The stock market, as measured by the S&P 500 Index

SPX,

has repeatedly seen rallies thwarted at the 4800 level this year. That is near the all-time high of SPX (the NASDAQ 100

NDX,

and the Dow Jones Industrial Average

DJIA

have both already made new all-time highs, but they too are facing resistance at current levels).

As this resistance has emerged, market internals have begun to worsen. However, the price pullback in SPX has been quite small so far, and if this is all the downside the bears can muster, then the bull market may still be intact.

There is support just below 4700 (the recent lows), with stronger support at 4600. The major support (4600) and resistance (4800) are marked on the accompanying SPX chart. If SPX should fall below 4550 (the December lows), that would be a very negative development and could indicate the start of a new bear market.

The recent McMillan Volatility Band (MVB) sell sign remains in place (marked with a green “S” on the SPX chart). Its target is the -4σ Band, which is now above 4600, so that might indicate even stronger support at that level. The MVB sell signal would be stopped out if SPX were to close above the +4σ Band, which is now at roughly 4880 and still rising.

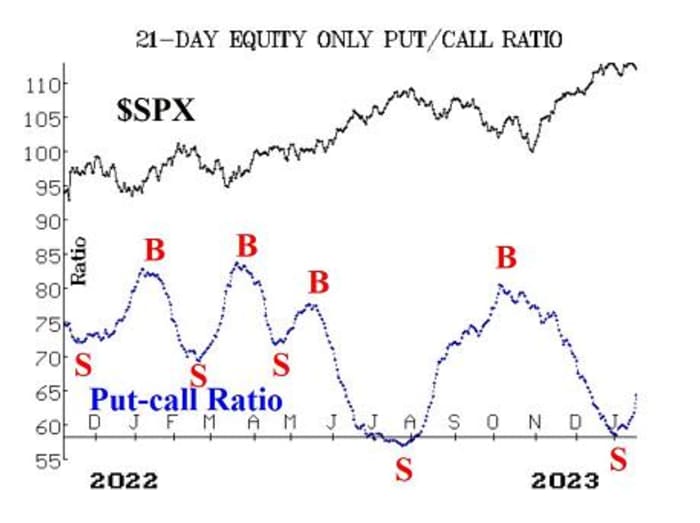

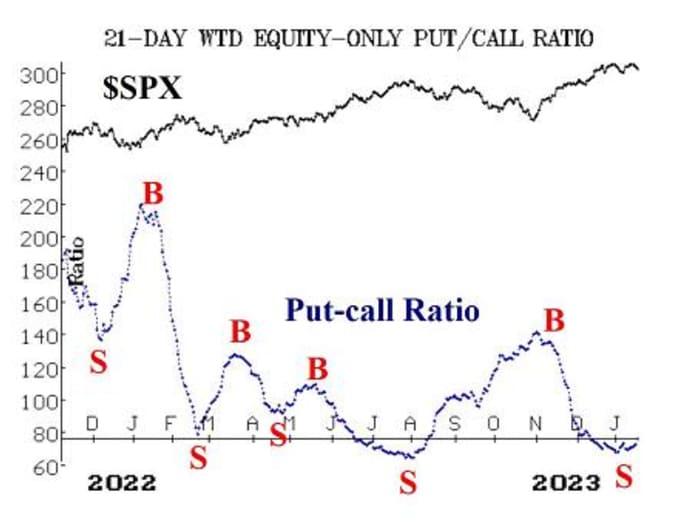

Equity-only put-call ratios have been on sell signals, and those signals are strengthening this week, as put buying is increasing. Both ratios are rising now, and as long as that is the case, it is a negative sign for the stock market.

Meanwhile, breadth has been terrible, and both breadth oscillators remain on sell signals. The “stocks only” oscillator is now in deeply oversold territory, and the NYSE oscillator is not far behind. In other words, despite the fact that SPX is only off slightly from its highs, breadth has gone from deeply overbought in late December to deeply oversold now. That means that this market internal has already “corrected,” even though SPX has not fallen much.

New Lows on the NYSE have finally overtaken New Highs. For the last two days New Lows have had the upper hand, and so this buy signal — which was confirmed last November — has been stopped out. This is not a sell signal, however. The indicator is in “neutral” status at the current time. Its next signal will come when New Lows or New Highs on the NYSE number more than 100 for two days in a row.

