Introduction

Barnes & Noble Education (NYSE:BNED) shares have fallen 32% YTD. Despite the fact that the company’s stock has declined significantly from its historical peak in 2021, I believe that it is still not the best time to go long.

Investment thesis

In my personal opinion, now is not the best time to go long, because we may see pressure on the quotes in the following quarters, as the company has significantly decreased its guidance for Q4 2023 (fiscal) due to a decrease in both revenue and profitability. In addition, I believe that the sale of the DSS (digital student solutions) segment can make an additional contribution to the decline in gross profit, since the DSS segment is the most profitable at the gross margin level. Also, I see additional risks when switching to the FDC model (selling physical and digital textbooks in one set), since if students continue to increase the share of purchases of only digital textbooks, this may also have a negative impact on operating profitability. In addition, the company continues to show a negative level of operating profit.

Company overview

Barnes & Noble Education operates bookshops on university and college campuses. The main revenue segments are: retail, wholesale and DSS (digital student solutions). In addition, in addition to the proceeds from the core business, the company receives a portion of the proceeds as rental income. The main sales channels are both offline and online. The company operates in the US market.

3Q 2023 (fiscal) Earnings Review

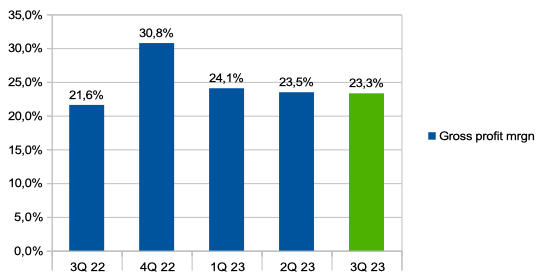

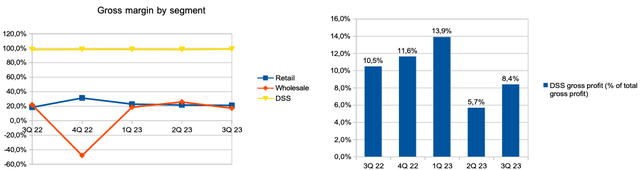

In the 3rd quarter of 2023 (fiscal), the company’s revenue increased by 11% YoY due to growth of 6.6% in the product sales segment and 76.6% in the rental income segment. Gross profit margin increased from 21.6% in Q3 2022 (fiscal) to 23.3% in Q3 2023 (fiscal). The main driver is the recovery of the gross profit margin in the retail segment, where the gross margin increased from 18.5% in Q3 2022 (fiscal) to 21.1% in Q3 2023 (fiscal), while in the wholesale segment the gross margin decreased from 21.9% in Q3 2022 (fiscal) to 17.1% in Q3 2023 (fiscal). You can see the details in the chart below.

Gross profit margin (Company’s information)

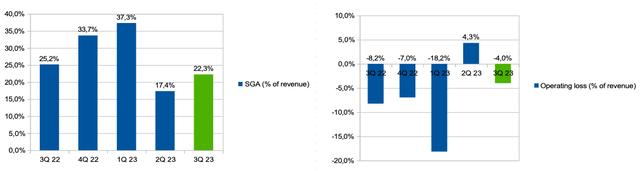

SGA spending (% of revenue) decreased from 25.2% in Q3 2022 (fiscal) to 22.3% in Q3 2023 (fiscal). I assume that the decrease in the number of personnel in December supported the reduction in operating costs. Thus, operating loss (% of revenue) decreased from 8.2% in Q3 2022 (fiscal) to 4% in Q3 2023 (fiscal). You can see the details in the chart below.

SGA & Margin trends (Company’s information)

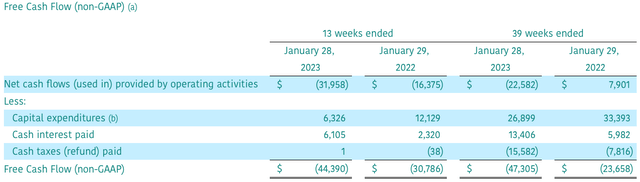

I would also like to draw attention to the fact that the company’s free cash flow continues to be under serious pressure. Thus, negative free cash flow increased from $30.8 in Q3 2022 (fiscal) to $44.4 million in Q3 2023 (fiscal). I believe that this is a serious risk for the company’s solvency, because the amount of cash on the balance sheet for the 3rd quarter of 2023 (fiscal) was $11.1 million. However, the company is currently closing a deal to sell the DSS division, which will net the company about $20 million, which should support the company’s balance sheet. The money will be used to pay off debt and replenish working capital.

