Investment Rundown

Fluor’s (NYSE:FLR) share price has been on a roll since May this year. It has increased significantly in the last 12 months. This increase has happened for Fluor Corporation even as the bottom line has struggled as the company is aiming to diversify its business and move somewhat away from oil and gas. The market seems to be quite negative towards the company as the short interest is over 12% right now. Usually, this would indicate that there might be poor performance in the coming years.

Estimates seem to be quite varied for the coming years regarding EPS for FLR and I think this should come with a lower valuation than it has right now. The revenues are essentially tied to there being a need for energy services around the world and managing them to their fullest potential. The energy solutions segment has seen stronger momentum and this has helped offset some of the volatility and poor performance of the other segments. I am still not convinced that the company extrudes a substantial amount of value right now and will be sticking with a hold rating for FLR for the time being.

Company Segments

FLR headquartered just outside of Dallas, specializes in providing professional and technical solutions, including design and construction services for large-scale projects globally. Historically, its core focus has been on serving the oil & gas sectors and power generation industries. However, in the wake of the pandemic, which significantly affected the company’s business and profitability, FLR leadership has undertaken efforts to diversify its portfolio. This diversification includes expanding into areas such as energy transition, high-demand metals, infrastructure development, and undertaking substantial projects for various governments, both within the United States and abroad.

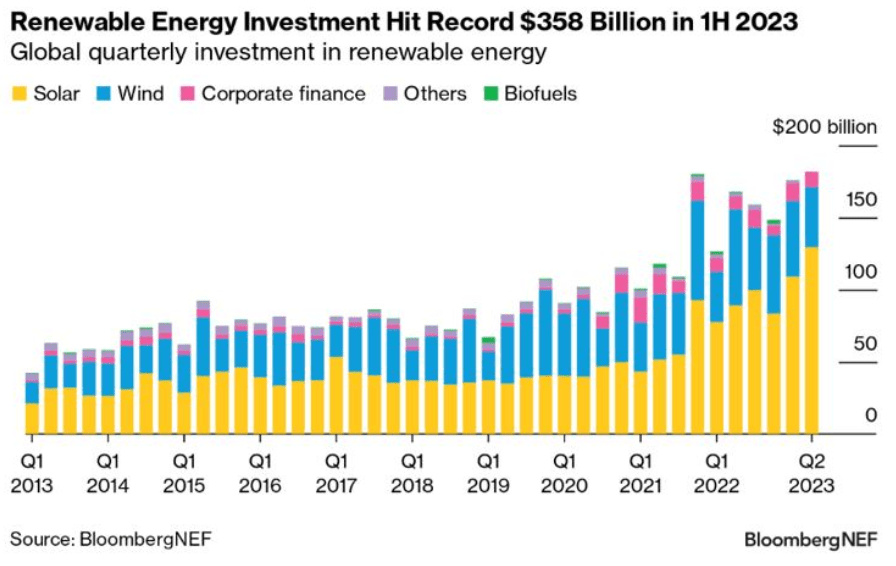

Renewable Investments (Bloomberg)

With more and more investments pouring into the renewables sector, I think that companies like FLR, which is getting in on the hype now, are going to perform very well over the long-term. One of the segments that grew very well in the last quarter was the mission solutions segment, almost 50% YoY. If this can continue, then FLR could showcase significant growth opportunities by engaging in emission and carbon projects. Investors seem to be somewhat undecided about the prospects of the company, as the share price has been quite volatile over the last few months.

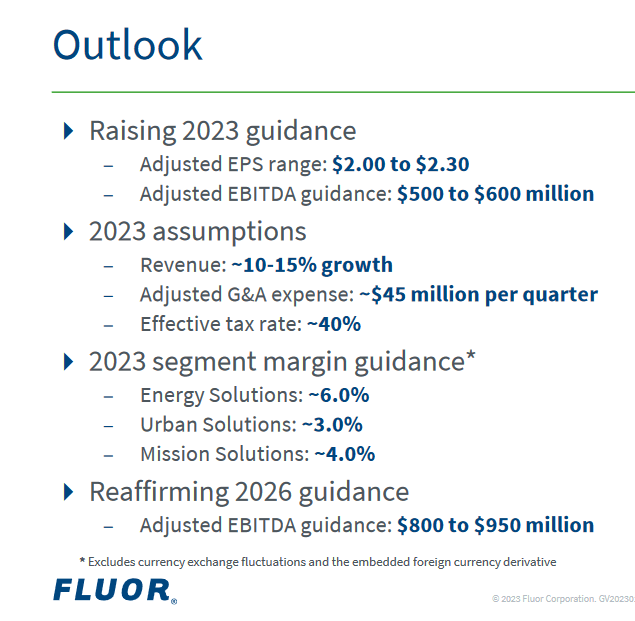

Outlook (Investor Presentation)

