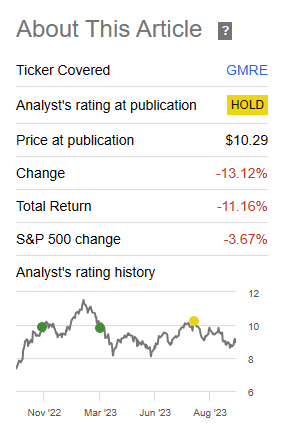

Global Medical REIT Inc. (NYSE:GMRE) is a medical office building play that we have covered before. After two buy ratings, we moved to the sidelines in our last piece.

Seeking Alpha

There was really nothing strongly negative about the company. In fact, we appreciated how management had managed to focus on real investor wellbeing rather than the empire building we have seen from some players. We concluded with,

The last time around we had lowered the fair value to $11.50 and we are moving even lower today to $11.00. This is about in line with some of the lower NAV estimates. The properties are well buffered against economic stress, but there is a huge glut of regular office space in secondary markets. The difference between medical office and regular office space is not so large that it cannot be bridged with the right capex. Coupled with the lack of growth and the short debt maturity, we have enough to want to hit the exits. We sold the $10.00 calls recently and along with the current dividend, this provides enough of a buffer.

Source: Higher For Longer Scenarios Will Stress The REIT

Update On the Common Shares

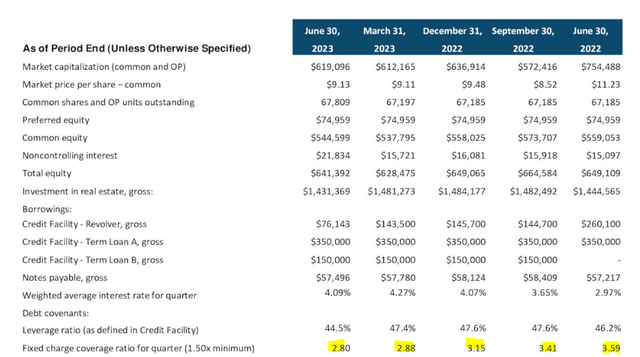

GMRE’s Q2-2023 was about in line but we saw the slow and steady impact from the interest rate hikes. Fixed charge coverage was steadily moving lower and we are likely to see the same trend in Q3-2023.

GMRE Q2-2023 Presentation

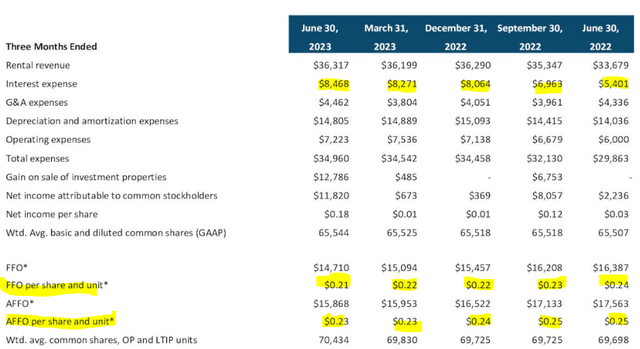

Interest expenses are up substantially from Q2-2022 and funds from operations (FFO) and adjusted FFO are both falling under the pressure.

GMRE Q2-2023 Presentation

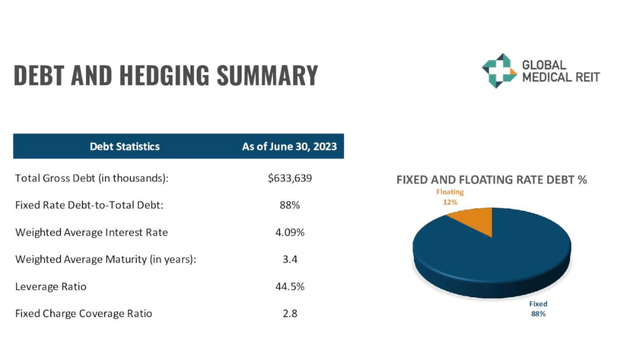

It is fascinating that we are here despite a primarily fixed-rate regime for the REIT.

