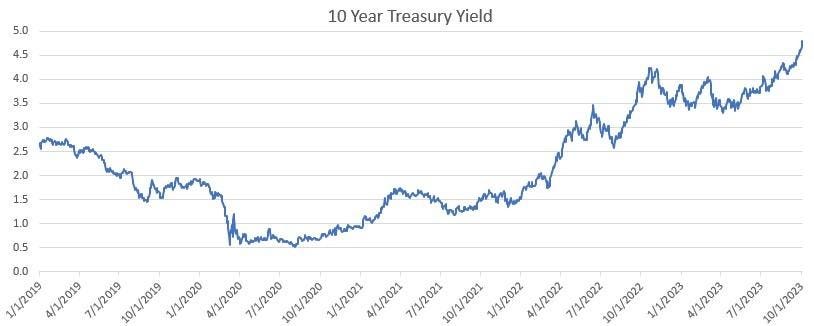

Just when investors were being lulled into complacency, the rug was pulled out from them as ten- year Treasury yields have surged by a full percentage point since mid-year to 4.8% this week, the highest level in 16 years. This move has been accompanied by a resurgent US dollar that is now at its high for this year and a pullback in the US stock market. Meanwhile, 30-year fixed mortgage rates are hovering around 7.5%, up from 6.9% three months ago.

What is perplexing for investors is that the factors causing the spike in yields are not obvious. Most of the run-up has occurred in the last two months when the Fed kept rates on hold, and investors believe it is near the end of the tightening cycle. Nor has there been a shift in perceptions that inflation is headed lower.

Consequently, investors are now asking several questions. First, what has caused the spike in yields? Second, how long will yields stay high? Third, will the associated tightening in financial conditions cause the US economy to weaken next year?

One explanation for the rise in yields is that investors are more confident about the resilience of the U.S. economy. They now accept that a “soft landing” is the most likely outcome, whereas they previously feared a recession. The economy is expanding close to its potential rate, which the Fed estimates to be 1.8% per annum. Estimates of real GDP growth for the third quarter are in the vicinity of 3%, although it could slow in the fourth quarter.

A second consideration is that investors appear more focused of late on the implications of prospective outsized budget deficits increasing the future supply of Treasuries. This will also take place as the Fed pursues quantitative tightening by shrinking its balance sheet.

A third factor relates to the term premium on bonds. It represents the additional yield on bonds that cannot be explained by expectations of future short-term rates. It captures all the uncertainties that investors accept in holding long-dated bonds including swings in inflation, economic growth and fiscal policy.

Since term premia are unobservable, they have to be extracted from the term structure of interest rates using mathematical techniques. Calculations by the New York Federal Reserve indicate that term premia have been negative for the past seven years but are now close to being positive as a result of the spike in yields. Previously, they added 25 basis points on average to longer-dated yields until the 2008 Financial Crisis, when investors flocked to safe assets such as treasuries.

Michael Howell of Cross Border Capital utilizes a different methodology, and he strips out the effects of bond volatility and inflation risk in the term premia to capture the effects of bond supply and demand.[1] His conclusion is that the rise in treasury yields since midyear mainly reflects two factors: (i) the revised perception of investors that interest rates will stay higher for longer, and (ii) the growing perception that the supply of treasuries will increase significantly in the future as a result of large federal budget deficits. In his view, investors should anticipate at least a 100-basis point gain in term premia based on future bond supply projections.

The bottom line is that different calculations of risk premia tell different stories about where bond yields may be headed. Those by the New York Fed suggest yields are not too far from their long-term trend, while the calculations by Michael Howell point to higher yields ahead. An analysis by Benson Durham of Piper Sandler concludes that options on 10-year Treasury futures imply that upside-downside risks to Treasury yields are evenly balanced.[2]

Which outcome materializes hinges on how the U.S. economy fares. The main consideration in this regard is that the surge in treasury bond yields, mortgage rates and the dollar, as well as the pullback in stocks, have tightened financial market conditions noticeably (see chart). Economists at Goldman Sachs, who are in the soft-landing camp, estimate that if this tightening is sustained, it could reduce US economic output by a full percentage point next year. If so, fears of recession would likely resurface.

The run-up in yields, moreover, is now impacting global bond markets according to the Financial Times. It is creating worries about potential capital losses for banks, insurers, pension funds and asset managers that own trillions of dollars of sovereign and corporate debt. While most U.S. banks will not have to realize losses if they hold bonds to maturity, fears about the ability of regional banks to manage interest rate risk could resurface.

Fed officials have not opined on what the changes in financial market conditions imply for the economy thus far. However, if the economy weakened it would likely spell the end of Fed tightening. Investors, in turn, would once again begin to anticipate an easing in monetary policy next year.

As regards fiscal policy, the spike in bond yields will add to interest expense on federal debt. In June, the CBO projected the annual interest cost would total $663 billion in fiscal 2023 and that it would double over the next ten years. In a recent speech, Treasury Secretary Yellen said that debt service costs are manageable for now – averaging about 2.9% in August — but she did not opine on whether yields would stay higher for longer.

So, what should investors do in these circumstances?

My take is that they should not over-react to the run-up in yields considering inflation is on a declining trend and the economy could soften next year as a result of the tightening in financial conditions. As the Fed ends a prolonged period of unorthodox monetary policies since 2008, treasury yields are now returning to more normal conditions and are more fairly priced than before. In this context increased bond volatility can be viewed as part of the normalization process.

[1] CrossBorderCapital Global View, October 2023.

[2] Piper Sandler commentary, “Yield Risks: Up or Down?” October 5, 2023.

Read the full article here