Artisan Partners Asset Management (NYSE:APAM) has carved a niche with its boutique approach and specialized teams. However, its heavy reliance on equities, recent AUM decline, and negative net client cash flows highlight vulnerabilities.

Despite its consistent dividend distributions, its decade-long dividend CAGR of 3.6% may not appeal to those seeking stable returns. Given the perceived lack of risk-adjusted returns and market unpredictability, the recommendation is to sell, as investors might find more secure and rewarding opportunities elsewhere.

Artisan Partners Asset Management Overview

Founded in 1994, Artisan is a global investment management firm headquartered in Milwaukee, Wisconsin.

Managing investments on behalf of institutional and retail clients, the firm provides a range of equity, fixed-income, and alternative investment options. Its primary revenue source is management fees derived from its Assets Under Management [AUM].

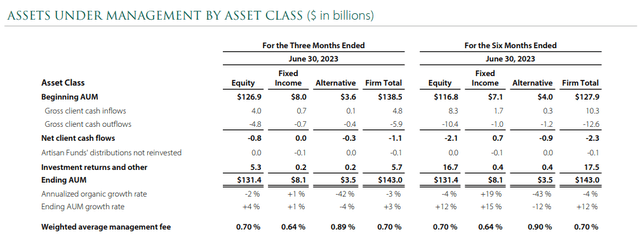

The vast majority of its AUM is in the equities asset class. In the second quarter of 2023, equities accounted for $131.4 billion of its total $143 billion AUM, which is 91.8%. Additionally, 75% of its clients with equities investments are based in the United States.

Artisan Investor Presentation

Artisan adopts a boutique investment style, with specialized teams for each asset class. Unlike giants like BlackRock or Vanguard, which prioritize client inflows, Artisan emphasizes investment results to grow AUM.

The company also distributes 80% of its quarterly cash generated as dividends, retaining a small portion for business growth. There has been a substantial special dividend paid at the end of most financial years.

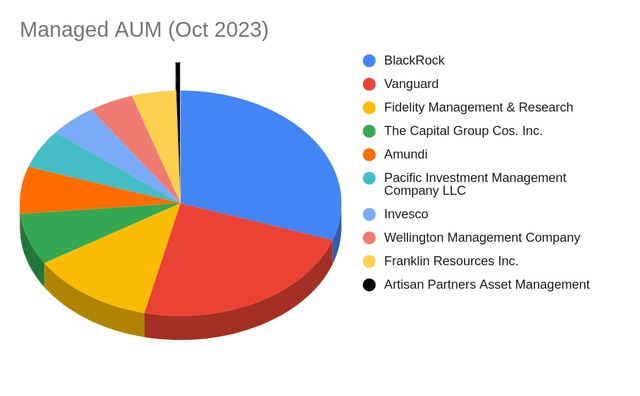

Consequentially, its AUM is $136.5 billion, a mere 1.44% of Blackrock’s $9.425 trillion. Among firms ranked by the Sovereign Wealth Institute, Artisan stands at #52 out of 100 studied firms based on this metric.

Author supplied

| Company | Managed AUM (October 2023) |

| BlackRock | $9,425,212,000,000 |

| Vanguard | $7,250,000,000,000 |

| Fidelity Management & Research | $3,880,000,000,000 |

| The Capital Group Cos. Inc. | $2,300,000,000,000 |

| Amundi | $2,101,000,000,000 |

| Pacific Investment Management Company LLC | $1,740,000,000,000 |

| Invesco | $1,483,000,000,000 |

| Wellington Management Company | $1,400,000,000,000 |

| Franklin Resources Inc. | $1,387,700,000,000 |

| Artisan Partners Asset Management | $136,500,000,000 |

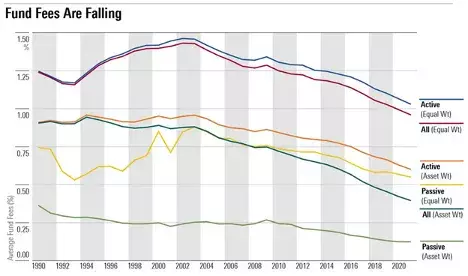

Artisan’s competitive advantage stems from its agile team size and deep specialization in investment strategies. This allows it to deliver significant value to clients and charge higher fees than industry norms.

