By Peter Vanden Houte, Chief Economist, Belgium, Luxembourg, Eurozone

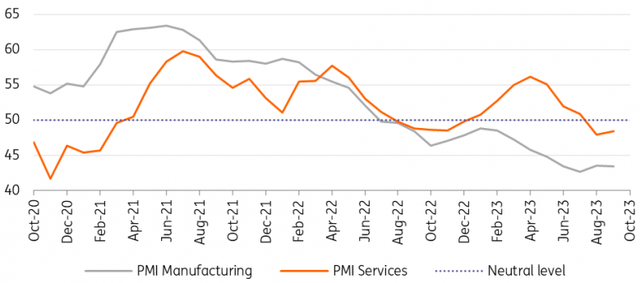

Softening orders

The latest economic data continues to confirm our scenario of a weakening growth environment in the eurozone, though the slowdown is no longer intensifying, as most indicators have stabilised around subdued levels. The PMI composite indicator is in contraction territory and the €-coin indicator, a proxy for the underlying growth pace, stood at -0.18% in September. However, we doubt that third-quarter growth was negative. Europe saw a very strong tourism season and not all services indicators are at recessionary levels (yet).

That said, there doesn’t seem to be an upturn in the offing. Inventory levels remain quite high and according to the PMI survey, orders in both manufacturing and services have softened further to levels not seen since the pandemic. This doesn’t bode well for the fourth quarter and that’s the reason why we now pencil in a very small negative figure for fourth-quarter GDP growth.

Sentiment indicators continue to be weak

LSEG Datastream

The labour market conundrum

The question is what happens afterwards. Most international institutions see a stronger growth rate in 2024 than in 2023. The current cycle has indeed some special features, one of them being the demographically induced labour scarcity. Because of that we are now experiencing the rare combination of weak business sentiment and declining unemployment (the eurozone unemployment rate was at a record low in August). The fact that the labour market is holding up well and that real wages are now rising is certainly a factor that supports consumption and for the time being prevents the current downturn from morphing into a full-blown recession.

Slower growth in 2024

However, concluding from this that growth can only accelerate is perhaps a bit premature. Let’s not forget that monetary policy works with a lag. And we have reasons to believe that the lag might be a bit longer than in the past, as the long period of low and even negative interest rates has probably allowed companies and governments to lengthen the duration of their debt. That said, credit growth was close to a standstill on a year-on-year basis in August and this trend is unlikely to reverse anytime soon. On top of that, there is still no agreement on a revamped Stability and Growth Pact, meaning that member states must abide by the old rules and present significantly more restrictive budgets this month. Several member states are at risk of the excessive deficit budget procedure, probably leading to some spread widening. Putting it all together, we only see some genuine improvement in the growth outlook from the second half of 2024 onwards. But we forecast this will result in a mere 0.4% GDP growth for the whole of 2024 after 0.5% this year.

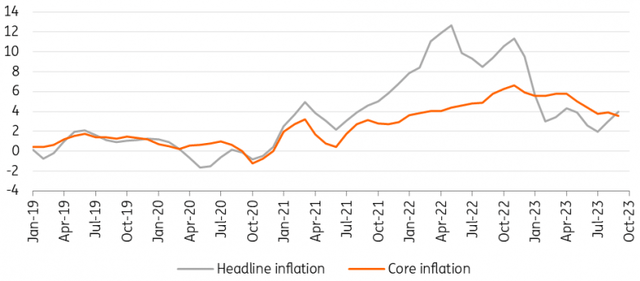

Inflation trend

3m-on-3m annualised consumer price change

LSEG Datastream

Inflation only slowly declining

Both headline and core inflation fell in September to 4.3% and 4.5%, respectively, and that was better than expected. However, one must bear in mind that base effects play a very important role in the recent decline. That’s why we like to look at the 3-month on 3-month annualised rate of inflation, showing the headline rate at 4.0% and core at 3.6%. Although softening, the trend is thus still clearly above 2%. On top of that, the recent oil price increase is likely to keep headline inflation higher in the first half of 2024. We are now anticipating 5.9% headline inflation for this year and 3.0% for 2024.

The ECB increased its main interest rates again in September, bringing the interest rate on the deposit facility to 4%, a 450 basis point increase in just 14 months. The monetary policy statement suggested that the top might have been reached, though rates will have to be kept high for a sufficiently long duration to bring inflation back to target. That is the reason why we shifted our expectation for a first rate cut to the third quarter of 2024. The ECB is also considering ending the reinvestment of the Pandemic Emergency Purchase Programme holdings early to diminish the amount of excess liquidity. An announcement to do so could fall in the first quarter of next year. All of this limits the potential for a substantial bond rally.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user’s means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more.

Original Post

Read the full article here