Executive Summary

Cigna Group (NYSE:CI) has emerged as a standout performer in the managed care industry, demonstrating a remarkable history of long-term earnings per share (EPS) growth. Despite initial skepticism following a contentious merger with Express Scripts, the company has successfully navigated its post-merger phase, solidifying its position as a reliable player in the healthcare sector. CI’s ability to outperform its own guidance underscores its potential for sustained growth.

Business Overview

Cigna operates through three distinct segments: Evernorth, Cigna Healthcare, and Corporate & Other. Evernorth, the largest segment, encompasses Pharmacy Benefit Services (including Express Scripts), Specialty Pharmacy, and Care Services. Notably, Evernorth anticipates steady revenue and earnings growth, with an upward bias fueled by the faster-growing Specialty Pharmacy and Care Services units. Meanwhile, Cigna Healthcare primarily focuses on the high-margin U.S. Commercial business, boasting an Administrative Services Only (ASO)-heavy approach. This approach, wherein self-funded clients bear the risk of medical costs, positions CI as a key player in this space. Around 84% of CI’s commercial lives operate under ASO arrangements, providing greater earnings stability compared to peers. Additionally, Cigna has a modest U.S. Government business and an International Health segment, contributing to the company’s diversified revenue streams.

Segments (Cigna)

The key to Cigna’s business model lies in its diversification across segments. This mitigates the risk associated with over-reliance on any one area of healthcare, positioning the company to adapt to changing market dynamics and capitalize on emerging opportunities. Furthermore, CI’s extensive portfolio allows it to cater to a broad customer base, ranging from individual consumers to large corporate clients. This diverse revenue stream not only provides stability but also sets the stage for continued expansion in both established and emerging markets.

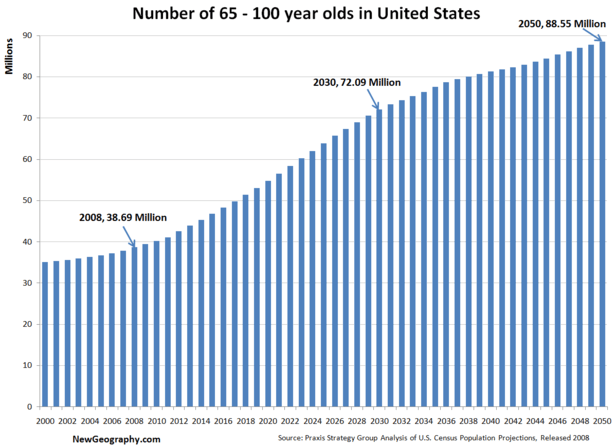

Moreover, Cigna benefits from important business and industry tailwinds, namely, aging population. The United States is currently undergoing a profound demographic transformation. According to the U.S. Census Bureau, the population of individuals aged 65 and older is projected to nearly double over the next three decades. By 2050, it is estimated that nearly 23% of the U.S. population will be aged 65 or older, compared to approximately 16% in 2020. This demographic shift signifies an increased demand for healthcare services, particularly those related to age-related conditions and chronic illnesses.

An aging population is associated with a notable increase in healthcare expenditures. According to the Centers for Medicare & Medicaid Services (CMS), approximately 60% of an individual’s lifetime healthcare expenditures occur after the age of 65. This trend is largely driven by the higher prevalence of chronic conditions and the need for more extensive medical care in older age groups.

Aging Data (US Census)

Cigna’s diversified service offerings, including specialized programs for chronic condition management and access to a broad network of healthcare providers, position the company as a crucial player in addressing the unique healthcare needs of the elderly population. Through its Evernorth segment, Cigna provides essential pharmacy benefits and specialty pharmacy services that are particularly vital for older individuals managing complex medication regimens.

While Medicare is a pivotal component of healthcare coverage for seniors, Cigna’s broad range of services extends beyond Medicare. The company’s managed care solutions cater to various stages of aging, providing a comprehensive continuum of care that includes preventive measures, disease management, and specialized healthcare services tailored to individual needs.

From a financial perspective, an aging population offers a lucrative opportunity for Cigna. As older individuals typically require more extensive healthcare services, this demographic shift contributes to a sustained demand for healthcare coverage. This steady demand not only supports Cigna’s existing business operations but also creates potential for further growth and expansion.

