a significant increase in revenue and all-in sustaining cost [AISC] margins year-over-year, and a 106% increase in operating cash flow, helping the company to continue its debt pay down. Let’s look at the results in a bit more detail below:

Tasiast Mine Operations (Company Website)

All figures are in United States Dollars unless otherwise noted.

Q2 Production & Sales

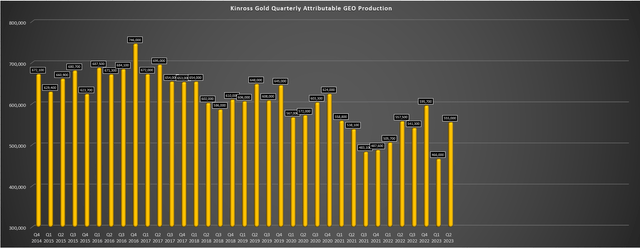

Kinross released its Q2 results last week, reporting quarterly production of ~555,000 gold-equivalent ounces [GEOs], a 22% increase year-over-year on a continuing basis. And while the company has continued to see lower production on a long-term basis (as shown below), impacted by a ~107,000 ounce headwind year-over-year related to zero contribution from Kupol and Chirano, its two largest operations put together very solid performance in Q2 2023, and we saw a significant increase in production from La Coipa which has successfully ramped up to full production at industry-leading costs. The result of the higher production and gold sales in the period combined with a higher average realized gold price ($1,796/oz) was that Kinross enjoyed a 33% increase in revenue ($1,092.3 million vs. $821.5 million), translating to the best quarter from a sales standpoint in nearly three years.

Kinross Gold – Quarterly GEO Production (Company Filings, Author’s Chart) Kinross – Quarterly Revenue (Company Filings, Author’s Chart)

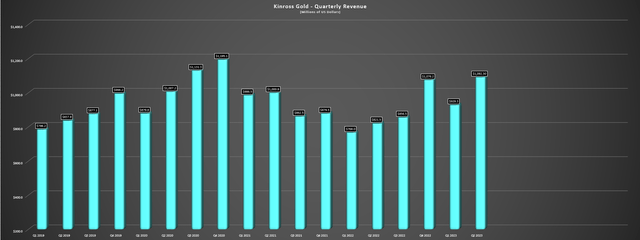

Digging into the operations a little closer, the company’s two largest contributors both had exceptional quarters, with Tasiast reporting record quarterly production of ~157,800 ounces (Q2 2022: ~129,100 ounces), with the benefit of higher grades (3.25 grams per tonne of gold), 400 basis point higher recovery rates, which were offset by a marginal dip in throughput (~1.66 million tonnes). Meanwhile, Paracatu also performed well, with production of ~164,200 ounces driven by a strong quarter for throughput (~15.1 million tonnes) and higher grades plus recoveries (0.42 grams per tonne of gold with 80% recoveries). The result was a material improvement in costs year-over-year in these assets, and Tasiast should see cost benefits from its soon-to-be commissioned solar plant, which could deliver a $15/oz cost savings once in operation at year-end.

Kinross Gold – Quarterly Production by Mine (Company Filings, Author’s Chart)

Unfortunately, the robust Q2 results out of Tasiast, Paracatu and La Coipa (~66,700 ounces) was partially offset by a weak quarter from the company’s United States operations. In fact, production from its United States portfolio (Fort Knox, Bald Mountain, Round Mountain) fell to just ~166,200 ounces (Q2 2022: ~188,000 ounces) at higher costs. This sharp decline in throughput from its Tier-1 ranked jurisdictions was despite a slightly better quarter at Round Mountain (~57,400 ounces vs. ~56,700 ounces), with lower grades affecting output at Bald Mountain and lower throughput at Fort Knox (fewer tonnes placed on Barnes Creek heap leach facility). However, despite the weaker Q2 for its Alaskan and Nevada mines, Kinross remains on track to meet full-year production of ~2.1 million GEOs, and H2 should be better for its Americas portfolio, with similar H2 vs. H1 production from Paracatu and La Coipa and slightly higher production out of its United States mines.

