By Albert Grosman & Brian Lund

Investor Optimism Masks Risks of Higher Rates

Market Overview

Whatever happened to “Don’t fight the Fed?” U.S. equity markets rose across the board in the second quarter, with the Russell 2000 Index up 5.21%, the Russell 1000 Index up 8.58% and the tech-heavy NASDAQ Composite up over 13%. Among small caps, the companies with the lowest returns on equity (ROEs) jumped 11% in the quarter, those with no earnings 12%, and those with no sales 21%, according to Jefferies. Large caps outperformed small caps and growth outperformed value yet again, while IT, industrials, biotechnology and consumer discretionary industries led the value index. The outlook seemed to be one of low interest rates and avoiding a recession, a sort of Goldilocks combination.

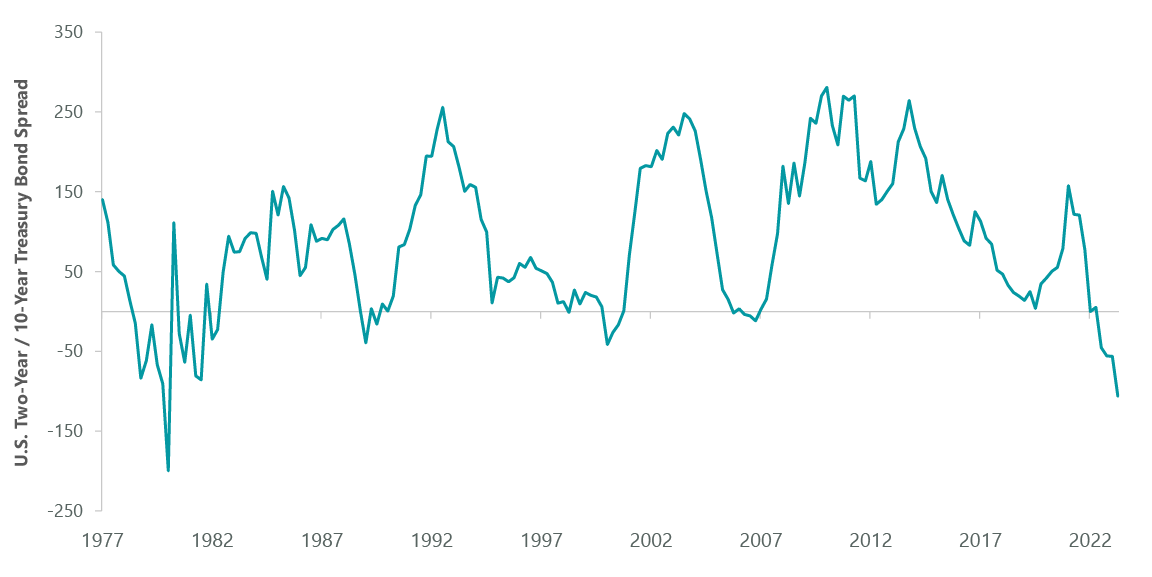

Meanwhile, the federal-funds target rate rose another 50 bps, with expectations for further increases this year, pushing the elusive and much anticipated easing cycle out of 2023 into 2024. The long-term bond rates didn’t keep pace, as the 10-year U.S. Treasury yield rose 37 bps and the 30-year just 21 bps. The result was the biggest inversion between the 2- and 10-year Treasury yields since the early 1980s (Exhibit 1).

Exhibit 1: Yield Curve Reminiscent of the 1980s

As of June 30, 2023. Source: Bloomberg.

The last two small inversions began in January of 2000 and 2006, both presaging recessions and drops in federal-funds rates and the equity markets, with the Russell 1000, 2000, and NASDAQ all down more than 7% annualized over the following three years. Yet, this time around, equity investors in the most speculative asset classes seem to think it’s time to buy, and bond investors want to anticipate Fed cuts years in advance by keeping long-term rates low.

As we wrote last quarter, these market movements are making it harder for the Fed to reduce rates. With long-term rates relatively low (10-year Treasurys rarely yielded 4% or less prior to the 2008 global financial crisis) and corporate investment-grade and high-yield credit spreads below their 20-year averages, financing is widely available and affordable, especially in light of ongoing inflation. Employment continues to surprise to the upside and wages continue to rise, creating all the conditions necessary for inflation to continue. The Fed has no reason to stop increasing rates.

The Fed has another tool it could use to address this conundrum: quantitative tightening (QT). It still has almost $7.7 trillion worth of long-dated Treasurys and mortgage-backed securities on its balance sheet, compared with $3.6 trillion prior to the March 2020 pandemic. While it has sold about $800 billion of securities from its peak a year ago, the Fed had to reintroduce a few hundred billion during the banking crisis in the first quarter. We believe that QT is perfectly suited to the situation where the Fed needs long-term rates to rise to slow economic growth. Those securities, however, are the backbone of a huge amount of investment portfolios, including in banks and insurance companies. An increase of 100 bps in the 10-year Treasury yield, which may be necessary to break this logjam, could lead to more failures in financial institutions or at least require more bailouts.

We believe the Fed will continue the path it has chosen so far — moving slowly to increase rates and trickle out its long-term securities, hoping the market will correct itself. However, it hasn’t worked so far, as inflation is not tamed, and the most vulnerable banks have already failed. The rubber band continues to stretch further, with yield-curve inversion at levels few investors have ever seen. We think the most likely outcome will be a sharp rise in long-term rates and higher overall interest rates than currently expected in market prices. The setup is not good for long-duration equities with high valuations and low returns/earnings — exactly the ones that outperformed in the second quarter.

“Quantitative Tightening is perfectly suited to the situation where the Fed needs to slow economic growth.”

