Investment Thesis

Werner Enterprises (NASDAQ:WERN) seems to be trending down financially. I wanted to take a look at the company’s overall financial position and see what kind of growth in revenues is achievable over the long run, now that the world is back to pre-covid levels of activity. I believe right now, the company is trading at a premium, and I would like to see a pullback in the next half of the year as I believe the volatility and deteriorating margins may bring a better entry point, therefore, I give the company a hold rating until I see financials improving.

Comments on Outlook

As you’ll see in the next section, the company managed to grow revenues significantly in the last two years. This is likely not sustainable and was driven by inventory and demand buildup from the pandemic. Inventory levels are beginning to normalize or are already at the pre-pandemic levels according to the management of the company, meaning the next revenue growth will not be as robust as it has in the past two years. I would expect the company to see revenue growth like it had averaged in the last decade, which I will also touch on in the next section.

The industry outlook looks to be in the range of 3%-5% according to the research, which matches what the company managed to achieve in the last decade. I don’t think the company would be able to outperform the average in my opinion.

Financials

As of Q2 ’23, the company had $46m in cash, against $636m in long-term debt. How bad is this position? Let’s take a look at the company’s interest coverage ratio. Historically it’s been very healthy, however, in the past the long-term debt has been slightly lower. Back in Q2 ’22, the company’s interest expense on debt was around $3m on around $440m of debt, now the extra debt that the company took on increased the interest on it to a whopping $16m. The company’s interest payments are mostly dependent on that $400m debt that bears a variable interest rate of 6.43% while the remainder is fixed at 2.88% for $150m and 1.28% for $90m.

This has deteriorated the company’s financial position, however, as of Q2 ’23, the interest coverage ratio stood at around 6x, meaning EBIT can cover the annual interest on debt 6 times over. That is above the recommended level of 2x and also still above my more stringent requirement of 5x, so I can safely say the company is at no risk of insolvency right now. The company is very exposed to interest rate risk, however, there may not be many more hikes coming, and these may come down soon, but I wonder if an interest rate swap would be a good idea right now to fix the payments.

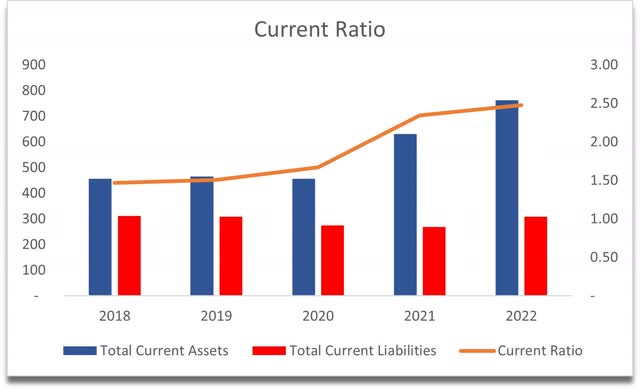

The company’s current ratio stood at around 2.5 as of FY22 and is down to around 1.9 as of the 2nd quarter of the year, which is even better in my opinion. I like to see companies being within the range of 1.5-2.0 as I believe this is an efficient current ratio, which strikes a good balance between the company’s ability to pay off short-term obligations and using its assets efficiently. The company has no liquidity issues.

Current Ratio (Author)

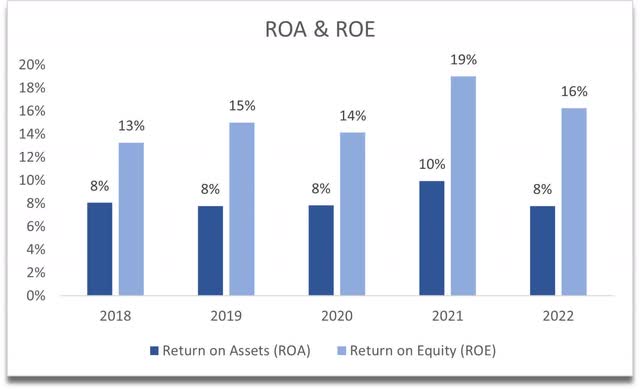

Speaking of efficiency, the company’s ROA and ROE have been quite decent historically, with a slight dip as of FY22, as these numbers came down to the company’s historical average by the looks of it. Nevertheless, the company is still achieving above my minimum of 5% for ROA and 10% for ROE. These may continue to come down further because as of Q2, net income is half of what it was in Q2 a year before.

ROA and ROE (Author)

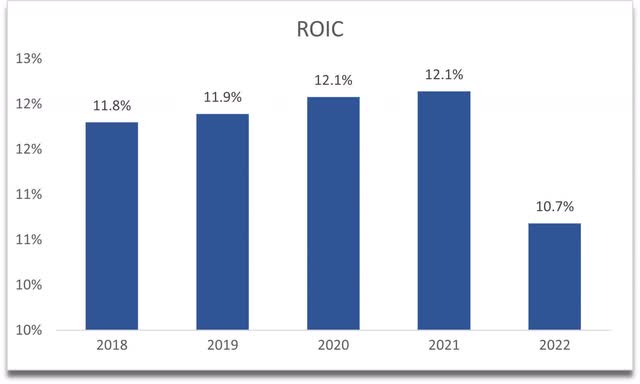

Historically, the company’s ROIC has been above my minimum of 10%, however, we can see that as of FY22 it has dropped quite a bit and I believe this will continue to trend down in FY23 because of increased costs.

