Investors in leading alternative asset manager Brookfield Asset Management Ltd. (BAM) have experienced a sharp upward reversal from its March 2023 lows, which initially saw BAM decline nearly 17% from its February 2023 highs before bottoming out.

However, dip buyers returned with conviction, helping BAM to bottom out decisively, and it hasn’t looked back since. While another selloff in May could have spooked investors momentarily, buyers held the $30 support zone robustly.

Given its well-diversified business model, I’m confident that the worst is likely over for Brookfield Asset Management investors, predicated on a predictable fee-based earnings stream. Furthermore, the company relies on “long-dated or permanent capital pools.”

Management held a wide-ranging Investor Day in mid-September, covering several areas in its business model and highlighting its leadership in infrastructure assets and its partnership with distressed credit specialist Oaktree. Notably, Brookfield Asset Management accentuated its focus to further bolster its “sticky fee streams” based on a long-dated capital base of 90% from the current 85%. As such, it aims to continue to deliver highly robust distributable earnings, providing substantial support for its dividend payouts.

Given its solid debt-free balance sheet, the company is well-primed for significant earnings growth from FY24. Management stressed that it remains on track to exceed $1T in fee-based capital over the next five years, indicating a 5Y CAGR of about 17.3%. The capital infusion is “expected to span all of BAM’s business lines.” Notably, near-term growth prospects are expected to remain solid, with management anticipating fee-based capital of $530B by the end of 2023, indicating a 27% YoY growth.

As such, I’m not surprised that analysts’ estimates on BAM are highly favorable. Accordingly, Brookfield Asset Management is projected to deliver a 13.7% CAGR in its distributable EPS from FY22-25. With FY23’s expected growth of about 5.1%, BAM could experience a sharp reacceleration in earnings growth over the next two years, supporting its distribution to investors.

I believe the market isn’t over-optimistic on the prospects of alternative asset managers like Brookfield Asset Management. The spotlight on these asset managers has risen since the regional banking crisis. Banks are expected to remain cautious, given uncertain macroeconomic conditions and a higher-for-longer Fed putting pressure on the long-duration fixed-income securities on their balance sheets. As such, leaders like BAM are well-positioned to capitalize on these opportunities, leveraging their expertise and well-recognized Brookfield ecosystem to deliver predictable and solid earnings growth for investors.

BAM’s valuation isn’t cheap but remains in line with its peers. It last traded at a forward distributable EPS multiple of about 23.7x. Market leader Blackstone stock (BX) last traded at a forward multiple of approximately 22.1x, while Ares Management stock (ARES) traded at a forward multiple of about 24.5x. Relative to its sector median of approximately 8.9x, they are priced for growth. As such, it’s critical to assess whether buying sentiments are robust enough, suggesting investors are still keen to lift its valuation, as they anticipate further upside moving ahead.

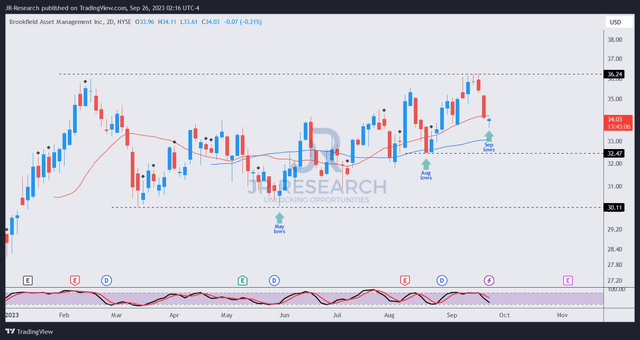

BAM price chart (2-Day) (TradingView)

As seen above, BAM has been making higher lows and higher highs, even though it faced stiff resistance at its September highs ($36.2 level). The selloff is justified, in line with the broad risk-off sentiments in September, as market operators reacted to the Fed’s “hawkish pause.”

However, I assessed that as long as BAM’s $32.5 support zone remains intact, BAM’s uptrend bias is expected to be supported. Dip buyers have also returned this week. While it’s too early to ascertain a robust consolidation zone, BAM’s solid earnings visibility and growth should help propel more momentum buyers to return.

As such, investors looking to partake in BAM’s opportunity can consider allocating their exposure in a few phases in anticipation of further downside volatility, leading to a potential re-test of its $32.5 level.

Rating: Initiate Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking and note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

We Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

Read the full article here