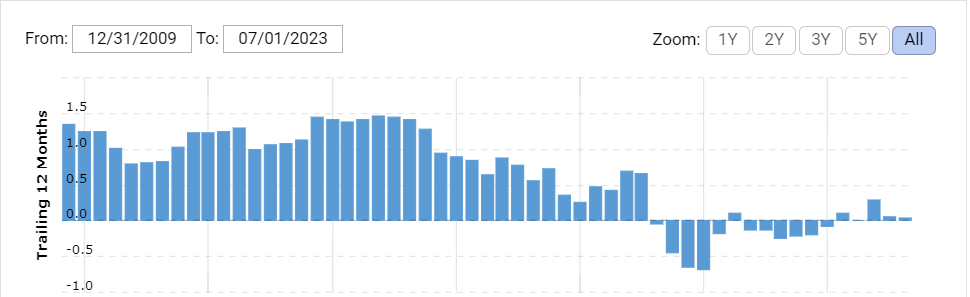

The EPS estimates suggest double-digit growth in the bottom line for the company in the near term. Nonetheless, the short interest is very high at over 12%. I think this revised optimism has come from the massive amount of backlog growth FLR has experienced. For the mission solutions segment alone, it’s nearing $5 billion right now.

Earnings Highlights

Income Statement (Earnings Report)

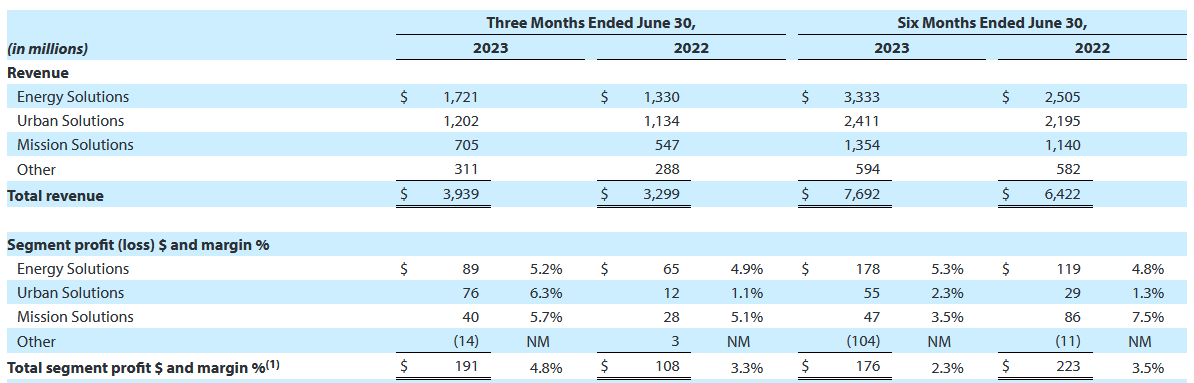

Looking at the results from the last quarter, the company had some difficulties in some parts of the business, more specifically the urban solutions which has fallen behind the other two in terms of growth. The lacking momentum here I think could halt the growth of the business.

