The REIT Investment Thesis Is Even Better At These Beaten Down Valuations & Prices

We previously covered W. P. Carey (NYSE:WPC) in June 2023, discussing its CPI-tied rental escalator and consequently, the safety of its top/ bottom lines and dividend growth. With the REIT stock already moderated from its hyper-pandemic prices, we had rated the stock as a great income Buy then.

On the one hand, WPC has reported another excellent double-beat FQ2’23 performance, with revenues of $452.57M (+5.7% QoQ/ +31.4% YoY) and AFFO per share of $1.36 (+3.8% QoQ/ YoY).

On the other hand, its AFFO margin has further declined to 64.8% (-0.4 points QoQ/ -9 YoY) by the latest quarter, with much of the profitability headwind attributed to the accelerating operating expenses of $231.68M (-6.1% QoQ/ +24% YoY).

While 85% of WPC’s debts (+3 points QoQ/ +1 YoY) are on fixed interest rate with a weighted average interest rate of 3.2% (+0.2 points QoQ/ +0.7 YoY) in FQ2’23, it is apparent that the net effect has been negative as well.

This is due to the rising interest expenses of $75.48M (+12.3% QoQ/ +62.6% YoY), thanks to the expanding long-term debts of $8.61B (+4.3% QoQ/ +27.3% YoY) by the latest quarter.

Therefore, while the WPC management has maintained their FY2023 AFFO guidance per share of $5.35 at the midpoint (+1.1% YoY), we are not overly impressed for now, since its margins have been underwhelming of late.

For now, based on its AFFO per share guidance and historical payout ratio of ~80%, investors may still see a decent full year payout of $4.28 (+1% YoY).

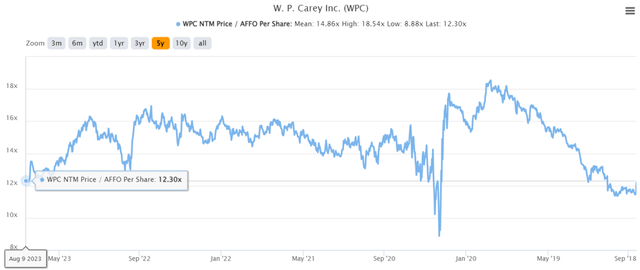

WPC 5Y Price/ AFFO Per Share Valuations

S&P Capital IQ

Despite the mixed prospects discussed above, we believe that WPC’s NTM Price/ AFFO Per Share valuations have been overly moderated to 12.30x, compared to its 1Y mean of 14.40x and pre-pandemic mean of 16.10x.

The pessimism embedded in its valuations are surprising indeed, since market analysts still expect the REIT to grow its profitability from FY2022 AFFO per share of $5.00 to FY2025 levels of $5.65, expanding at a CAGR of +2.2%, compared to pre-pandemic levels of -0.8%.

While some analysts may have priced in the Fed’s pivot in 2024, potentially impacting WPC’s lease income and AFFO generation, we are not overly concerned yet, since it may take a few quarters for the effect to trickle down.

In addition, the management has strategically allocated its lease contracts with 43% comprising fixed rental escalators and 54% tied to the inflation index in FQ2’23, demonstrating its well-diversified offerings that will perform well in both low and high inflationary rate environments.

Combined with a weighted-average lease term of 11.2 years (+0.3 years QoQ/ -0.2 YoY), a stable occupancy rate of 99.0% (-0.2 points QoQ/ -0.1 YoY), and excellent rental collection rate of >90% in the latest quarter, there is no danger to WPC’s top and bottom line performance in the intermediate term.

We believe that the management’s execution and risk management have been stellar as well, since the REIT has successfully collected most of its rents at an impressive rate of over >90% even during the worst of the pandemic, with similar occupancy rates spread across different tenant industries.

While there has been some concerns about remote work, investors must also note that office properties only comprise 16.1% of WPC’s portfolio (-1.1 points QoQ/ -2.6 YoY), with many tech companies already mandating employees to largely return to the office, including Apple (AAPL), Amazon (AMZN), Disney (DIS), and most interestingly, Zoom (ZM).

Therefore, while expenses may have accelerated, we believe WPC’s FY2023 profit target is still largely achievable. However, investors may also want to temper their expectations a little, since without the CPI rental growth contribution, we may see the REIT’s performance decelerate from those observed over the past few quarters.

So, Is WPC Stock A Buy, Sell, Or Hold?

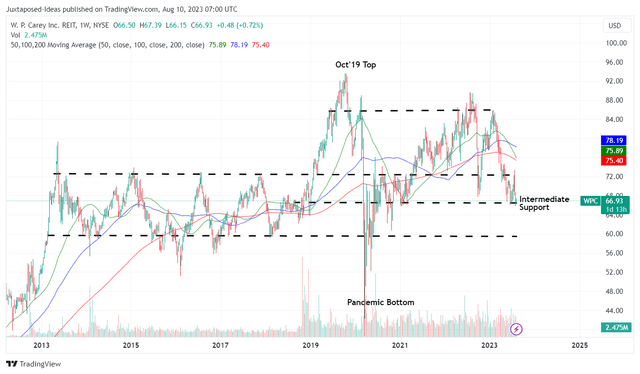

WPC 10Y Stock Price

Trading View

Therefore, we believe that Mr. Market’s drastic correction has provided opportunistic investors with an expanded forward dividend yield of 6.43%, compared to its 4Y average of 5.59% and sector median of 4.34%.

As a result of the attractive risk reward ratio, we continue to rate the WPC stock as a Buy, with a recommended accumulation range of between $60 and $66, depending on individual investors’ dollar cost averages.

Then again, we believe that current levels of $66 already provide an excellent entry point, since these levels have also been well supported since June 2021.

Therefore, it is unlikely that the WPC stock may return to its pre-pandemic trading range of between $60 and $72, especially given the highly competent management team and the healthy balance sheet.

Read the full article here