Introduction

Alkermes (NASDAQ:ALKS) is a global biopharmaceutical firm with a focus on neuroscience and oncology. Headquartered in Dublin, Ireland, with facilities in the US, it offers solutions for alcohol dependence, opioid dependence, schizophrenia, and bipolar 1 disorder. In November 2022, Alkermes announced a plan to split its neuroscience and oncology businesses. This separation, set for 2023, would birth a new entity, “Mural Oncology”, dedicated to cancer therapies, while Alkermes continues its neurological focus.

The following article details Alkermes’ recent financial performance, highlighting strong revenue growth and the promising potential of the drug Lybalvi. I also discuss the strategic separation of their neuroscience and oncology divisions.

Q2 2023 Earnings

Looking at Alkermes’ most recent earnings report, the company reported a significant surge in total revenues to $617.4M, a rise attributable in large part to $248.4M in back royalties from arbitration with Janssen. Sales of proprietary products rose 21% to $231.5M. Specifically, Vivitrol (opioid dependence and alcohol dependence) sales increased by 6% to $102.1M, Aristada (schizophrenia) saw a 10% growth to $82.4M, and Lybalvi (bipolar 1 disorder and schizophrenia) experienced a substantial growth of 134% to $47M. Operating expenses grew to $378.2M, primarily from the Lybalvi launch and the oncology business separation. Within these expenses, R&D reached $100.8M and SG&A was at $205.3M. GAAP net income stood at $237.1M, a turnaround from the prior year’s net loss, while non-GAAP net income was $94.3M.

Liquidity, Assets, & Debt

Turning to Alkermes’ balance sheet as of June 30, 2023, the company boasts cash and cash equivalents of $665.8M, short-term investments of $163.3M, and long-term investments of $78.1M, aggregating to $907.2M. After adjusting for the one-time revenue boost of $248.4M from arbitration with Janssen, the net cash used by operating activities over the past six months is -$53.2M, equating to a monthly outflow of roughly $8.87M. Using this metric, the company has an implied runway of approximately 102 months (or 8.5 years) based on its present cash and investments. However, this estimation is simplistic, not accounting for possible variances in expenses, other revenue sources, or unforeseen costs. Overall, Alkermes demonstrates robust liquidity, underlined by its sizable current assets and manageable long-term debt of $289M. However, it’s imperative to monitor the company’s cash flow moving forward, ensuring sustained financial stability.

Valuation, Growth, & Momentum

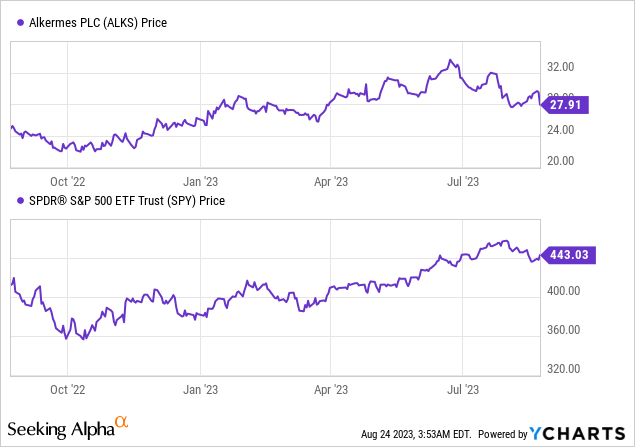

According to Seeking Alpha data: Alkermes possesses a capital structure that includes a modest debt level relative to its market capitalization, while holding a significant amount of cash. The enterprise value stands at $4.47B. In terms of valuation, the forward P/E and EV/EBITDA indicate a relatively high valuation, although revenue growth has been robust with a projected increase of +45.91% in 2023, despite an anticipated decline of -6.47% in 2024, followed by a rebound in 2025. The earnings revision trend is overwhelmingly positive, with FYQ1 experiencing upward revisions exclusively. From a stock momentum perspective, Alkermes outperformed the S&P 500 over a 9-month and 1-year period, albeit showing some recent softness in the 3-month view.

Lybalvi: Weighing Benefits Without The Weight

Lybalvi’s robust growth of 134% YoY signifies its emerging prominence in the pharmaceutical sector, especially concerning treatments for bipolar 1 disorder and schizophrenia. At its core, Lybalvi combines olanzapine, an established antipsychotic, with samidorphan, aiming to balance olanzapine’s proven efficacy with the need to control its associated side effects, notably weight gain.

Weight gain, especially when coupled with increases in waist circumference, presents significant health concerns. These aren’t just cosmetic issues – they’re established risk factors for cardiovascular diseases and diabetes. In psychiatric care, the challenge has often been to balance therapeutic benefits with side-effect profiles. Many patients with bipolar or schizophrenia often deal with comorbidities, making it even more crucial to control additional risks introduced by medications.

