Co-produced by Austin Rogers.

We think it is safe to say that there is a high degree of uncertainty about the long-term future level of inflation. Will inflation be high, low, or somewhere in the middle going forward?

As for the short term, most CEOs are predicting a recession in 2023, and recessions cause demand to decline sufficiently to result in lower inflation in virtually every case.

But outside of recessions, a fierce debate rages between various economists and market practitioners about where rates of inflation will land.

Beyond 2023, will inflation run hot or cold?

Candidly, more than at any time during the 2010s, there are credible cases to be made for multiple future inflation scenarios, ranging from high to low.

We have thoughtfully and intentionally curated a diversified portfolio of real estate investment trusts, or REITs (VNQ), that should collectively thrive in any inflation scenario.

| Scenario | Level of Annual Inflation |

| Low Inflation | 1-3% |

| Moderate Inflation | 3-5% |

| High Inflation | 5-8% (or higher) |

In what follows, we discuss the current debate raging about the future direction of inflation and highlight a handful of our highest conviction picks to outperform through each potential inflation scenario.

Debating The Future of Inflation

Low Inflation

On one end, you see the likes of Tesla (TSLA) founder Elon Musk, ARK Innovation ETF (ARKK) investment chief Cathie Wood, and Starwood Capital chairman Barry Sternlicht warning that the Federal Reserve’s aggressive rate-hiking regime is going to “empty the ocean of water” (quoting Sternlicht) and cause serious pain in the economy.

This comes at exactly the time when, according to Wood, inventories are rising, input costs are falling, and year-over-year rates of inflation are coming down. As you can see below, the YoY CPI rates have been coming down consistently since their peak in the middle of the summer, especially for the Producer Price Index (orange line).

The idea here is that, now that the huge influx of stimulus money from 2020-2021 has been largely depleted, the Fed is ratcheting up the pressure at exactly the time when the economy would be rolling over anyway.

Though consumers were flush with cash in 2021 and into the first half of 2022, there are numerous signs that the consumer is nearly out of spending power.

For one, the U.S. personal savings rate now sits at a mere 3.5%, the lowest level going back to at least 1959.

The price hikes that have already taken place in the economy have eaten away at all the cash surplus consumers enjoyed over the past few years.

Now, rather than being cash-rich, consumers are exceedingly cash-poor. Hence we find credit card debt soaring higher at an alarming rate:

In short, the artificially inflated level of consumer demand for goods and services seen from mid-2020 to mid-2022 is over. Therefore, the primary force pushing up consumer prices in the U.S. is gone.

The “low inflation” scenario camp would argue that, at this point, the Fed is boxing against the shadow of inflation and that the real surge in inflation is fully behind us.

Beyond 2023? The low inflation camp would argue that the Five Horsemen of Disinflation will prevail over any lingering inflationary forces:

- Aging Demographics

- High Debt Loads

- Income Inequality

- Technological Innovation

- Globalization.

Aging demographics mean that the bulk of the population is past their prime spending years.

High debt loads indicate that nominal GDP growth will be lower, also weighing on inflation.

Income inequality reduces inflation because it means that a greater share of income and wealth is in the hands of wealthier people who tend to spend less as a share of their income.

Innovation, as Cathie Wood likes to point out, is inherently deflationary, because it finds ways to do more with less.

And, finally, the “deglobalization” trend we see playing out today is really just moving some manufacturing from China to friendlier countries and selectively onshoring production of certain strategic goods like semiconductors and green energy. Globalization creates too much efficiency to destroy.

High Inflation

For the most part, those in the “high inflation” camp, such as John Mauldin, do not dispute the idea that a 2023 recession will be temporarily disinflationary. But beyond that, they see several forces coming together to cause a secular inflationary cycle in a large number of commodities.

The primary cause of this inflationary cycle in commodities is the green energy transition.

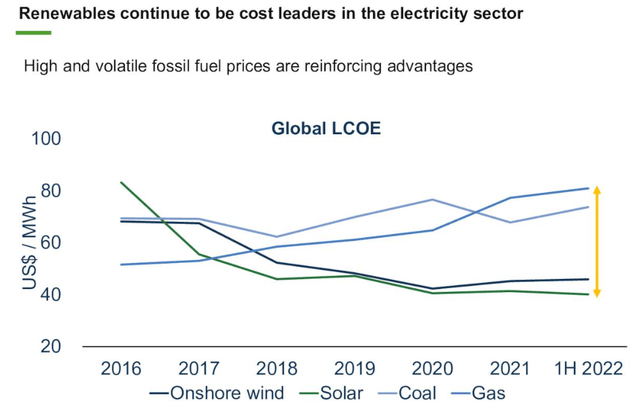

It is true, as Brookfield Renewable (BEP, BEPC) points out in its November presentation, that the levelized cost of electricity production from renewables has become significantly lower than fossil fuels in recent years.

BEP Presentation

But looking forward, the International Energy Agency recently forecast that the total amount of global solar PV installations over the next five years should roughly equal the amount of capacity installed in the 20 years from 2001 to 2021. This will create significantly more demand for the scarce materials required to produce these assets, like industrial and rare earth metals.