Competitive Advantage

Cigna leverages several key advantages to maintain its competitive edge. First, Cigna’s emphasis on high-growth assets within the Evernorth segment positions it for sustained expansion. The strategic focus on areas like Specialty Pharmacy and Care Services, which exhibit above-average growth rates, is a testament to the company’s forward-thinking approach. This commitment to innovation and growth ensures that CI remains at the forefront of industry trends, allowing it to capture additional market share and drive revenue growth.

The successful implementation of the Cross-Enterprise Leverage strategy demonstrates the company’s ability to optimize synergies across its various business units, driving further growth. By capitalizing on the strengths of both Evernorth and Cigna Healthcare, the company can offer integrated solutions to clients, creating additional value and solidifying customer relationships.

Additionally, Cigna’s ASO-heavy approach in the U.S. Commercial business provides a unique competitive advantage. This model not only enhances earnings stability but also offers clients a cost-effective solution to managing healthcare expenses. By acting as a processor rather than an insurer, CI can provide valuable administrative services, while clients assume the risk of medical costs. This approach has resonated with clients and contributed to CI’s industry-leading position in this segment.

Valuation

A conservative valuation approach, based on industry transactions, supports an intrinsic value estimate of at least $370 per share for Cigna. This valuation methodology takes into account both the historical multiples paid for similar businesses and CI’s unique position within the industry. The resulting estimate implies a 15x the current 2023E EPS guidance, suggesting significant upside potential for investors.

Notably, CI trades at a discount relative to its peers, presenting an attractive opportunity for those seeking exposure in the healthcare sector. This valuation gap is reflective of both the market’s initial skepticism following the Express Scripts merger and a potential undervaluation relative to the company’s earnings potential. For investors seeking a compelling entry point into a fundamentally strong company, CI’s current valuation presents an enticing opportunity.

Additionally, Cigna offers a nearly 2% dividend yield, enhancing its appeal to income-oriented investors. This dividend, combined with the company’s share buyback program, further underscores CI’s commitment to returning value to shareholders. As the company continues to generate strong cash flows, there is potential for further dividend increases, providing investors with an attractive income stream.

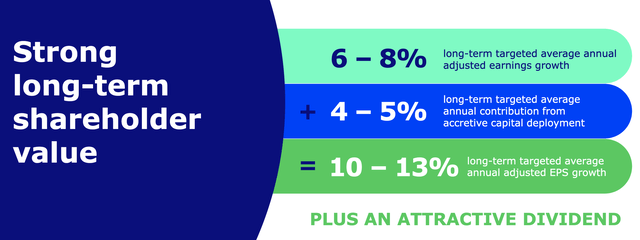

Long term growth algorithm (Cigna)

Conclusion

Cigna’s exemplary track record of exceeding growth targets, coupled with its well-executed strategic initiatives, positions it as a compelling investment opportunity within the managed care industry. The company’s commitment to capital efficiency, diversified revenue streams, and prudent allocation of resources underscores its potential for sustained outperformance. While potential risks, such as economic uncertainties and shifts in healthcare policies, persist, Cigna’s proven track record and strategic positioning suggest a promising future for investors seeking exposure in the healthcare sector.

By capitalizing on demographic shifts, optimizing synergies across segments, and maintaining a disciplined approach to capital allocation, Cigna stands poised for continued success in the years ahead. As always, investors should conduct thorough due diligence and consider their individual risk tolerance before making any investment decisions. With Cigna’s strong competitive position, diversified business model, and prudent financial management, it represents a compelling opportunity for investors seeking exposure to the dynamic and evolving healthcare sector.

Risks and Challenges

Investing in Cigna offers substantial potential, yet it’s essential to acknowledge and address potential risks:

1. Regulatory

The healthcare industry is highly sensitive to regulatory changes. Alterations in government policies, reimbursement rates, or compliance requirements can significantly affect CI’s operations and financials. This uncertainty can lead to market volatility and impact the stock price.

2. Competitive Pressure

The managed care sector is fiercely competitive, with ongoing consolidation. Emerging technologies and new entrants can alter industry dynamics. Adapting to these shifts is crucial for CI to maintain market share and pricing power.

3. Recession

Cigna’s performance is tied to economic conditions. Downturns or recessions can lead to reduced spending on healthcare services and insurance. Interest rate fluctuations impact investment income and portfolio valuation. Economic challenges also influence employer-sponsored health insurance enrollment.

Vigilant monitoring of these risks is essential, as they can significantly influence CI’s financial performance and market standing. Proactive management and adaptability to industry trends will be critical in mitigating potential negative impacts.

Read the full article here