Summary

One area where the financial and tech world come together is the world of cybersecurity, so today I am rating Akamai Technologies (NASDAQ:AKAM), a well-established provider of managed cybersecurity solutions, among a basket of other products.

My analysis gives this stock a Hold rating for the following reasons:

I think the cybersecurity segment will continue to be their growth engine despite being in a crowded market. However, I would not rate it currently a Buy as this stock does not currently pay any dividends, its most recent earnings report for Q1 was lackluster, and with a balance sheet needing some improvement.

In addition, its current price chart shows potential to hold on to it some more, if you currently hold their shares, but if I were a new investor I would not buy it at this time.

Risks to my neutral outlook on this stock would be that the company decides to start offering a dividend this year and it attracts a wave of dividend investors to this company, as well as the next few quarterly earnings reports extremely outperforming, combined with investors being bullish on tech stocks in general again later in the year and causing a tailwind for the sector. If these materialize, it could end up making my current rating a bit too cautious.

Growth in the Cybersecurity Segment should be Promising for this Firm

This company, founded in 1998 and based in Cambridge, Massachusetts, has by now established itself as a serious tech brand, in my opinion.

From info on its company website, it is “trusted by 45 of the top 50 brokerages, 16 of the top 20 banks, and 14 of 15 US federal civilian cabinet agencies.”

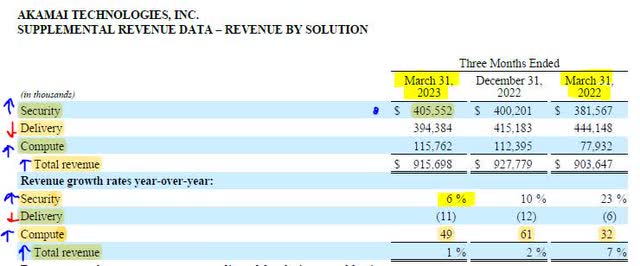

Further, based on its Q1 2023 earnings results, I can see that their cybersecurity segment is growing:

……………………………………………………………………………………………..

Q1 2023 Earnings – Revenue by Segment (Akamai Technologies)

……………………………………………………………………………………………..

From the screenshot above, you can see that its security segment’s revenue increased from the same quarter in the prior year, as did their compute segment, while their delivery segment lost revenue.

In their Q1 2023 release, the firm commented that “security and compute revenue represented 57% of total revenue in the first quarter and grew 13% year over year.”

In fact, in their earnings release, their CEO Tom Leighton reiterated the growth in security.

“For the first time in Akamai’s 25 year history, security became our largest revenue stream,” he remarked.

As someone who has worked in IT and currently writes about both financial and tech stocks, rather than discuss every single security solution this company offers I will say that managed cybersecurity solutions overall are vital to our critical infrastructure which is continually subject to threats… so hence we need multiple vendors who can provide risk reduction to these infrastructure threats.

In IT departments I have been in, usually multiple vendors are used for multiple solutions, since security is not about a single magic wand but a multi-layered approach to risk management and control.

Although the market is crowded with multiple vendors, this firm has proven in its results that it can grow revenue in this specific segment year over year, and that it has recognized the ongoing need in the marketplace to protect the infrastructure, but also that clients have put trust in this firm.

One look at its client list on the company website and you can see that they do business with the likes of Liberty Mutual, Lufthansa Airlines, Airbnb (ABNB), and Adobe (ADBE), to name a few.

My sentiment was echoed by a March 2023 article by the International Monetary Fund:

Tight financial and technological interconnections within the financial sector can facilitate the quick spread of attacks through the entire system, potentially causing widespread disruption and loss of confidence.

Fintech firms that rely heavily on new digital technologies can make the financial industry more efficient and inclusive, but also more vulnerable to cyber risks.

In that light, I forecast that serious organizations worldwide will continue to spend on preventing, detecting, and dealing with cyber threats, particularly to protect the valuable “data” of both its customers and employees, in a very data-centric business world. This is an opportunity for firms like Akamai Technologies to fill that existing need.

But don’t just take my word for it… Seeking Alpha analyst Richard Durant’s April 27 analysis of Akamai Technologies also reiterated a similar tone:

Cybersecurity is an ever present issue for every organization, and even through macro uncertainty, demand is likely to continue to increase. DDoS attacks are increasing and becoming larger. Bot activity remains elevated post-pandemic, and application and API attacks are increasing.