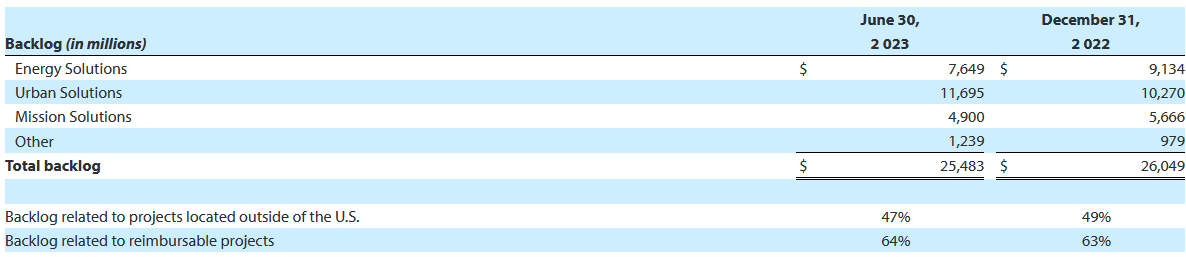

Backlogs (Earnings Report)

Seeing as FLR is quite dependent on there being a significant amount of backlogs built up to yield reliable and steady revenue growth and incentive to expansions, I think the last quarter was decent. The urban solutions sit at over $11 billion in backlogs right now, the highest level ever. If this can continue, then perhaps eventually it can be translated into more quickly growing revenues.

Company Grades (Seeking Alpha)

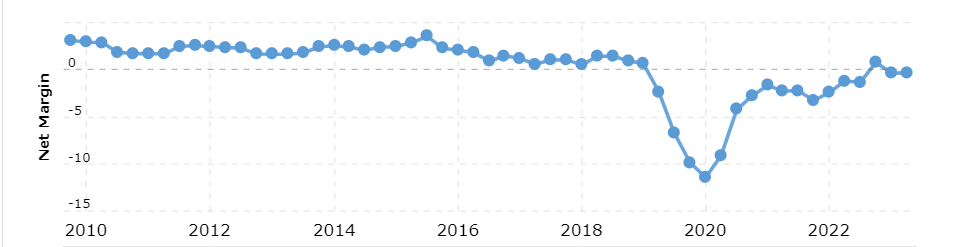

When we move our attention to the earnings multiple, I think we aren’t necessarily getting a very good deal. The p/e is at 17 right now and as you will see below in the article under the risk segment, the net margins have been steadily declining over the last several years. If this trend is continuing, I fear a significant correction may happen to the share price if FLR was to post a negative EPS for a quarter. This risk is also heavily weighing on the company right now and ultimately is a leading factor for a hold rather than a buy. On an FCF basis, FLR falters here too I think. The company has been unable to increase it significantly the last few years and as a result, trades at a FWD p/fcf of 45 which I just find too high to pay. It’s such a significant premium to the sector and leaves further downside risk to fall and correct instead.

When comparing FLR to a company like MDU Resources Group, Inc. (MDU) I think we get a more favorable case here instead. MDU trades at a p/e of 14.37, 15% below the same industrial sector that FLR operates in. Furthermore, MDU is right now also distributing a dividend of almost 3% and has been able to do so because of their solid margins; net margins have been consistently around the 5 – 6% range and I think it can continue that way as well going forward. This leaves more upside potential with MDU, given it both trades at an earnings discount and has a solid dividend yield too.

Risks

Investing in FLR does come with a certain level of risk, not necessarily in terms of the company’s survival, but due to the historical volatility associated with this business. Additionally, there’s a lack of clarity regarding the reinstatement of the company’s dividend, which, considering the current circumstances, seems like a prudent approach. The uncertainty surrounding the company’s results is notable, especially with one out of three segments currently not even achieving EBITDA profitability.

EBITDA (macrotrends)

The fact that the company is reporting negative EBITDA raises concerns about its ability to meet its debt obligations. With nearly $1 billion in debt on the books, if this trend continues, there’s an increased risk of resorting to share dilution as a means to address the debt situation.

Net Margins (macrotrends)

With the net margins trending downward for the company, I am becoming worried that the dilution I mentioned might be a reality. The saving grace could be the energy solutions segment of the business, which expanded revenues by nearly $400 million YoY last quarter. But this needs to be supported by strength across the other segments too. If that doesn’t happen then FLR will likely see its valuations cut and the high short interest could also increase further in my view.

Final Words

For investors that seek a broad company that has exposure to a variety of energy markets and industries, FLR seems like a decent opportunity if they can manage to turn the margins around. As we have seen, the bottom line has been steadily trending downwards and I fear there won’t be a quick reversal. The renewable energy projects the company is engaging in seem promising but it needs to translate to EPS growth. For the moment, the risk/reward is not very favorable in my opinion and leads to a hold rating for FLR.

Read the full article here