The firm has maintained a 0.70% average management fee, even as industry fees have declined. For instance, US equities’ average fees dropped from 0.70% in 2018 to 0.61% in 2022, and overall fund fees went from 0.70% to 0.59% over the same period.

Morningstar

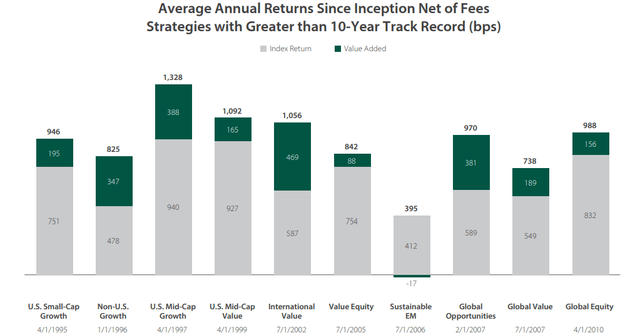

What justifies these higher fees are strong average returns provided to investors across the majority of its investment strategies.

Artisan investor presentation

The top three strategies by value-added at Artisan are the Emerging Markets Debt Opportunities with 1,010 bps, the Global Unconstrained Strategy at 759 bps, and the Credit Opportunities Strategy with 708 bps.

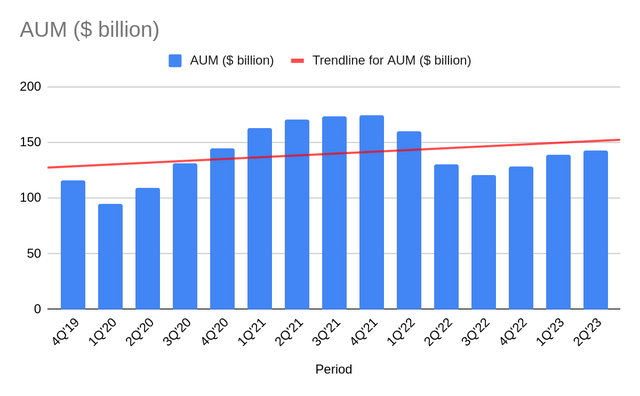

The chart below shows the fluctuations in AUM over the past 3.5 years. While AUM experienced a CAGR of 5.71% from 4Q’19 to 2Q’23, it also underwent periodic variations.

Author supplied

I conducted research on this article when Artisan’s AUM dropped from $142.8B at the end of August to $136.5B. This 4.4% decrease in AUM was announced just a couple of days ago. Prior to this drop in AUM, the company reported a $1.1 billion in net client cash outflows.

Net client cash flows are like the water level in a bucket. If more water (money) is poured in than taken out, the level rises (positive flow). If more water is taken out than poured in, the level drops (negative flow).

The last time these net client cash flows were positive was back in 1Q’22 at $0.7 billion. We can therefore deduce that its growth in AUM from 3Q’22 to 2Q’23 were exclusively investment returns, as clients had taken more money out than what they had put in.

Author supplied

Why sell APAM?

Based on what we’ve discussed so far, some of the premises for my thesis are the following:

- The company’s success hinges solely on outperforming passive benchmarks and delivering value to customers.

- If they don’t outperform, their value proposition becomes destructive. Customers can easily switch to more affordable options, questioning the value of paying a premium.

This then forms a base hypothesis: Artisian’s AUM is now particularly vulnerable to market downturns due to a lack of client cash inflows. AUM could decrease due to investors avoiding the market, withdrawing funds, and the reduced value of the managed assets. A triple hit.