For Dividend Investors, This Stock Does Not Pay Any

If you have been following my articles on Seeking Alpha, you know I have a preference for dividend-paying stocks, because I believe it is sign of a company who is in a strong position to return capital back to shareholders consistently each quarter. This also creates a recurring income source for shareholders for simply holding the stock.

With that said, based on its dividend page on Seeking Alpha, this company has not offered any dividend to shareholders, and does not have any coming up.

By comparison, if you are an investor in the tech sector overall, several other companies in the tech sector do offer a dividend: Microsoft’s dividend yield is currently 0.87%, the yield for Cisco Systems (CSCO) is 3.28% , and the yield for Intel (INTC) is 1.73%.

My preference for investing in dividend stocks when possible is a sentiment shared also by American investor Warren Buffett and Berkshire Hathaway.

According to a May 18 article by Morningstar:

The investor has achieved legendary long-term returns with a strategy that values dividend yield.

A recent article in the Wall Street Journal estimates that Berkshire Hathaway in 2023 is expected to receive $5.7 billion in dividends from its $300 billion equity portfolio.

So, with that said, I would not put a Buy rating at this time on Akamai Technologies or add it to my portfolio as it offers no dividends to shareholders, despite it being well past startup stage for over 20 years while many other tech companies do offer dividends.

The Company will Need to Improve Earnings and Balance Sheet in Next Few Quarters

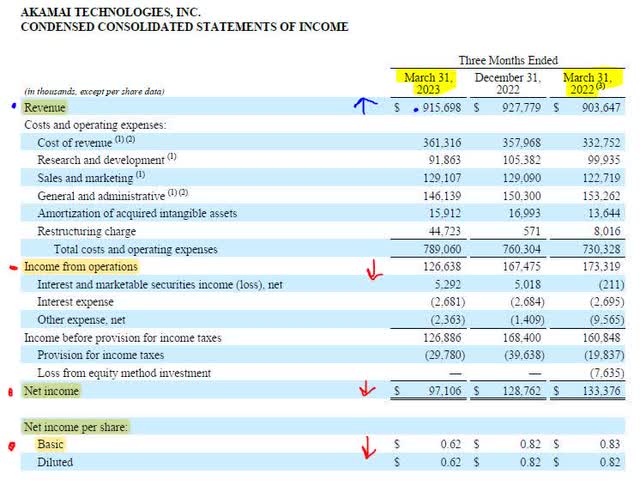

Another reason I am not rating this stock a Buy at this time, is because its most recent Q1 2023 results indicate room for improvement in their net income and balance sheet, while only showing a very modest revenue gain from the same quarter a year ago.

Here is a look at its most recent income statement below:

………………………………………………………………………………….

Akamai Technologies – Q1 2023 Earnings – Income Statement (Akamai Technologies)

………………………………………………………………………………….

As is evidenced, while revenue rose somewhat, both net income and earnings per share went down vs the same quarter a year ago.

One notable cost that sticks out is a “restructuring charge” of $44.7MM they were hit with in the first quarter. According to their earnings commentary, the charge was:

“related to severance costs in connection with a workforce reduction to enable prioritization of investments in the fastest growing areas of the business. In addition, the Company continues to record facility-related charges as it reduces its real estate footprint due to its flexible workspace strategy.

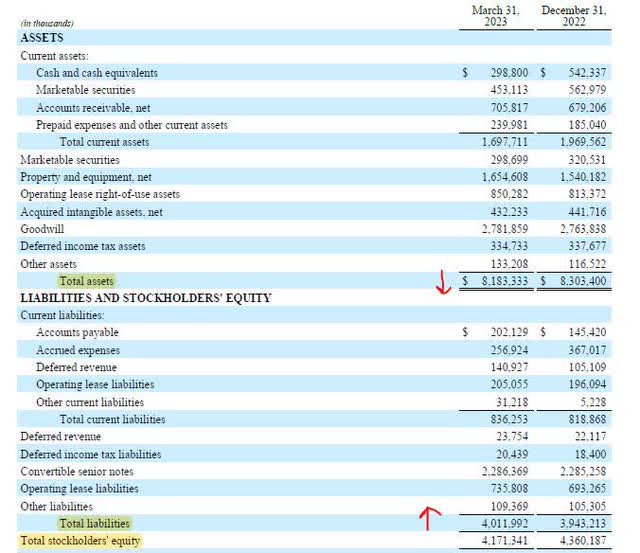

Next, below is the balance sheet:

………………………………………………………………………………….

