Introduction:

In my prior articles on Whitehaven Coal (OTCPK:WHITF) (here (Jun ’23) and here (Dec ’22)), I rated the Company as a Buy due to its strong fundamentals and its strong but now-ceased share buyback program, while also noting a couple visible risks and the stock’s less-than-ideal technicals.

Today, however, I am upgrading my rating of the company to a Strong Buy, as the Company is still cheap, coal prices look set to rebound, and the Company made a fantastic acquisition a couple weeks ago, expanding in both size and scope. I think WHITF shares are headed much higher, soon, I still hold my roughly 2/3 position, and I’ll be looking to add as I raise cash.

Global Coal / Gas Prices Stabilizing

Global coal and gas prices are still significantly elevated from pre-COVID levels, but they are refusing to come down any further. In fact, they seem to be threatening significant moves higher. As I have discussed in my prior articles, coal has both a fundamental supply/demand imbalance and a perception problem, and I believe these will persist until we either 1) come up with technological breakthroughs or 2) admit to our coal addiction and allow further capital investment.

Negative press around coal, along with ESG and sustainability mandates, have caused global financiers to shy away from funding coal investments, and the biggest mining corporations like BHP (BHP) and Glencore (OTCPK:GLCNF) have promised to slow and/or abandon coal investment. Less than 10 days ago, BHP’s Chair Ken MacKenzie said in an interview the Company is “exiting energy coal progressively.”

While this may be a “win” for environmental preferences, so far the results have also been higher prices. Below is the Newcastle Coal price in Green and Red, with the related Dutch TTF Gas price in slightly translucent Orange.

Author’s analysis, TradingView

As you can see, the price for both commodities remains stubbornly above 2021 levels, and even looks set to move higher. I am highlighting a few things from these charts that make me think the next move is UP:

- Volume for the front Newcastle Coal contract is starting to pick up at these prices (green circle),

- There are 3 separate positive divergences on the MFI and RSI indicators, marked in green, and

- The Dutch TTF gas price is already making new highs, and using the right-sided volume profile, if Newcastle can break through ~$160-165, there will be little volume resistance until $250 and then $350/t.

These are exactly the kind of setups you want to see if you have a bullish bias. Price/volume action, money flow, and momentum ALL seem to be confirming my fundamental analysis of a tight underlying coal market.

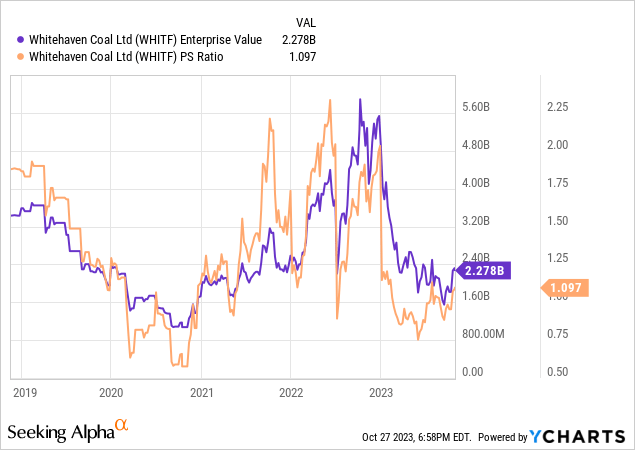

While WHITF has bounced from its lows, the Company is still trading at a valuation it has only seen for ~2 of the last 5 years (see chart below). As I wrote in my last article, “Whitehaven is trading at a lower valuation than much of 2021 – a year in which it went up almost 60% – and a lower valuation than its brief selloff in 2022, which preceded a 150% run. The Company is again Cheap.” These facts remain true, and any upward coal movement from here makes the equity almost absurdly cheap and a no-brainer long, in my humble opinion.

Transformational Transaction:

Up until two weeks ago, the WHC thesis was simple: earn lots of cash, and given the cheap valuation discussed above, plow it into the massive share buyback program to reward those willing to finance coal.

On October 17th, however, WHC made this strategy moot by announcing it would purchase the Daunia and Blackwater metallurgical coal mines from BHP for up to US$4.1B in cash. Briefly, the deal states WHC must pay $2.1B at closing (assumed mid-2024), $1.1B over the following 3 years ($500m, $500m, and $100m), and up to an additional $900m in performance considerations over time.

While this somewhat complicates the investment strategy for the Company, I think this will end up being a great deal for most WHC stakeholders. Not only did they get a good price for good assets in my opinion, this transaction is also transformational for the Company and executes on their long-term vision.

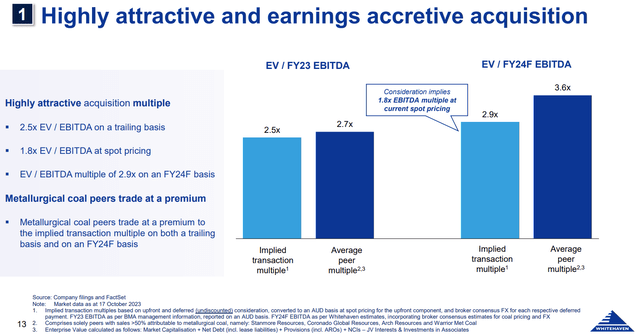

First off, let’s look at price: Whitehaven says the deal was done at below market multiples, and at spot coal prices, is under 2x EV/EBITDA:

WHC Presentation 10.23

Whitehaven is also saying the deal is accretive to EPS by 70% on consensus 2024 coal pricing, and by 160% at spot pricing! The deal is so accretive because Whitehaven simply was carrying most of this cash on its balance sheet. It is now immediately “putting it to work.”