ROIC (Author)

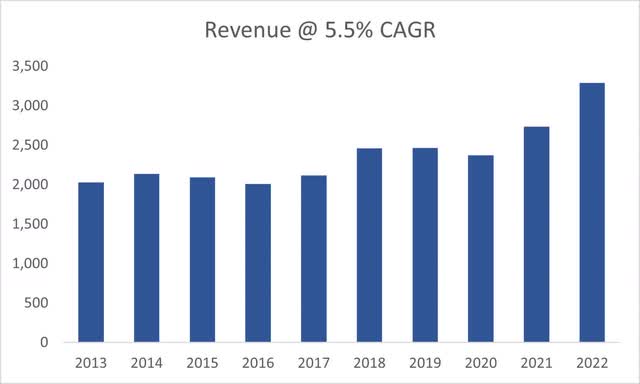

In terms of revenues, these have steadily grown by around 5.5% CAGR over the last decade, while in the two recent years, the company saw 15% and 20% growth, which I believe will come down because this growth seems to be spurred by the global opening after the pandemic, so I would expect the company to return to its historic average.

Average Revenue growth (Author)

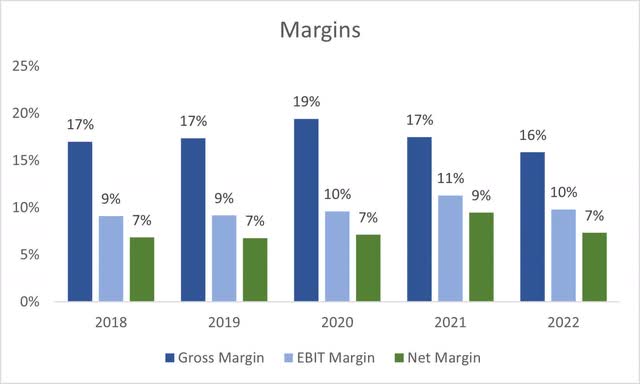

Margins saw slight declines over the last couple of years and it seems to continue down the same road as of Q2 ’23, however, quarterly numbers tend to fluctuate more, so I would like to see how these develop over the next 2 quarters. The website I use separates some expenses and categorizes them as COGS, while the company reports all of them as operating expenses, just an FYI.

Margins (Author)

Overall, historically, the company seems to be doing pretty well, while in the upcoming quarters, the company may see further deterioration in these metrics. I don’t expect these problems to last too long, however, I will add a larger margin of safety because there may be further volatility ahead of us still.

Valuation

I’m not going to trust the most recent revenue growth as I believe it is unsustainable. I will be on the conservative side of this, so for my base case revenue growth, I went with a 4% CAGR for the next decade, slightly below the company’s average growth rate to be on the safer side. For the optimistic case, I went around 8% CAGR, while for the conservative case, I went with 2% CAGRS to give myself a range of possible outcomes.

As for the margins, I see that analysts are expecting a 36% decline in EPS from the prior year and a 30% increase after that in FY24. I went ahead and anchored my assumptions to the FY23 and FY24 analysts’ estimates, then after that, I will improve margins slightly over time since companies tend to become slightly more efficient. The company will see around $7.5 a share of EPS in FY32 with these estimates, which is not too outrageous in my opinion as net margins will go from around 7% in FY22 to around 10% by FY32.

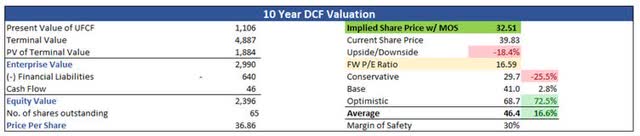

I believe there will be further volatility ahead that will increase costs and reduce margins in the short term, so I decided to add a 30% margin of safety on top of these assumptions. With that said, Werner Enterprises’ intrinsic value is $32.51 a share, implying the company is trading at an 18% premium to its fair value.

Intrinsic Value (Author)

Closing Comments

A FW PE ratio of almost 17 is I believe a little too expensive for such revenue growth and deterioration in margins. If it comes down to my PT, that will make the PE ratio go down to around 13.5, which is slightly more reasonable and would present a better risk/reward profile in my opinion.

I don’t think the volatility in the markets is going to go away soon, and in the short run, I expected some more price fluctuations driven by misses in earnings and reductions in margins fueled by increases in costs. I can see the company coming down to around $30 a share and if it does, I will reassess my thesis if the financials improve over the next couple of quarters and if the guidance is positive for the beginning of next year. Right now, I am going to stay put and assign a hold rating until everything improves.

Read the full article here