Free cash flow (Company’s information)

My expectations

I would like to point out the fact that the company has lowered its guidance for the 2023 fiscal year. Following the release of Q3 2023 (fiscal) results, the company expected adj. EBITDA in the range of $20 million to $30 million, but at the end of May the company lowered its expectations to expect losses in the range of $10 million to $5 million. Thus. I expect a loss at the adj level. EBITDA in the range of $31 million – $36 million. The decline is due to pressure on revenue due to an unfavorable change in the product mix, the purchase of digital courses instead of physical textbooks, which puts pressure on both revenue and gross margin.

In addition, the company announced the sale of the DSS segment in order to focus on growth in volumes and profitability of the core business. On the one hand, I like the company’s strategy in the long term, on the other hand, despite the fact that the share of DSS segment revenue in the company’s total revenue is about 2% at the end of Q3 2023 (fiscal), the share of gross profit from the DSS segment is 8.4% in the 3rd quarter of 2022. So, I believe that selling the DSS segment may be a strategically sound decision, however, in my personal opinion, this may lead to pressure on gross profit in the coming quarters.

Margin trends (Margin trends)

According to management’s announcements during the Earnings Call following the release of quarterly financial results, the company is taking a number of strategic initiatives to achieve revenue growth and margins, however, this may take time.

While some of the strategic initiatives we are implementing will take time and results won’t be linear, we’re taking the appropriate actions to deliver consistent and profitable long-term growth.

In addition, I am alarmed by the fact that the CFO of the company left his post.

Risks

Margin: an unfavorable change in the product mix in favor of online products can lead to both lower revenue and pressure on operating margins. In addition, the sale of the DSS segment may lead to pressure on the gross margin, as the share of gross profit from the DSS segment is about 8.4% in Q3 2023 (fiscal).

COVID: a decline in school attendance or a transition to a remote format could lead to a significant decrease in both revenue and profitability of the company, because a large proportion of students will prefer to buy electronic textbooks, where the return on sales is lower than in physical textbooks.

Solvency: negative operating margin and negative cash flow can lead to additional share issue or even bankruptcy of the company, which is one of the main risks of this small cap company.

Drivers

Revenue: the company plans to continue increasing school outreach through the FDC model in the fall, which could help drive revenue growth going forward.

Margin: moving to an FDC model (selling both physical and digital courses in bundles) and reducing fixed operating costs can support the operating margin of the business. Thus, the company plans to achieve a positive level of adj. EBITDA for 2024.

Valuation

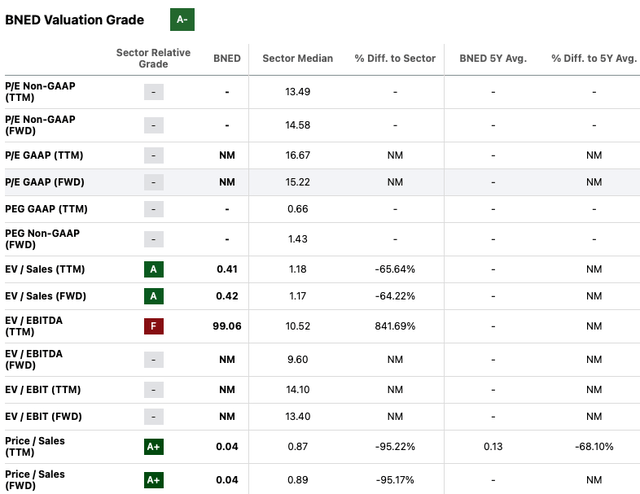

At the moment, we can only use P/S, EV/EBITDA and EV/Sales multiples to value a company. We cannot use a P/E multiple since the company has a negative net income. I believe that using the EV/EBITDA multiple now is also not rational, since EBITDA is at an abnormally low level, so the multiplier is extremely high. Under EV/Sales (FWD) and P/Sales (FWD) multiples, the company trades 64% and 95% cheaper than the sector median, respectively. I believe that the current valuation level is abnormally low, which, in my personal opinion, limits the potential downside.

Valuation (SA)

Conclusion

In my opinion, now is not the best time to open long positions, despite the decline in quotes. I believe that it is necessary to wait for the publication of financial results for the 4th quarter of 2023 (fiscal) before making a decision to buy shares. So, I would like to see the company’s guidance next year in order to understand more precisely how the transition to the FDC model can contribute to improving profitability, as well as to understand more precisely how much the gross margin will decrease after the sale of the DSS segment. However, the company’s quotes have declined significantly from their historical peak in 2021, so I stick to the HOLD recommendation, not Sell.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here