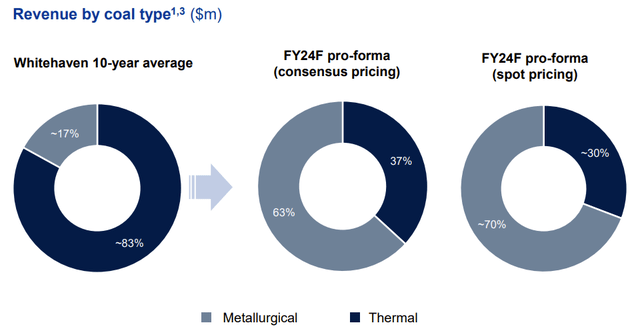

Secondly and perhaps just as importantly, the transaction immediately transforms Whitehaven from a 90% thermal coal producer (2022) to a roughly 70% met coal producer (FY24F), in line with the long-term corporate strategy:

Whitehaven Coal Presentation 10.23

And while I do believe the “death of coal” is exaggerated, thermal coal is still increasingly off-limits to the investment community. Met coal, on the other hand, is seen to have more duration and durability, as steel forecasts continue growing out to 2040, 2050, and beyond. Transforming into a met coal producer helps “de-risk” Whitehaven for many investors (including myself).

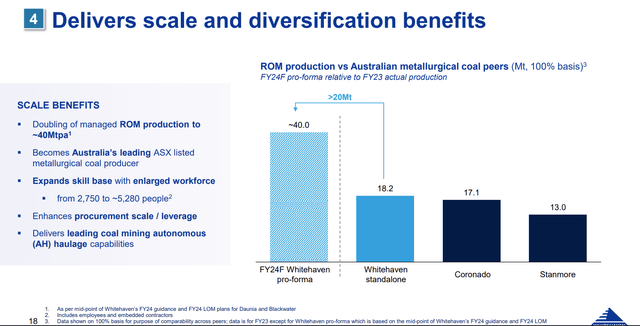

Finally, I want to note this purchase essentially doubles Whitehaven’s annual coal production/sales, and makes WHC the leading ASX met coal producer.

WHC Presentation 10.23

This is important for an industry in decline like coal, as size and margins will matter significantly to maintaining production. With additional size, Whitehaven can maintain bargaining power and its margin profiles as coal continues to mature.

I will add here that almost exactly 2 years ago, BHP executed a similar but smaller met coal divestment with Stanmore Resources (OTCPK:STMRF), another holding of mine. Upon deal closing, the stock jumped roughly +150% and has run another +140% from there!

Author’s Analysis, TradingView

While several factors differ between Stanmore’s purchase and Whitehaven’s, to me this is simply more good evidence of value accretion for met coal buyers right now.

Technical Analysis

So given all of these bullish factors, where can WHC stock go? Readers of my previous articles will know I like to use a combination of fundamental and technical analysis to determine potential paths. I am pretty happy with the results in my articles so far and hope readers feel the same.

Taking a fresh look at the chart, I’ve marked it up and made some notes below (note it is adjusted for dividends):

Author’s Analysis, TradingView

TA Notes:

- This chart is very bullish. First of all, I’ve highlighted with light green circles the new highs since February on all three of price, Money Flow (first indicator panel), and TSI (second indicator panel). It is somewhat rare to see all three making new highs together, there is usually a divergence or two; this signifies a strong upward trend.

- Secondly, there are positive divergences in all three of our panels (price, money flow, and momentum), indicating buyers are stepping in at higher prices and are unwilling to let the stock fall further before accumulating.

- Third, the volume profile on the right side of the screen shows that WHC has already broken above its biggest volume node and is currently chewing through its second. Once it gets above this node, it has the ability to “slide” upward with little resistance.

- I do see one negative / reason for pause with this chart, which is the lack of broad volume stepping in on the recent moves upward. Because I know the Company has been buying back so much stock, I think this is less concerning than it otherwise might be.

As you can see, in a bullish scenario (green path), I think $WHC.AX can get to $12 by next summer, representing a +55% increase from time of writing. In a more muted scenario, I still think WHC does well and can gain +25% or so in the next 6-9 months, even in the face of a choppy market.

Closing

In summary, I think investors are currently getting a great deal on WHITF shares, and both underlying price inflection as well as a larger, de-risked Company means this stock is set to materially outperform the indices. I am excited and hope other holders are, too.

Thank you for reading, and as always, consider what’s best for your risk tolerance, time horizon, and overall portfolio before making any financial decisions. Do not make decisions based on any one viewpoint, including mine. I often like to be active in the comments so leave your thoughts or questions below if you care to.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here