Fort Knox Fleet (Company Website)

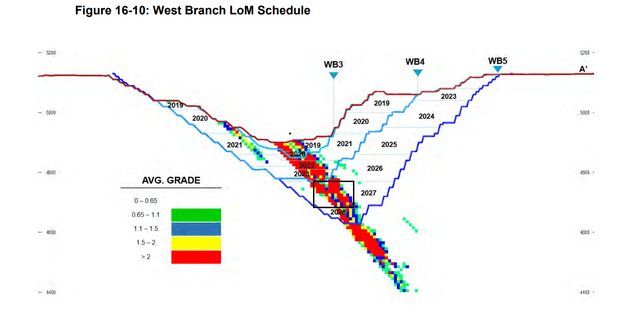

That being said, while Tasiast will enjoy higher throughput rates with its 24K expansion delivered in line with schedule (per 2022 year-end commentary for “mid-year”), the mine benefited from elevated grades year-to-date, with head grades of 3.30+ grams per tonne of gold being well above reserve grades (1.7 grams per tonne of gold). So, while fresh contribution from higher-grade Manh Choh ore in H2-2024 will benefit its Fort Knox operations in Alaska, we could see some offset of this near-term growth as grades normalize at Tasiast, with head grades expected to peak this year and decline from 2024 to 2026 and over the life of mine, with an exception of an unusually high grade year with WB5 ore. Hence, while there was previously an outlook for Kinross to be one of the best growth stories among its peer group, the expected dip in grades at Tasiast combined with the sale of Udinsk means that production should be flat to down from 2023-2026 even despite production growth at Fort Knox.

West Branch Mine Production & Grades (Company Presentation)

Costs & Margins

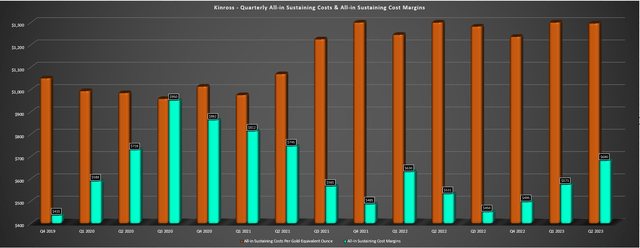

Moving over to costs and margins, Kinross reported all-in sustaining costs [AISC] of $1,296/oz in Q2 2023, an improvement from $1,341/oz in Q2 2022 and $1,321/oz in Q1. And like some other producers, Kinross noted that it’s seeing some easing of inflationary pressures with benefits from lower oil prices, but that there are some offsets, mainly labor/contractor inflation which has been called out elsewhere in the sector, and higher royalties (gold price). Still, this improved cost performance on the back of strong quarters from Tasiast, Paracatu and from a lesser degree La Coipa helped the company to see a significant increase in AISC margins ($680/oz vs. $531/oz) and we also saw a material improvement in its financial results and position. This was evidenced by net debt declining to ~$2.0 billion at quarter-end, benefiting from a $40 million deferred payment from the Russian asset sale, and it paid down $200 million on its RCF in the quarter.

Kinross Gold – Quarterly AISC & AISC Margins (Company Filings, Author’s Chart)

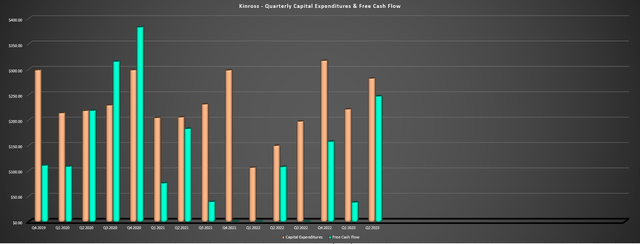

As for Kinross’ financial results, we saw a significant increase in operating and free cash flow year-over-year to $528.6 million and $246.7 million, respectively (Q2 2022 free cash flow: $107.7 million) benefiting from the higher average realized gold price. This has pushed trailing twelve month free cash flow to ~$420 million, and this is despite higher capital expenditures over the past 12 months with spending at Tasiast 24k and development work at Manh Choh with key operating permits received in May. As for Q2 specifically, free cash flow more than doubled despite higher capex ($281.9 million vs. $149.4 million), an impressive feat, especially relative other producers. So, with the gold price continuing to hang out above $1,900/oz and a solid H2 on deck, Kinross’ should make continued progress on de-leveraging which could help its more depressed multiple relative to peers with stronger balance sheets. Let’s take a look at Kinross’ valuation:

Kinross – Quarterly Capex & Free Cash Flow (Company Filings, Author’s Chart)

