Tecnoglass (NYSE:TGLS) is a leading architectural glass manufacturer with vertically integrated operations based in the US, where 96% of its revenue comes from. The company has been a remarkable growth story over the last few years and continues to have high ambitions. Let’s dive into the company.

At a glance

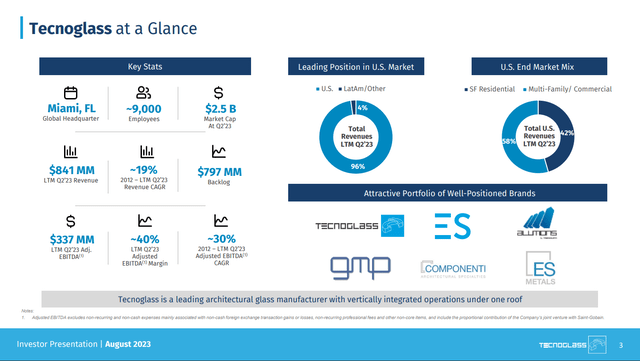

In the picture below, you can see an overview of Tecnoglass. The company has experienced rapid growth over the last decade at a 19% revenue CAGR and a 30% AEBITDA CAGR. In the past five years, the company started to push into the single-family residential market, which has grown to 42% of the business. Tecnoglass focuses primarily on the Southeast and Southcentral regions of the US, which are underpenetrated according to management. Tecnoglass has a healthy order backlog, close to their trailing twelve-month sales. Historically, 64% of multifamily/commercial backlog rolls off within 12 months and 97% within 18 months.

Tecnoglass at a glance (Tecnoglass Investor Presentation)

Low-cost producer

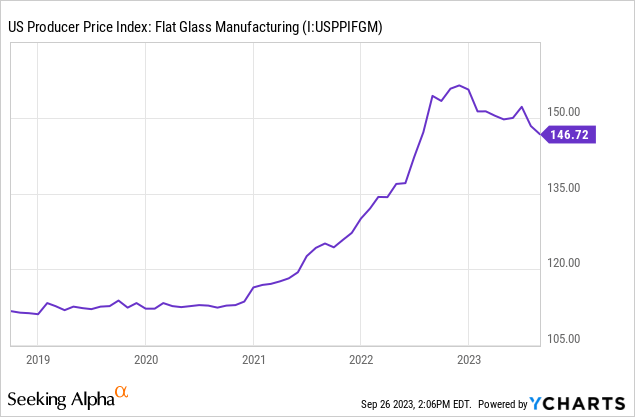

Tecnoglass has seen a massive surge in profits over the last few years. EBIT margin improved from 13% in 2019 to 32% in 2022. Part of this is the sharp increase in glass prices, displayed with the US Producer Price Index for flat glass.

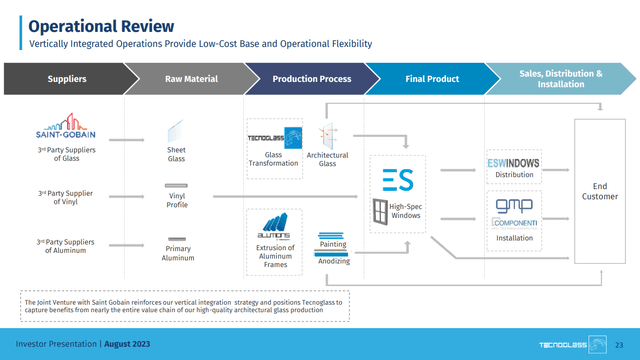

Another reason is the vertical integration Tecnoglass has invested in over recent years. Below, we can see that the company has internalized many of the steps in the value chain. This includes a joint venture with Saint-Gobain (OTCPK:CODGF) for the glass supplies. This led to a better cost structure and enabled higher margins.

Operational Review (Tecnoglass Investor Presentation)

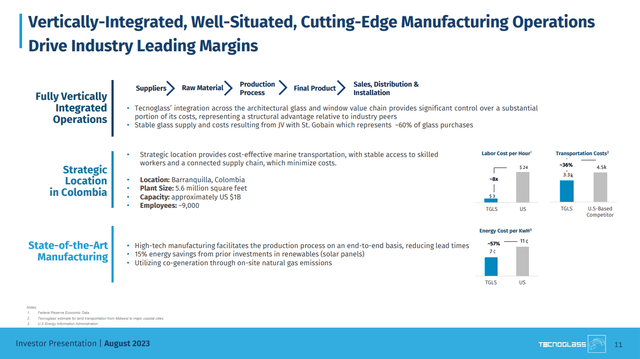

Lastly, the company is producing in its production facility in Colombia. This leads to a much cheaper labor cost of just $3 per hour, compared to $24 for a US-based manufacturer. A prior investment in renewables reduces energy costs and transportation costs are also estimated to be lower than a US operation. All of these factors have led to stellar margins.

