A panic in the market, or even panic in a specific industry or sector, can be incredibly frustrating for investors who already have money in the game. But for those who haven’t bought in or who are looking to buy more, it can also represent a great opportunity. In March of this year, the banking sector saw what could only be described as a panic. Fear of contagion as some regional banks started failing caused shares across the industry to plummet. In some cases, the downside experienced was most certainly warranted. In other cases, I would argue, it was not. One example of the latter that I could point to is a fairly small bank called Civista Bancshares (NASDAQ:CIVB). Even now in early June, shares of the company are still down significantly from where they were earlier in the year. In fact, year to date, CIVB stock is down 30.8%. But yet when you dig into the actual data provided by management, there is no reason why, that I can see, that the stock shouldn’t move materially higher from here.

A small and misunderstood bank

According to the management team at Civista Bancshares, the company operates as a holding firm for Civista Bank. For its entire history dating back to 1884 when it was known as The Citizens Bank, the institution has been quite small. Today, for instance, the company, which is operated out of Sandusky, Ohio, has 41 different branches spread across two different states. Through these branches, the company provides its clients with a variety of services. These include, but are not limited to, providing customers with deposit and loan products such as checking accounts, money market accounts, time and savings deposits, safe deposit boxes, ACH origination activities, telephone banking, digital banking, and more. The firm also provides certain wealth management services for individuals, families, businesses, nonprofits, and more.

Author – SEC EDGAR Data

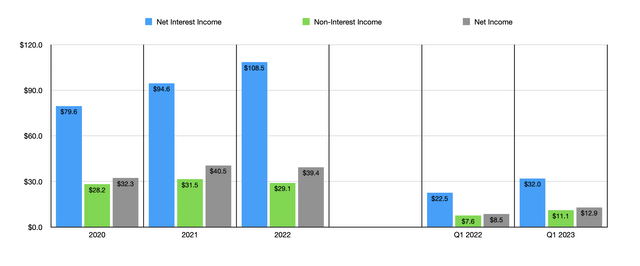

Operationally speaking, Civista Bancshares has done quite well for itself in recent years. From 2020 to 2022, for instance, net interest income for the company grew consistently, climbing from $79.6 million to $108.5 million. Over that same window of time, non-interest income remained rangebound between $28.2 million and $31.5 million. Net income managed to grow from $32.3 million to $39.4 million over this time. Some of this increase was driven by some acquisitions that the company had made along the way. And these acquisitions have been helpful in pushing up the overall asset base of the firm.

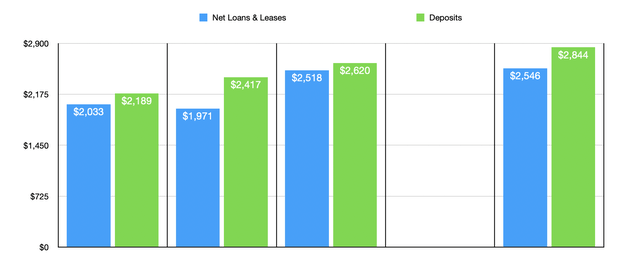

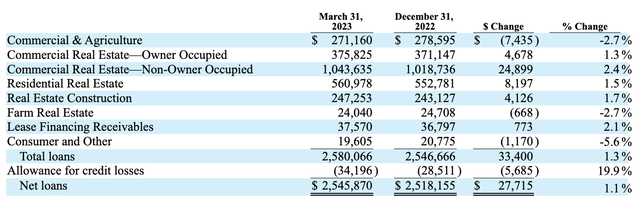

Focusing on loans for a moment, it’s worth mentioning that the greatest exposure for the company involves commercial real estate. From 2020 through 2022, the value of loans on its books grew from $2.03 billion to $2.52 billion. Of this amount, about $1.39 billion, or 54.6%, involves commercial real estate, with much of it classified as non-owner-occupied real estate. This on its own is a little undesirable since we don’t know how much of it is office based real estate. And right now, that’s not exactly a great space to be playing in.

Author – SEC EDGAR Data

Significant exposure to residential real estate, commercial and agriculture loans, and real estate construction loans. Of its total loan portfolio, 31.1% is classified as fixed rate. This means that the company has a large portion of its loans that are variable in nature. This is a double-edged sword. On the one hand, as interest rates rise, there is a higher probability that those paying the loans might default. But on the other hand, greater exposure to variable loans means with greater income in a high interest rate environment. On the deposit side of things, the company has also experienced growth in recent years. Overall deposits grew from $2.19 billion in 2020 to $2.62 billion in 2022. This makes sense since you cannot increase loans materially without having a growing deposit base.

While the past is most certainly important to focus on, it’s not the most important thing during these uncertain times. We also need to be paying attention to what has transpired to the company recently. The concern in the banking sector is that a high amount of uninsured deposits could lead to a banking failure because of what is called a bank run. This is where depositors, fearful that the bank might ultimately fail, withdraw their funds. And that can create something of a self-fulfilling prophecy. The good news for investors in Civista Bancshares is that there is no evidence of this transpiring.

Civista Bancshares

For the first quarter of the company’s 2023 fiscal year, the business had $2.84 billion of deposits on its books. This actually represented an increase of $223.5 million over the $2.62 billion that the company reported at the end of 2022. This came at a time when loans also increased, growing modestly from $2.52 billion to $2.55 billion. To make things even better, the exposure of the company to uninsured deposits went from low to even lower. At the end of 2022, 78.5% of its deposits were insured. That was a three-year high. But as of the end of the most recent quarter, that number grew further to roughly 83%. And so only around $483 million worth of its deposits are uninsured. By comparison, the company boasts $52.7 million in cash and $629.2 million of available for sale securities. This gives it plenty of liquidity even in the event that depositors withdraw their funds.

There are also some other positive things that the company has going for it. For instance, overall borrowings on its books came out to only $121.1 million at the end of the most recent quarter. That’s actually down from the $516.6 million that the company had at the end of last year. On top of this, the rise in interest rates, combined with higher deposits and greater loans, has helped to push revenue and profits up. Net interest income in the first quarter of 2023 came out to $32 million. That compares favorably to the $22.6 million reported one year earlier. Non-interest income grew over this time from $7.6 million to $11.1 million. All of this was instrumental in pushing net profits for the company up from $8.5 million in the first quarter of 2022 to $12.9 million the same time this year. Even ignoring the prospect of higher returns for 2023 as a whole, shares of the company look quite cheap. The price to earnings multiple of the company, using data from last year, is a rather low 6.2.

Takeaway

For the most part, I feel as though I have a pretty good ability to understand why a company’s share price is behaving in the manner that it is. Yes, I understand that there is general concern in the banking sector. But after the company reported results for the first quarter of its 2023 fiscal year, I have no idea why the stock has not moved higher. There might be rampant pessimism in the market right now. But with such a low amount of exposure to uninsured deposits, and with deposits expanding throughout the quarter even as concerns began to develop in the banking sector, it is shocking to me that shareholders were not rewarded for holding their units. Out on top of this how cheap the stock is, and I have no problem rating the company a ‘strong buy’.

Read the full article here