Already we have seen the prices of many metals soar in the last three years:

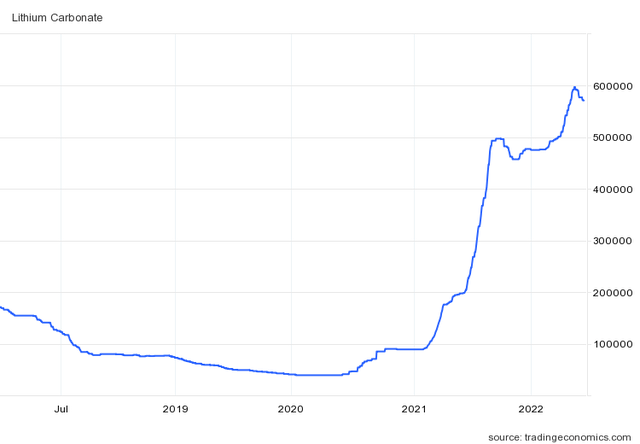

Not to mention the massive surge in price for lithium, which is a crucial material used in EV batteries and utility-scale battery storage systems.

Trading Economics

According to the “high inflation” camp, this should result in higher costs of power production in the years to come, as the all-in costs of EVs and renewables rise along with their input materials.

What’s more, cheap oil & gas won’t be able to swoop in the keep inflation low, because oil producers around the world are heavily emphasizing returning cash to shareholders rather than investing in long-term growth in production volume.

This is a sensible move for the oil producers because new oil rigs only pencil out as profitable over long time spans of multiple decades. But decades from now, the world will have moved heavily away from the use of fossil fuels, if government policies work as intended. Thus, in most cases, there is too great a risk of obsolescence before the end of the productive life of a new well to invest the huge sum of upfront money.

Hence we find that both U.S. and global oil production has still not recovered to its pre-COVID peak levels.

Oh, and the aging demographics that supposedly suppress GDP growth and consumer spending? The “high inflation” camp would argue that it won’t result in much of a drop in consumer spending because of cost-of-living adjustments in old-age benefits, and instead, it should exacerbate the labor shortage, thereby pushing up wages and spurring an inflationary wage-price spiral.

Moderate Inflation

Who is right? Will the “low inflation” camp or the “high inflation” camp prevail?

We do not think that investors should forget the possibility of the “middle ground” scenario – moderate inflation that is higher than the 1-2% levels of the 2010s but lower than the high inflation experienced over the past few years.

The “moderate inflation” camp could argue that, on one hand, it is true that massive government stimulus and money printing was a special circumstance and not necessarily the start of a long-term trend. Thus, the spike in inflation that resulted from it should prove temporary rather than a new trend.

On the other hand, the late 2010s era of cheap energy may never return, since oil companies aren’t prioritizing production and the requirement for certain materials should push up commodity prices that eventually trickle down into consumer prices.

However, high prices are spurring increases in the production of specific materials like lithium. Some experts believe the commencement of operations at new lithium mines next year should help bring prices down significantly.

These contrasting forces could very well come together for the remainder of the decade after 2023 to result in moderate inflation of around 3-5% annually.

REIT Investing For An Uncertain Inflation Outlook

The beauty of real estate investment trusts as an asset class is the level of diversity within it. In the world of REITs, there are some types that thrive in low inflation environments, others that thrive in high inflation environments, and others that are ideally suited for moderate inflation.

Therefore, we have intentionally shaped our portfolio to perform well in any inflationary scenario. To illustrate, we show the inflation scenarios in which a handful of our holdings perform best.

Example From Our Portfolio (For Illustrative Purposes):

| Scenario | Level of Annual Inflation | Examples of REITs That Thrive In This Scenario |

| Low Inflation | 1-3% | Realty Income (O); Agree Realty (ADC) |

| Moderate Inflation | 3-5% | Armada Hoffler (AHH); VICI Properties (VICI) |

| High Inflation | 5-8% (or higher) | BSR REIT (OTCPK:BSRTF), Farmland Partners (FPI), Whitestone REIT (WSR) |

Let’s go through each scenario to explain our thinking.

Low Inflation REITs

Net lease REITs like Realty Income and Agree Realty are ideal for a low inflation environment. They feature long lease terms with fixed rent rates and contractual rent escalations of only 1-2% per year. When inflation is low, interest rates are also likely to be low, granting these REITs a wider spread between their cost of capital and their acquisition yields.

Moderate Inflation REITs

AHH is a diversified REIT with a portfolio of multifamily, retail, and office property types with a particular emphasis on internally developed mixed-use town center-type properties. While its multifamily properties are able to raise rents rapidly in inflationary environments, its office and retail properties tend to have rent escalations limited to around 3-5% per year.

Meanwhile, VICI is net lease REITs with long lease terms. However, it features CPI-based rent escalations in their leases granting rate hikes that are much higher when inflation runs hotter. However, often these CPI-based rent hikes are capped at a certain level and that is why they are ideal for a moderate inflation scenario.

High Inflation REITs

Generally speaking, REITs with shorter lease terms have the ability to reset rents higher during periods of elevated inflation. Thus, BSR with its well-located, Class B apartments in the Sunbelt is one of the most inflation-protected stocks on the market for high inflation periods.

FPI, on the other hand, owns farms. These leases often have participation rents that entitle the landlord to a percentage of farm revenue above a certain threshold when crop prices are high. This effectively acts as high inflation protection.

Finally, for well-located, Sunbelt shopping centers such as those owned by WSR, the combination of 3%+ annual rent escalations and double-digit rent growth for new leases provides strong protection against inflation. That is especially true when WSR’s weighted average lease term sits at only 4 years, providing a steady stream of expiring leases to roll over at higher rates.

Bottom Line

The uncertainty about the future of inflation is greater today than at perhaps any time in the last decade. But we sleep well at night, knowing that our portfolio is prepared for any scenario.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here