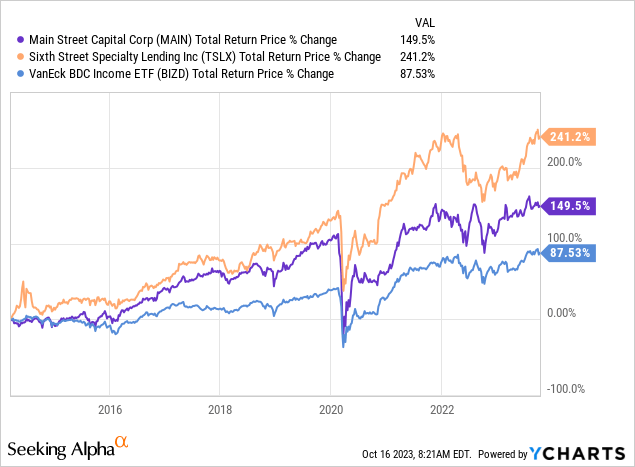

Two of the very best-of-breed business development companies, or BDCs (BIZD), in the market today are Main Street Capital (NYSE:MAIN) and Sixth Street Specialty Lending, Inc. (NYSE:TSLX). They both have significantly outperformed the broader BDC space over time:

In this article, we will compare them side-by-side and offer our take on which is a better buy right now:

MAIN Stock Vs. TSLX Stock: Investment Portfolio Analysis

Sixth Street Specialty Lending primarily invests in middle-market loans targeting U.S.-based companies. These companies typically have an EBITDA ranging from $10 million to $250 million, with the portfolio’s average EBITDA at $67 million. Their portfolio is heavily weighted towards senior secured debt investments, with 91.9% of TSLX’s investments being senior secured and 90.6% being first-lien debt investments. This makes them one of the most defensively positioned BDCs and – with 99.2% of the portfolio consisting of floating rate debt investments – they are well-positioned to benefit from a rising interest rate environment. Moreover, they have excellent underwriting performance with non-accruals making up only 0.6% of the portfolio at fair value, indicating that the vast majority of their investments are performing as expected.

Main Street Capital’s unique investment strategy, meanwhile, focuses on equity investments in the lower middle market portfolio, which they believe provides them with unique opportunities for net asset value growth alongside the generation of recurring dividend income. This strategy has paid off significantly, as since 2007, MAIN has witnessed a NAV growth of $14.84 per share (a 115% increase).

Moreover, MAIN’s internally managed operating structure offers significant operating leverage and a very low expense ratio relative to many of its peers, thereby increasing net profit margins for shareholders.

MAIN’s portfolio also benefits from strong underwriting performance. While 83.5% of the portfolio is invested in debt, 69.3% in senior secured debt, and 58.2% in variable rate debt as of the end of its latest quarter, only 0.3% of the total investment portfolio at fair value was on non-accrual status.

MAIN Stock Vs. TSLX Stock: Balance Sheet Analysis

Sixth Street Specialty Lending enjoys a solid balance sheet with a leverage ratio of 1.16x, fitting within TSLX’s target range of 0.90x – 1.25x. On the liquidity front, TSLX has an undrawn capacity of $659 million on its revolving credit facility against $190 million of unfunded portfolio commitments, determined by the stipulations of their loan agreements. The debt maturity profile is also well-structured as the average life of investments funded by debt is about 2.5 years, while the liabilities have a weighted average maturity of around 4.1 years. This staggered maturity calendar reduces potential refinancing risks. Last, but not least, TSLX’s investment grade credit ratings from multiple agencies such as Fitch, S&P, Moody’s, and KBRA further underscore its financial strength.

Main Street Capital also boasts investment grade ratings from both S&P and Fitch, allowing MAIN to access debt at fairly attractive rates. With a very low leverage ratio of 0.87, a non-SBIC leverage ratio of 0.75, and an interest coverage ratio of 4.35, MAIN’s balance sheet appears to be in very strong shape. Moreover, it has roughly three-quarters of a billion dollars in total liquidity and a very well-laddered debt maturity profile:

- Corporate Facility: $980.0 million, SOFR+1.875% floating (7.1%), Maturity in August 2027 with $410.0 million drawn.

- SPV Facility: $255.0 million, SOFR+2.50% floating (7.8%), Maturity in November 2027 with $170.0 million drawn.

- Notes Payable: $500.0 million, 3.00% fixed, Redeemable at MAIN’s option, Maturity on July 14, 2026.

- Notes Payable: $450.0 million, 5.20% fixed, Redeemable at MAIN’s option, Maturity on May 1, 2024.

- Notes Payable: $150.0 million, 7.74% fixed (weighted average), Redeemable at MAIN’s option, Maturity on December 23, 2025.

- SBIC Debentures: $350.0 million, 3.00% fixed (weighted average), Various dates between 2024 – 2033 (weighted average duration = 5.1 years).

MAIN Stock Vs. TSLX Stock: Dividend Outlook Analysis

TSLX’s net investment income for Q2 2023 was $0.58 per share, while the distributions per share were $0.50, giving TSLX ample coverage of its dividend. As management pointed out on the latest earnings call:

This quarter’s net investment income continues to reflect the strength in the core earnings power of our portfolio as we over earned our quarterly base dividend by 28%…Based on the current shape of the forward curve, we expect that the interest rate environment will continue to support core earnings in excess of our base dividend through 2024 without any activity-related income.

In addition to the positive outlook from the forward curve and its current robust dividend coverage ratio, TSLX’s dividend outlook is also bolstered by the fact that the company’s spillover income per share estimate is currently at $0.90.

MAIN’s dividend is paid out monthly, distinguishing it from many BDCs, including TSXL (which pays out quarterly dividends). Perhaps most impressively – especially given that MAIN has been in operation since before the Great Financial Crisis – the company has never cut its regular monthly dividend payout. Moreover, from Q4 2007 to Q4 2023, there has been a 114% increase in monthly dividends, while supplemental dividends amounted to $0.775 per share during the last twelve months. As a result, MAIN has a tremendous track record as a monthly dividend growth stock.

Moreover, MAIN’s dividend appears to be in very strong shape for the foreseeable future, with management pointing out on their latest earnings call:

Our DNII in the second quarter exceeded the monthly dividends paid to our shareholders by 66% and the total dividends paid to our shareholders by 24%…our Board declared a supplemental dividend of $0.275 per share, payable in September, representing our largest and eight consecutive quarterly supplemental dividend. Our Board also declared an increase in our regular monthly dividends for the fourth quarter of 2023, to $0.235 per share, payable in each of October, November, December, representing a 6.8% increase from the fourth quarter of 2022.

MAIN Stock Vs. TSLX Stock: Valuation Analysis

In terms of valuation, MAIN is more expensive than TSLX, as it is currently trading at a 43.34% premium to its NAV whereas TSLX is currently trading at a 19.35% premium to NAV.

MAIN also has a lower dividend yield than TSLX does, offering investors a 7.11% yield compared to TSLX’s 9.21% yield.

Investor Takeaway

Both MAIN and TSLX are clearly high quality BDCs with impressive track records, well-built and high-performing investment portfolios, relatively strong and conservatively positioned balance sheets, and well-covered dividends. That said, given how much more expensive Main Street Capital is than Sixth Street Specialty Lending, Inc., if we had to pick one of these stocks today, we would purchase TSLX. However, neither is cheap enough for us to buy in an environment where we expect economic conditions to decline and interest rates to be at or near peak levels, both of which should pose as headwinds to these BDCs. As a result, we are neutral on both of them right now.

Read the full article here