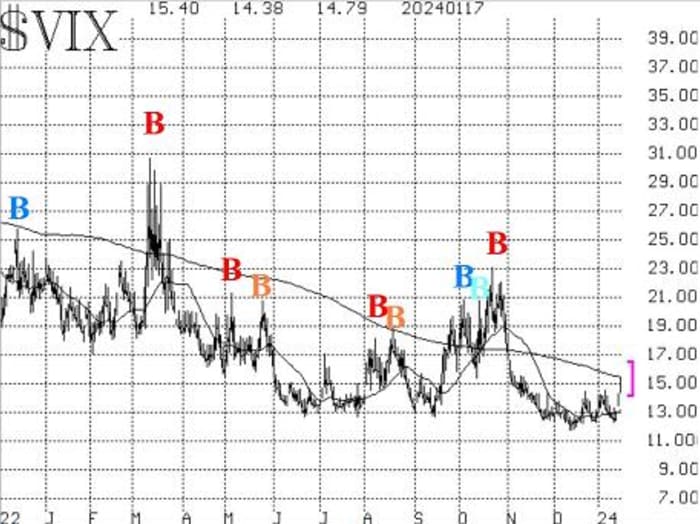

The market internals discussed above have been, or are, fairly negative. That is not the case with the implied volatility indicators — VIX and its derivatives. They have remained quite bullish throughout the last few weeks, although things might be about to change.

VIX

VIX

VX00,

remains at a low level, and a low VIX is not a problem for stocks. It’s when VIX begins to rise that stock traders should get worried. Specifically, we are looking at VIX compared with its declining 200-day Moving Average (currently at 15.40 and declining). If VIX were to close above that 200-day MA, that would stop out the trend of VIX buy signal that has been in place since November. Even then, that would not be a sell signal -– just a move to a neutral status.

Perhaps more worrisome, though, would be if VIX were to return to “spiking” mode — a close of at least 3.0 points higher over any three-day or shorter time period. That nearly happened this past week. Today, VIX would enter “spiking” mode if it were to close above 15.70. When VIX is in “spiking” mode, the stock market can fall sharply, but eventually it leads to a “spike peak” buy signal.

The construct of volatility derivatives remains bullish in its outlook for stocks. That is, the term structures of the VIX futures and of the CBOE Volatility Indices continue to slope upwards, and the futures are trading at a premium to VIX. The front month is now the February VIX futures (January expired this past Wednesday), so the relationship that we are watching is February versus March. If the price of February should rise significantly above the price of March, that would be very negative for stocks. This has not remotely been the case so far, though, as March continues to trade about one point above February.

The realized volatility sell signal that occurred a couple of weeks ago is still in place, since the 20-day historical volatility of SPX (HV20) has remained above 9%.

Seasonality is still potentially playing an important role currently. We are in a seasonally negative period in mid-January, which is often best reflected in a decline in the NDX index. But a strong positive seasonality begins at the end of this month.

Overall, we are still maintaining a “core” bullish position as long as the price of SPX is above 4600. We are, however, trading other confirmed signals around that “core” position. The market “feels” bearish, but the indicators are mixed.

Market insight: The ‘January defect’ (part 2)

As noted in last week’s report, this particular system is centered around the fact that there is usually a market correction in the middle of January (after the initial new deposits have been invested by institutions), and it is most evident in tech stocks. Hence, the trading system is to short the NASDAQ 100 Index at the close of the 8th trading day of January and to cover the short at the close of the 18th trading day of January.

In theory, the system enters its position by buying QQQ

QQQ

puts at the close of the 8th trading day of January, which was Jan. 11th. In reality, the best entry point has varied over the years, so we are going to enter in stages. Overall, the best performance results, percentage-wise, have come from entering on the 12th trading day. The median gain (for the short sale) from entering on the 12th trading day has been 0.8%. So, we are going to add to our position at today’s close, which is the 12th trading day of January.

At the close of trading on Jan. 18th, (the 12th trading day of January), Buy 1 QQQ Feb (2nd) at-the-money put.

Your total position will thus be two long QQQ puts, which might each have a different striking price. With regard to taking partial profits, sell the first put that becomes 20 points in-the-money, and roll the other down when and if it becomes 20 points in-the-money. Sell all the remaining puts at the close of trading on the 18th trading day of January — Friday, Jan. 26.

Note that, at the close of the 18th day, the other January Seasonal trade will begin.

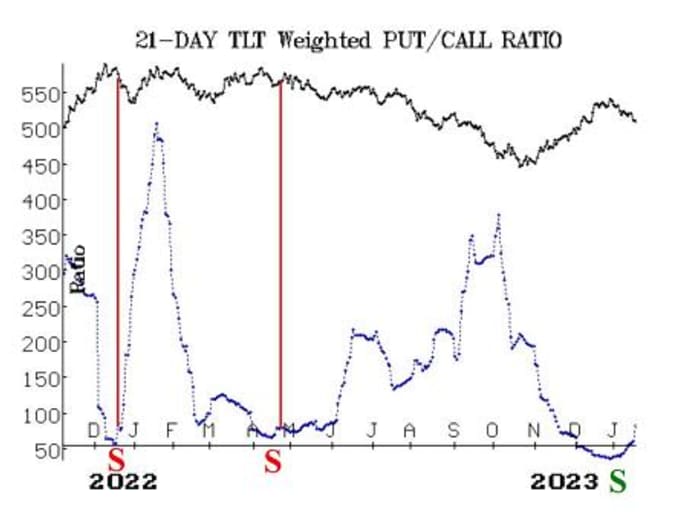

New recommendation: U.S. Treasury bonds (TLT)

TLT

TLT

is the ETF that tracks the price of 20+ year Treasury bonds. There have been new put-call ratio sell signals in both the futures options in Treasurys and in the ETF options of TLT. These have a decent track record, so we are going to act.