Valuation

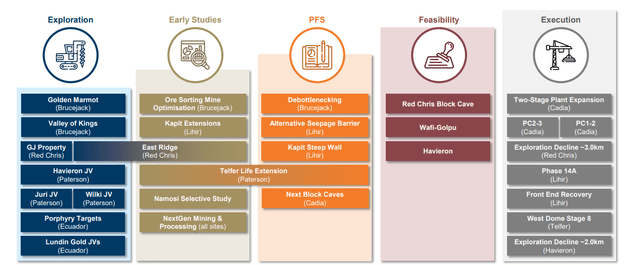

Based on ~1,230 million fully diluted shares and a share price of US$4.95, Kinross trades at a market cap of ~$6.1 billion and an enterprise value of ~$8.1 billion. This makes it one of the cheapest multi-million ounce producers on an enterprise value basis, with it trading at less than half the valuation that recently offered for Newcrest (OTCPK:NCMGF), explaining why Endeavour Mining (OTCQX:EDVMF) made an opportunistic bid for the company. That said, while Kinross may have scale, it is a much higher-cost producer than Newcrest; it lacks Newcrest’s long mine lives on balance, and it doesn’t have nearly as strong a development pipeline, with Newcrest arguably having three world class assets in the wings, including Wafi-Golpu (negative AISC on a by-product basis), Red Chris Block Cave (negative AISC on a by-product basis), and Havieron (70%). Finally, Newcrest benefits from a more attractive jurisdictional profile, with most of its largest assets in Tier-1 jurisdictions (Cadia, Telfer/Havieron, Brucejack).

Newcrest Development Pipeline (Newcrest Presentation)

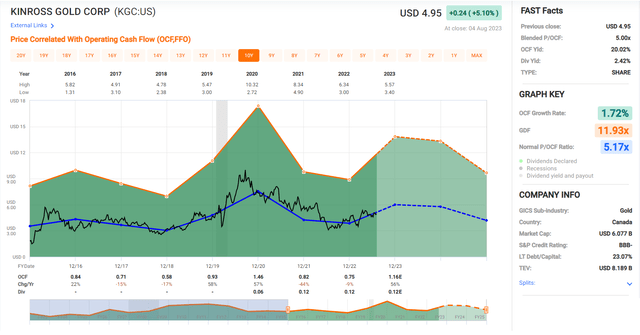

That said, and even when adjusting for Kinross’ inferior jurisdictional and cost profile and less robust development relative to Newcrest, the stock remains very reasonably valued despite its recent outperformance. This is based on it trading at just ~4.3x conservative FY2024 cash flow per share estimates of $1.13, and it’s even more undervalued when we compare it to smaller producers like Evolution Mining (OTCPK:CAHPF). And even if we apply only a 20% premium to Kinross’ 10-year average cash flow multiple (6.2 vs. ~5.15) to reflect its improved jurisdictional profile (Chirano + Russian assets divested) and an improved development pipeline (Great Bear Project) offset by a track record of declining per share metrics, this would translate to a fair value for Kinross of US$7.00. Measuring from a current price of US$4.95, this translates to a 41% upside to fair value even using more conservative FY2024 estimates.

Since Q2 2013, Kinross’ quarterly production has declined by 15% while its share count has increased by ~8%, even with the benefit of this being a much stronger year at Tasiast.

Kinross Gold – Historical Cash Flow Multiple (FASTGraphs.com)

Although this is an attractive upside, I prefer a minimum 40% discount to fair value to justify buying mid-cap producers with less than 60% of production from Tier-1 jurisdictions, and if we apply this discount to Kinross, its ideal buy zone moves up from US$4.00 previously to US$4.20 or lower. So, while there’s no disputing that there’s upside here if gold prices can continue to cooperate and the company can continue to de-leverage, I don’t see enough margin of safety to justify paying up for the stock at US$4.95. Obviously, just because I don’t see the valuation as compelling enough here doesn’t mean that the stock can’t go higher, but I prefer to buy stocks when they’re hated and trading at massive discounts to fair value, and while this was the case at US$3.40 last year, I don’t see nearly as meaningful of a margin of safety at current levels.

Kinross – June 2022 Update (Seeking Alpha Premium)

Summary

In a surprising change relative to past years, Kinross put up one of the stronger quarterly performances among the million-ounce producers and looks to have positioned itself well to deliver into FY2023 guidance of ~2.1 million GEOs at $1,320/oz. Meanwhile, the company has done a solid job of balancing opportunistic share buybacks and debt repayment, offsetting the dilution from the Great Bear acquisition and continues to reduce its net debt after another solid quarter financially in Q2 (albeit with significant help from the gold price). This has certainly improved the investment thesis, and Kinross’ valuation is certainly attractive relative to producers like Evolution Mining that have outperformed their peers. That said, I still don’t see enough margin of safety, and if one digs through the rubble, I continue to see better opportunities. So, while I would become interested below US$4.20, I remain neutral short term on Kinross stock.

Read the full article here