GMRE Q2-2023 Presentation

The weighted maturity does still look small and that represents the biggest risk to the long term health of the company. The company is aware of this and is actively managing things before there are problems.

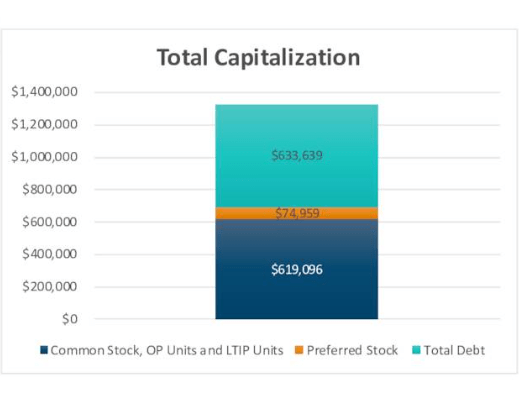

Jeffrey M. Busch, Chairman, Chief Executive Officer and President stated, “During the second quarter, we took a significant step forward in reducing our variable rate debt and leverage by selling a medical office building portfolio in Oklahoma City, Oklahoma for gross proceeds of $66 million. We used the net proceeds from this disposition to pay down the balance of our variable rate debt, resulting in a leverage ratio as of June 30, 2023 of 44.5%.

Source: GMRE Q2-2023 Press Release

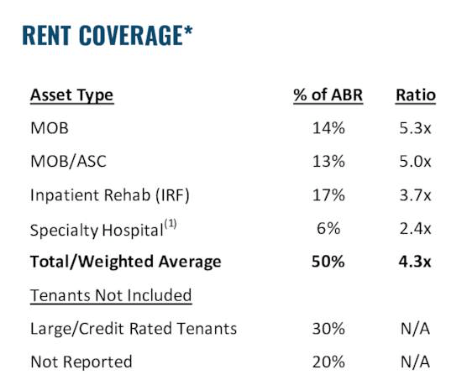

Portfolio level metrics look great, as they always have. We would not expect any deterioration here, outside of a very severe recession.

GMRE Q2-2023 Presentation

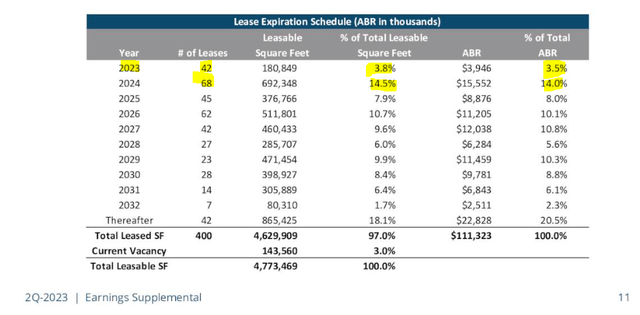

GMRE has a soft lease maturity schedule for the remainder of 2023 and then we have over 14% coming up for renewal in 2024.

GMRE Q2-2023 Presentation

Occupancy levels remain near 97% and this is the other area to monitor. While the two (office buildings and medical office buildings) are not identical, there are overlaps. It is not too uncommon to find doctors having clinics in general office space and also seeing general office space “upgraded” to accommodate doctors. With the plethora of office space that is begging for attention, this is a risk that investors should look out for. Keep in mind that doctors are not the class of tenants that will move to save a few dollars. Practice location and convenience are key. Most also have staffing shortages and moving to a new location might make that worse. But it is a longer term risk factor for this area. Even in the more complex area of laboratory spaces, which Alexandria Real Estate Equities, Inc. (ARE) specializes in, we have seen conversions start to create additional supply. So while the asset class may be recession resistant, it is not going to defy the laws of supply and demand.

Global Medical REIT Inc. 7.50% CUM PFD A (NYSE:GMRE.PR.A)

Whichever way you look at it, GMRE.PR.A is of course safer than the common shares. After all, you have the large common equity buffer in front.