The introduction of samidorphan to the treatment mix addresses this gap. By mitigating weight gain while retaining olanzapine’s therapeutic prowess, Lybalvi provides a dual advantage, making it a potentially game-changing drug for many patients. This can lead to enhanced patient compliance, as many individuals discontinue antipsychotic treatments due to undesirable side effects like rapid weight gain.

Analysts have previously estimated Lybalvi’s peak annual revenue to fall anywhere between $300 million and $700 million. Considering its unique therapeutic benefits, the indications it addresses, the current competitive landscape with generic options (but with the associated side effects), and its sales trajectory to date, I’m inclined to believe that Lybalvi could surpass the higher end of these projections.

In conclusion, Lybalvi’s potential goes beyond its current sales growth. Its unique approach to balancing efficacy with a reduced side-effect profile underscores its importance as a potential front-runner in treating bipolar 1 disorder and schizophrenia. Future studies might delve deeper into long-term impacts and other potential benefits, solidifying its position in the therapeutic landscape.

Lybalvi’s Commercial Expansion: A Growth Catalyst

Management is pushing forward with a multifaceted approach to growth. One of their main thrusts is expanding the commercial reach of Lybalvi, an oral medication. Its recent launch into the market is promising, and they are boosting its visibility with a Direct-to-Consumer campaign. On the legal front, there’s anticipation around resolving the Vivitrol litigation, but given potential legal intricacies, the strategy for the drug might remain steady for the next couple of years. Meanwhile, the company is making significant strides in research and development, notably with ALKS 2680. They’ve initiated studies to explore its impact on narcolepsy and are gearing up for further clinical explorations. Lastly, the spin-off of the Mural Oncology business is a major strategic move. With Dr. Caroline Loew at the helm, they’re poised to create a dedicated and dynamic entity focusing solely on oncology. All in all, the management seems to have its hands full with initiatives aimed at solidifying its market position and paving the way for future growth.

My Analysis & Recommendation

In light of the recent developments surrounding Alkermes, investors find themselves at a pivotal juncture. The decision to partition the neuroscience and oncology segments appears to be a strategic move designed to harness the maximum potential of each business unit. With the inception of “Mural Oncology,” Alkermes evidently seeks to drive sharper focus and specialization within its oncology arm, creating a distinct platform to expedite breakthroughs in cancer treatments. For Alkermes investors, this bifurcation indicates an opportunity to participate in the growth of a new, dedicated entity, while still partaking in the promising neurological pipeline Alkermes continues to push.

Speaking of promise, Lybalvi is an epitome of the same in the neuro portfolio. This drug’s dual capacity to mitigate side effects, particularly weight gain, while maximizing therapeutic benefits makes it a standout in the bipolar and schizophrenia treatment domain. If its sales trajectory and unique advantages are any indication, Lybalvi may very well transform into a revenue powerhouse for Alkermes in the foreseeable future.

Yet, for investors plotting their next move, the coming weeks and months warrant close observation. While the financials exhibit robust growth, the projected revenue dip in 2024 should be of concern, even if temporary. The liquidity position, bolstered by a sizable cash pool and manageable debt, is a comfort, but it’s vital to keenly scrutinize cash flow patterns. Additionally, with Lybalvi’s commercial expansion, Alkermes is primed for more market penetration, but the impending Vivitrol litigation may introduce an element of unpredictability.

Finally, as Alkermes navigates this significant business transition, there’s an undercurrent of change, anticipation, and opportunity. Given the strength and potential of the neuro portfolio, along with the promising trajectory of Lybalvi and the strategic separation of the oncology division, I’m optimistic about Alkermes’ future prospects. Therefore, my recommendation for Alkermes’ stock at this juncture is a “Buy.” I believe that the company’s recent developments and forward-looking vision set the stage for significant growth, making it an attractive investment opportunity.

Risks to Thesis

When the facts change, I change my mind.

While I recommend a “Buy” for Alkermes, several factors could contradict this stance:

- Business Division: While the separation of neuroscience and oncology might streamline operations, there’s a risk that the split could dilute branding, lead to operational inefficiencies, or result in loss of synergies between the two units.

- Future Sales Projections: My projection for Lybalvi surpassing peak annual revenue estimates might be overly optimistic. Clinical setbacks, competition, or unforeseen side effects could hinder growth.

- Revenue Decline: The anticipated revenue dip in 2024 is a concern. A temporary dip might deter short-term investors and impact stock momentum.

- Legal Hurdles: The outcome of the Vivitrol litigation is unpredictable and could negatively impact the financial position and reputation of Alkermes.

- Competitive Landscape: The market might witness the introduction of other drugs that either compete directly with Lybalvi or offer better efficacy/safety profiles.

- Management Challenges: Navigating the company through significant changes requires strong leadership. Any missteps can be detrimental.

- Valuation Concerns: The relatively high forward P/E and EV/EBITDA might indicate that the stock is overvalued.

Read the full article here