Last week, Aviva (OTCPK:AIVAF) (OTCPK:AVVIY) reported its H1 financial results. Here at the Lab, we have covered the stock twice already in 2023, and we suggest that our readers check up on our past analysis so that they are well acquainted with the story up to now:

- FY 2022 results: Aviva Is Delivering;

- Q1 2023 results: Solid Q1, Time To Buy More.

No buy case recap today, and before commenting on the latest financial release, it is important to recap the recent disappointment in Aviva’s stock price performance. Since our buy, Aviva shares are down by almost 7% (with its tasty DPS, we arrived at a total return of minus 2%). Interestingly enough, Aviva’s stock price depreciation was not paired with a fall in profit (and also lower Wall Street expectations). Jumping to the conclusion, today we reiterated our buy rating, and in our next paragraph, we follow up on Aviva, including the company’s latest financial performance.

Mare Past Analysis

Q2 Results

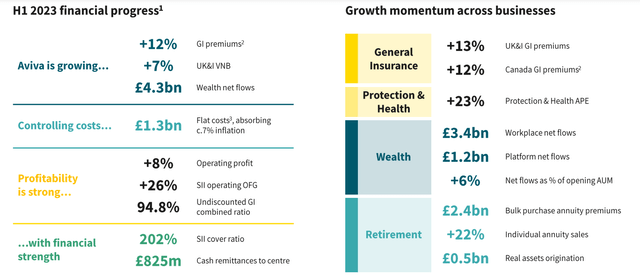

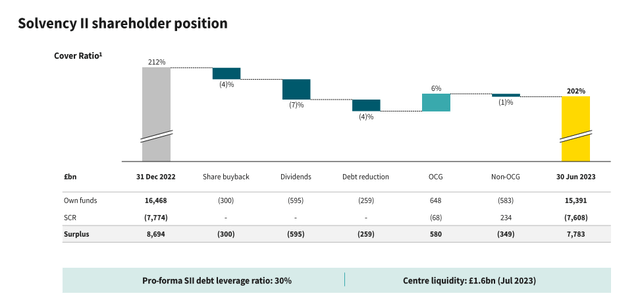

Starting with the General Insurance gross written premiums were up by 12% to £5.27 billion compared. A strong performance was recorded in the UK (where the company is the market leader). In numbers, the UK & Ireland division was up 13% to £3.21 billion. This was mainly due to the new product offering. Going down to the P&L analysis, what is critical to emphasize is the cost evolution. Despite inflation (very high in the UK vs. EU and USA), the company managed to control its cost basis and recorded in absolute value flat expenses (£1.34 billion both in H1 2023 and in H1 2022). In number, Aviva managed to absorb 7% of inflationary pressure. Group operating profit reached £715 million, and EPS was up by 10% on a yearly comparison thanks to Aviva’s operating leverage. Looking at the balance sheet and solvency ratio, the company reached 202% with a solid center liquidity of £1.6 billion compared to £2.2 billion in FY 2022 comments. This was due to dividend payments, buyback completion, and ongoing debt repayment.

Aviva H1 Financials in a Snap Aviva H1 Main Highlights

Source: Aviva Q2 results presentation

Why are we still over-weighing Aviva?

Despite a stock price decline, we still believe Aviva is a solid investment call. Aside from the company’s latest financial performance, we should recall that Aviva is emerging into a transformation story with an improving cash flow trajectory, higher shareholders remuneration, and a path to strengthen its balance sheet. Aviva’s business model simplification will likely generate sustainable long-term results. Here are our primary evidence and critical forward-thinking highlights:

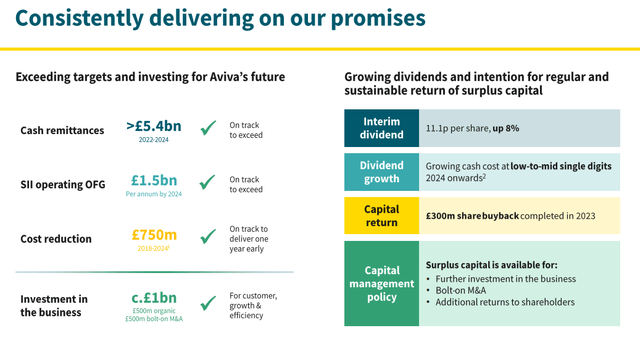

- With a continued focus on cost efficiency, the company confirmed its 2024 saving target of £750 million. However, looking deeper into the results, there was a cost target acceleration. Therefore, Aviva might surprise Wall Street to the upside;