Vertical integration (Tecnoglass Investor Presentation)

Capital Allocation

Tecnoglass defined five capital allocation priorities:

- Strategic growth capex is the highest priority. It invested $182 million over the last two and a half years to expand production capacity and automation. The company also showed superior Returns on Capital compared to its competitors of 15% versus 7% for the peer group.

- Dividends are the second-highest priority. At just a 7% EPS payout, the 1.1% yield has a lot of room for growth. One must remember that TGLS does not have a great dividend history. In 2020, the dividend was cut from $0.14 to $0.03 and was pretty stagnant before 2020.

- The board authorized buybacks up to $50 million.

- Debt repayment is a low priority, especially given the strong balance sheet with a net debt to EBITDA of just 0.3 and no significant maturities until 2026.

- Lastly, M&A is an option, but TGLS prefers to grow organically. However, management wants to be opportunistic in case a good deal presents itself.

Tecnoglass looks cheap

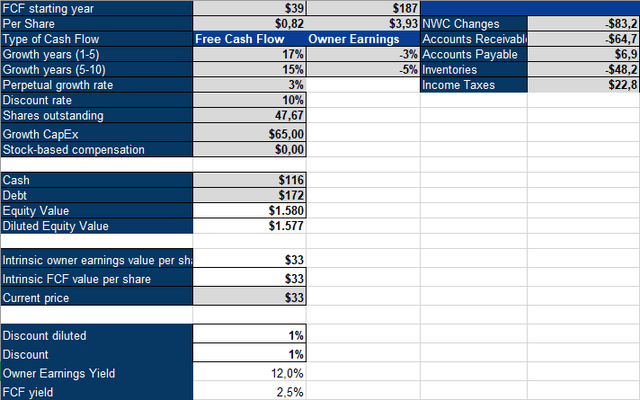

I believe that cash flows matter most and thus, I use an inverse DCF model to value Tecnoglass. The company is in a growth capex phase and has invested $182 million over the last two and a half years. Over the previous 12 months, capex was $82 million. Depreciation and amortization ($17 million) can be a good proxy for maintenance capex, so I used $65 million as growth capex in my model. We see a significant difference between Free Cash Flow and Owner Earnings (FCF + Growth CapEx – Stock based compensation +/- NWC changes). Once the growth capex cycle is over, Tecnoglass could return that capital to shareholders or moderate the spending.

Tecnoglass inverse DCF model (Authors Model)

We also get a large difference in required growth based on the large variance in these two cash flow numbers. While the company needs long growth in the high teens on an FCF basis, it could even contract in earnings on an owner-earnings basis. Given its large cash flows, I believe that Tecnoglass presents an excellent opportunity for investors if we consider capex and current NWC headwinds. The company has not yet penetrated many US states and has much potential for expansion. The architectural glass market is also expected to grow at a 5.6% CAGR through 2028, giving Tecnoglass a secular tailwind.

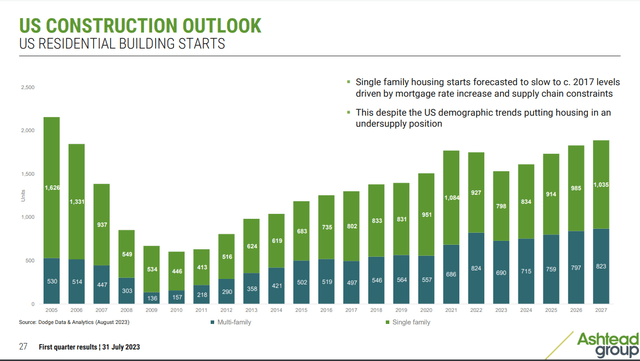

The stock has sunk 35% since its all-time high. The same picture can be seen with other industrials as well. The market is worried about increasing mortgage rates, now at rates not seen since 2000. The risk of a collapse in the US construction market does not look too likely if we look at the Dodge US Construction outlook. Tecnoglass of course is highly dependent on US construction, but even if the market were to turn, they could continue to grow by entering new markets. That being said, I trust in the forecasts of Dodge as a way to judge US construction. I assign a buy rating to Tecnoglass stock.

US Construction Outlook (Dodge Data & Analytics)

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here