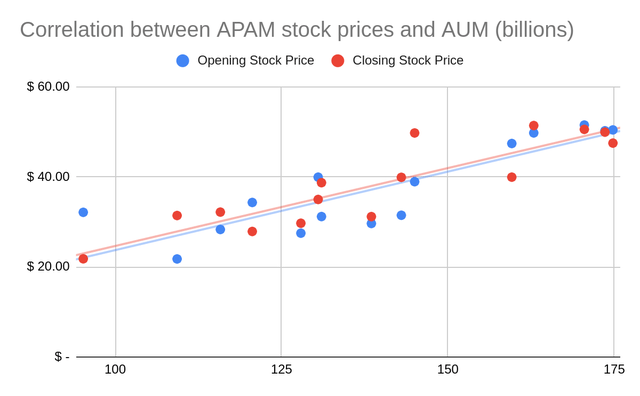

Artisan’s AUM growth overwhelmingly stems from equities investment returns. Analyzing its relationship with the broader market can provide insights into future expectations.

From looking at the chart below, you can see a strong correlation between Artisan’s AUM and opening and closing stock prices.

Author supplied

| Opening Stock Price Correlation |

Closing Stock Price Correlation |

| 0.859 | 0.889 |

While correlation indicates a relationship between two variables, it doesn’t imply that one causes the other. Just because they move in tandem doesn’t mean one directly influences the other.

Therefore, a falling AUM doesn’t guarantee that the stock price will fall by a proportionate amount either. However, investors might eventually associate a declining AUM with reduced management fees and smaller dividends, impacting total returns and prompting a sell-off.

Given this, Artisan faces significant risks, regardless of market direction. If there’s a downturn, the consequences could be severe. Negative net client outflows during a bull market raise concerns about their extent in a bear market. Moreover, in a stagnant market, AUM growth could still be challenging.

Given these risks, it’s debatable whether investors are receiving appropriate returns for the risks they’re taking on.

Dividend Growth Potential

Artisan’s primary appeal is its quarterly and special dividends, though its capital appreciation is an added benefit.

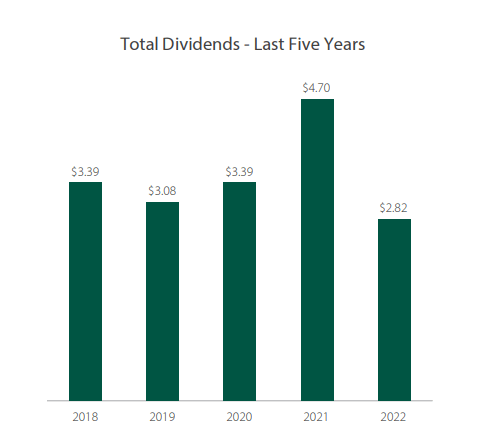

Over a ten-year period, the CAGR for the dividends over the five-year period is approximately -4.5%. This does account for events such as COVID, which skews the results.

Artisan investor presentation

Over a ten-year span, the results are somewhat better, though not particularly impressive. The dividends have a CAGR of approximately 3.6% over this decade, which is notably higher than the inflation rate of 2.48% during the same timeframe.

Author supplied

It’s important to note that dividends are paid from the cash generated within that specific year and quarter. Thus, a decline in the stock price could impact both dividends and capital growth.

Risks

Artisan has consistently demonstrated its commitment to shareholders by distributing dividends, both on a quarterly basis and through special dividends. By selling the stock, investors would be relinquishing the opportunity to benefit from this potential future dividend income.

On the other hand, the stock market is inherently unpredictable, and timing it perfectly is a challenge. Making decisions based on short-term market fluctuations or recent changes in AUM can be shortsighted. Selling the stock based on transient trends might mean missing out on the company’s future growth and potential rebounds. It’s crucial for investors to adopt a long-term perspective as to whether they are getting the appropriate risk-adjusted return.

Conclusion

Artisan offers a unique boutique investment approach, emphasizing outperformance and consistent dividend distributions. However, recent performance and market unpredictability cast doubts on its future. The firm’s reliance on equities and vulnerability to market downturns, especially with declining AUM and net client cash flows are concerns. Despite a decade-long dividend CAGR of 3.6%, Artisan may not be ideal for those seeking stable dividends. Investors might find more secure alternatives elsewhere.

Read the full article here