GMRE Q2-2023 Presentation

But is this the best bang for your buck? Probably not. One issue we have with GMRE.PR.A is just how lopsided the setup is on this, thanks to the very high coupon of 7.5%. GMRE.PR.A trades right near par with a 7.7%. Now, that does not sound like a problem by itself, but you have the risk of a call, immediately in the next rate cut cycle. So you have minimal upside and yes, all the downside if interest rates go higher or if the gradual destruction of value in the company. We will illustrate our point further with two examples.

Spirit Realty Capital, Inc. 6% PFD SER A (SRC.PR.A)

In the realm of REITs, triple nets tend to be the safest. The parent company here Spirit Realty Capital (SRC) sports a BBB rating (GMRE does not have a credit rating). SRC has a fantastic balance sheet. The weighted average lease maturity is over 10 years. On a credit quality SRC is definitely going to be miles and miles ahead of GMRE. But you get about the same yield from both preferred shares with SRC.PR.A giving you 7.48%. The big difference here is that SRC.PR.A trades at $20.06 offering you substantial upside to par in case of interest rate cuts.

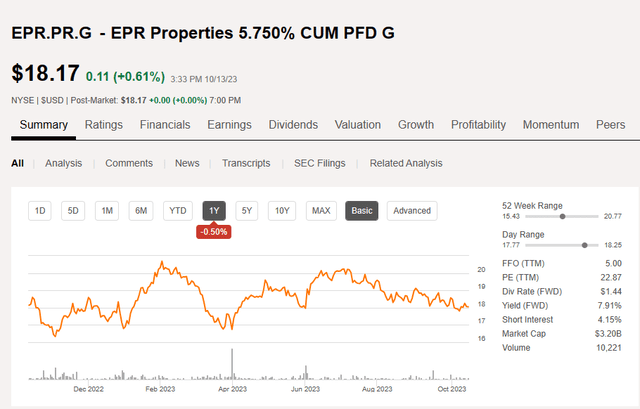

EPR 5.75% Series G Cumulative Redeemable Preferred Shares (NYSE:EPR.PR.G)

This is from EPR Properties (EPR) which we recently wrote about. We will focus on this one, even though EPR has two other preferred share series. This one is a straight preferred (no convertible calculations) and offers a 7.91% yield currently. It too trades at a big discount to par and offers substantial upside in case of a rate cutting cycle.

Seeking Alpha

On a credit quality basis as well, we see EPR preferreds as somewhere between GMRE.PR.A and SRC.PR.A. So relative to GMRE.PR.A, you are getting higher credit quality and more upside if interest rates are cut.

Verdict

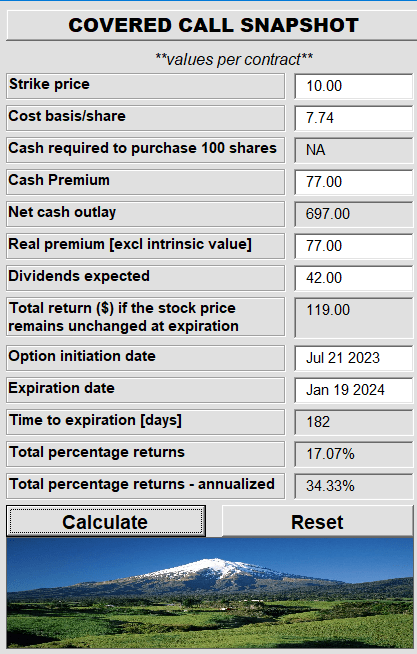

Common shares now offer a 9.4% yield and we think that will be maintained for the foreseeable future. Of course growth is going to be next to impossible as the AFFO payout ratio approaches 100% and the company can only issue equity below NAV. But the stock still has value and we think we can eek out 10-12% returns from here by opportunistically using covered calls. Our last executed covered calls are shown below and they reduced the volatility of our position substantially.

Author’s App-Trade Alert 368

The preferred shares seem remarkably expensive relative to what is available today. We would only be interested in GMRE.PR.A shares if they offer a 8.2% plus yield.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Read the full article here