- Aviva recorded higher-than-expected results thanks to investment returns in the UK and Canada. Despite that, at the aggregate level, operating profit included one-off benefits from lower claims (PYD) and favorable weather conditions. According to our estimates, excluding PYD and weather, operating earnings would be £140 million lower. Here at the Lab, we expected a normalization trend over H2, but we also confirmed our operating profit of £1.6 billion in 2023. In addition, in the future, thanks to the new product offering, we believe that Aviva will include these new initiatives in other countries;

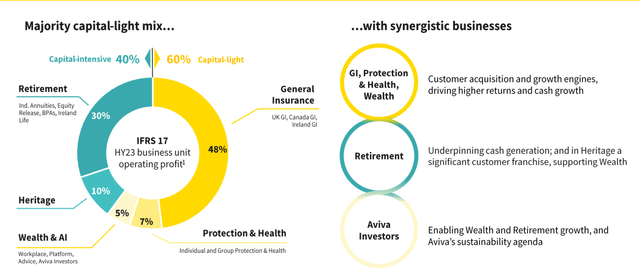

- Aviva is building momentum and accelerating growth in its asset-light business with expected synergetic businesses (insurance and Wealth in particular);

- There was no change in the 2023 dividend projection, and the company confirmed an interim DPS up 8% to 11.1 cents (it was 10.3p in H1 2022). Buyback, in line with our expectation, was also executed in the first half (total amount was £300 million);

- On the balance sheet, the Solvency metric was +3 basis points higher than consensus expectation, but the key metric is the solid capital generation with cash remittances at £825 million, exceeding the average consensus by 9%;

- Aviva is on track to achieve its >£5.4bn cumulative cash remittances target in the next two-year period with a higher operating profit between 5-7% on a yearly basis;

- Aviva’s leverage was at 32% in H1, 30% on a pro-forma basis.

Aviva asset-light business Aviva organic and inorganic capital deployment evolution

Conclusion and Valuation

Let’s keep in mind our last conclusive paragraph:

We are estimating this additional share repurchase assuming Aviva will meet its business targets thanks to a solid pricing momentum in General Insurance and controllable cost inflation. Our internal team estimates a buyback limit when the Solvency ratio is close to 180%. However, given the strong cash generation performance, there is flexibility in its central liquidity. To sum up, the company is growing and delivering its diversified business model. Capital position remains solid, and Aviva focuses on sustainable shareholders remuneration“.

Looking at the Q2 results, we were well in line with the company’s performance. In H1, Aviva paid its dividend and completed the share buyback program. There are now a few possibilities: 1) M&A optionality, 2) higher shareholders remuneration (including a new buyback plan), and 3) a deleverage plan. At this stage, we are not forecasting (or speculating) on M&A, and we also believe that Aviva will focus its attention on its internal growth engine. Therefore, we are more inclined towards points 2) and 3). In addition, our estimates forecast a +5% DPS growth per year in our forecasted visible period (until 2026), combined with our 2023 debt reduction of £300 million. We were already above Wall Street consensus in Q1, and after the solid Q2 results with positive guidance (slightly increased by the company), we decided to leave our target price set at £5 per share ($12 in ADR). Our valuation is supported by a P/E of 8x in line with peers such as Aegon. Here at the Lab, we apply a 20% discount versus players such as Allianz, AXA, Zurich, and Generali. Aviva’s valuation is also supported by a price-to-book value 1.2x vs. a historical average set at 1.5x. After the H1 results, we are still confident in Aviva’s stock price appreciation opportunity; earnings and the payout ratio are increasing. Insurers tend to geared movements in equity and debt markets. The company is sensitive to catastrophe-related losses. In addition, the company carries significant credit default risk in its investment portfolio.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here