Akamai Technologies – Q1 2023 Earnings – Balance Sheet (Akamai Technologies)

………………………………………………………………………………….

As is shown, there was a drop in total assets vs the prior quarter, as well as a rise in liabilities, and a reduction in stockholder equity.

Why should an investor care about the income statement and balance sheet?

From a forward-looking perspective, it gives me some framework into whether it is a well-managed company financially, but also if it will continue to be solvent and viable as an entity.

My opinion on the importance of looking at financial statements was highlighted by a May 2020 article from Harvard Business School:

Accountants, investors, and business owners regularly review income statements to understand how well a business is doing in relation to its expected future performance, and use that understanding to adjust their actions. A business owner whose company misses targets might, for example, pivot strategy to improve in the next quarter. Similarly, an investor might decide to sell an investment to buy into a company that’s meeting or exceeding its goals.

In that regard, I will continue to track Akamai Technologies in the coming quarters to see what “pivots” management makes to reach its targets going into 2024.

This Stock has Hold Potential due to an Upward Price Trend

Let’s talk about a trading strategy an investor can consider. Take a look at the most recent price chart as of May 18 for this stock, taken from the StreetSmart Edge trading platform:

……………………………………………………………………………………………..

Price Chart – Akamai Technologies (StreetSmart Edge trading platform)

……………………………………………………………………………………………..

In an earlier article I mentioned well-known trading concepts called the golden cross and death cross. In the above chart, I circled all of these crosses, where the 50 day simple moving average (solid dark blue line) crosses the 200 day simple moving average (solid dark red line).

These crosses are known for being lagging indicators of bullish or bearish trends, the golden cross being bullish and death cross being bearish.

For example, the death cross of late May 2022 was followed by a downward price trend staying below the 200 day moving average, followed by a reversal lately which points to the possibility of another golden cross being formed soon, though not guaranteed of course.

If you had acquired this stock between late February 2023 and early May, for example, and you continue to Hold it through the next golden cross formation, it creates a good Sell opportunity at that point for you to achieve a capital gain.

For example, if you bought at $75 and hold it until it hits $90, which I think it could do soon if there are a few days of tech-sector rallies, then that’s a 20% profit on your trade.

Another reason I rate it a Hold and not a Sell, is because I think the golden cross formation will occur, followed by another death cross if tech stocks sink in the next quarter. A 2-day rally in tech stocks sometime in late May and early June could be just the tailwind it needs for an investor to sell shares at a gain, then redeploy that capital.

After taking the capital gain, I would redeploy that capital to a dividend-paying tech stock perhaps after the next dip in prices, giving you a tech stock that pays over a 3% dividend yield at least.

Risks to my Hold Rating on this Stock

Risks to my neutral / hold outlook would be that the company decides to start offering an attractive dividend to shareholders, as well as its next few quarterly earnings reports being wildly better than analyst expectations, combined with its stock surging later in the year, driven by investors being bullish on tech stocks again. That scenario would have made the current price a good buy opportunity.

However, my counterargument is that we don’t yet know if there will be that kind of rally in tech stocks this year or not, and overall equities markets are still wrestling with Fed decisions on rates, inflation numbers, war in Europe, and the debt-ceiling debate in Washington.

While short tech sector rallies may happen in periods of volatility, my skeptical view of a longer-term tech sector rally was shared by major bank analysts in a May 16 article in Business Insider. According to the article, “analysts at top banks including Morgan Stanley (MS), JPMorgan (JPM) and BofA (BAC) warn the sector faces a selloff as a recession looms.”

Chris Toomey, a Managing Director at Morgan Stanley, also echoed this view in the article:

I don’t think the technology industry is immune from the overall economy,” he said, adding that the US is heading into an earnings downturn and is vulnerable to an economic slump.

Conclusion

In conclusion, I reiterate my Hold rating on this stock.

It is worth holding on to due to its strength in the cybersecurity segment and its current price showing signs of an upward trend. However it is not a Buy in my opinion as it does not offer dividends despite being in business since 1998, and it currently could use some improvement to its balance sheet and net income in the next few quarters of 2023.

As already mentioned, risks to my outlook are that its next few quarters are superb, it decides to offer a dividend, and there is a bull run on tech stocks overall.

I am not convinced that that will happen, but I am certain.. as I have shown evidence for.. that our critical infrastructure will continue to need cybersecurity vendors and as investors and analysts looking forward towards 2024 we should at least keep an eye on Akamai Technologies, as it continues to keep an eye on cyber threats to our world.

Read the full article here