Buy 3 TLT May (19th) 95 puts in line with the market.

TLT: 94.34 May (19th) 95 put: 3.30 bid, offered at 3.40

If bought, we will hold as long as the put-call ratio sell signal is in place for Treasurys.

Follow-up action:

All stops are mental closing stops unless otherwise noted.

We are using a “standard” rolling procedure for our SPY spreads: in any vertical bull or bear spread, if the underlying hits the short strike, then roll the entire spread. That would be roll up in the case of a call bull spread or roll down in the case of a bear put spread. Stay in the same expiration and keep the distance between the strikes the same unless otherwise instructed.

Long 4 expiring XLP

XLP

Jan (19th) 72 calls: Roll to the Feb (16th) 72 calls. The stop remains at 71.20.

Long 1 expiring SPY

SPY

Jan (19th) 477 call: This position was initially a long straddle. It was rolled up, and the puts were sold. The calls were rolled up twice more. This is, in essence, our “core” bullish position. Roll to the Feb (16th) 477 call. Roll the calls up every time they become at least eight points in-the-money.

Long 2 expiring TECH

TECH,

Jan (19th) 70 calls: Sell these calls to close the position.

Long 1 SPY Feb (16th) 477 call and short 1 SPY Feb (16th) 497 call: This spread is based on the “New Highs vs. New Lows” buy signal. New Lows on the NYSE have exceeded New Highs for two consecutive trading days, so close this spread now.

Long 4 UNM Mar (15th) 45 calls: We will hold this position as long as the weighted put-call ratio of UNM

UNM,

remains on a buy signal.

Long 1 SPY Feb (16th) 480 call: This call was bought in line with the Cumulative Volume Breadth (CVB) buy signal. The entire premium is at risk here, since there really isn’t a stop-out for this trade. Sell these calls if SPY trades at 482 at any time.

Long 10 ESPR

ESPR,

Feb (16th) 3 calls: The closing stop remains at 2.25.

Long 2 DIS June (21st) 90 puts: We will hold these puts as long as the weighted put-call ratio of DIS

DIS,

is on a sell signal.

Long 1 SPY Feb (16th) 469 put and Short 1 SPY Feb 16th) 449 put: Was bought in line with the McMillan Volatility Band sell signal. It will reach its target if SPX trades at the -4σ Band, and it will be stopped out of SPX closes above the +4σ Band.

Long 1 SPY Feb (16th) 469 put and Short 1 SPY Feb 16th) 449 put: Was bought in line with the HV20 sell signal. It will be stopped out if the 20-day historical volatility of SPX (HV20) falls below 9%.

Long 1 SPY Feb (16th) 469 put and Short 1 SPY Feb 16th) 449 put: Was bought because the Santa Claus Rally failed this year. We are going to modify the stop slightly: stop out SPX closes above 4800 for two consecutive days.

Long 1 QQQ Feb (2nd) 409 put: This is the first of two QQQ puts which will be bought in line with the January Defect seasonally bearish time period. The second put will be bought at the close of trading on Thursday, January 18th. Your total position will thus be two long QQQ puts, which might each have a different striking price. With regard to taking partial profits, sell the first put that becomes 20 points in-the-money, and roll the other down when and if it becomes 20 points in-the-money. Sell all the remaining puts at the close of trading on the 18th trading day of January — Friday, Jan 26.

Long 1 SPY Feb (16th) 476 straddle: We are going to use a “money” stop here. If the straddle’s offer is less than 7.0 at any day’s close, stop yourself out. Meanwhile, roll either option if it becomes eight points in-the-money.

All stops are mental closing stops unless otherwise noted.

Send questions to: [email protected].

Lawrence G. McMillan is president of McMillan Analysis, a registered investment and commodity trading advisor. McMillan may hold positions in securities recommended in this report, both personally and in client accounts. He is an experienced trader and money manager and is the author of the best-selling book, Options as a Strategic Investment. www.optionstrategist.com

©McMillan Analysis Corporation is registered with the SEC as an investment advisor and with the CFTC as a commodity trading advisor. The information in this newsletter has been carefully compiled from sources believed to be reliable, but accuracy and completeness are not guaranteed. The officers or directors of McMillan Analysis Corporation, or accounts managed by such persons may have positions in the securities recommended in the advisory.

Read the full article here