Market enthusiasm for these types of companies notwithstanding, the ClearBridge Small Cap Value Strategy outperformed its Russell 2000 Value Index benchmark for the second quarter, as strong contributions from stock selection in the IT and financials sectors offset detractors from the health care sector.

Investor enthusiasm for AI-related companies and strong idiosyncratic catalysts helped drive our outperformance in the IT sector. Our top individual performer was SMART Global (SGH), which designs and manufactures specialty solutions for the high-performance computing, memory and LED markets. The stock caught the AI tailwind and got an added kicker from news it will sell the majority of its Brazil-based memory business to focus on higher-value products in computing and specialty memory. We believe the company is poised to deliver higher growth and better incremental margins than the market anticipates.

Another IT holding, Photronics (PLAB), also posted substantial returns for the quarter on the back of strong quarterly earnings and the AI-driven tech rally. Despite growing demand for high-end photomasks, the industry is capacity constrained and outsourced manufacturers such as Photronics stand to benefit. This has created a much more favorable environment for the company, which has shown increasing pricing power and longer-term contracts with major semiconductor manufacturers. We believe that the company’s investment and expansion of its manufacturing capabilities will allow it to continue to capture greater market share and extend its lead as the top merchant option in the industry.

The financials sector was also a positive contributor to relative outperformance during the quarter as fears of further contagion of March’s bank crisis eased and allowed for a rebound in many of the higher-quality small and regional banks caught up in the panic. For example, as investor pessimism dissipated, Bank OZK (OZK) exceeded analyst expectations and raised its quarterly dividend, highlighting continued improvement in its net interest income margin in the first quarter. We capitalized on the retreat in bank stocks early in the quarter to initiate a new position in regional bank First Horizon (FHN), which reflected a unique opportunity to buy a bank with an extremely strong capital and liquidity profile at a distressed value after its deal to be acquired by Toronto Dominion (TD) was canceled through no fault of First Horizon. While we continue to be vigilant for signs of further deterioration in the sector, we have high conviction in our holdings and believe that they will continue to be positive contributors to our long-term performance.

However, our top performers in the financials sector proved to be consumer-facing credit lenders, PROG and Oportun Financial (OPRT), which benefited as economic resiliency bolstered optimism for greater demand from customers. PROG serves as a lease-purchase solutions provider to underserved and credit challenged customers. It saw its stock price rebound after solid first-quarter earnings showed a normalization in prepayments and improved delinquency metrics. Likewise, Oportun Financial, which provides financial services through personal loans, auto loans and credit cards, generated positive returns after exceeding analysts’ expectations on top-line revenue, supported by an increase in customers.

Portfolio Positioning

We were active adjusting our positioning across sectors following our bottom-up, fundamental process.

We initiated a position in QuidelOrtho (QDEL), in the health care sector, which develops and manufactures diagnostic testing technologies and solutions. The current stock price discounts very modest long-term growth and no margin improvement. We believe that the combination of Quidel and Ortho results in a company that can produce steady growth over time via cross-selling opportunities, menu expansion across various platforms, and the introduction of a new molecular testing platform. Margins will expand over time as testing revenue grows and synergies are captured. In the near to medium term, however, we expect some noise in results due to fluctuations in revenues related to COVID-19 testing.

We also added Valaris (VAL), in the energy sector, which provides offshore contract drilling services to the international oil and gas industry. We feel the offshore drilling market is materially tightening, the industry has undergone substantial consolidation, and the company’s free cash flow is set to rapidly rise over the next few years against the backdrop of higher competition. We believe Valaris offers a compelling valuation given the underestimation of the company’s earnings potential.

We exited our position in Syneos Health (SYNH), a clinical research company that provides clinical trial services. The company’s share price has faced sustained pressure over the last few quarters due to difficulty in the company rebounding to pre-COVID testing levels and internal mismanagement. As a result, Syneos agreed to be acquired as part of a takeover deal with a private investment consortium, and we capitalized on the offer to sell and capture the premium offered by the acquirers as we concluded a higher offer was unlikely.

Outlook

Like Odysseus, forced to choose between sailing closer to the sea monster or the whirlpool, the Fed now also finds itself between Scylla and Charybdis. Either it keeps increasing short-term rates, pressuring consumers and businesses funded with floating-rate loans, or it ramps up QT and risks institutional instability. Despite an uptick in investor optimism, we see substantial evidence of turbulence underneath the market’s calm exterior and recognize the risks the rest of the market is discounting. We believe our approach of investing in companies with strong balance sheets, pricing power and managerial competence will allow us to persevere through whatever conditions emerge and generate attractive, long-term returns over the full market cycle.

Portfolio Highlights

The ClearBridge Small Cap Value Strategy outperformed its Russell 2000 Value Index benchmark during the second quarter. On an absolute basis, the Strategy had gains across seven of the 11 sectors in which it was invested during the quarter. The leading contributors were the IT and industrials sectors, while the utilities sector was the main detractor.

On a relative basis, overall stock selection positively contributed to performance. Specifically, stock selection in the financials, IT, materials and industrials sectors contributed to relative returns. Conversely, stock selection in the health care sector weighed on relative performance.

On an individual stock basis, the biggest contributors to absolute returns in the quarter were SMART Global, Photronics, PROG, Textainer (TGH) and Eagle Materials (EXP). The largest detractors were Heartland Financial (HTLF), Everi (EVRI), TriCo Bancshares (TCBK), WesBanco (WSBC) and Amarin (AMRN).

In addition to the transactions listed above, we initiated positions in Sterling Check (STER) and Janus International (JBI) in the industrials sector and exited positions in Mirum Pharmaceuticals (MIRM) in the health care sector and Heartland Financial in the financials sector.

Albert Grosman, Managing Director, Portfolio Manager

Brian Lund, CFA, Managing Director, Portfolio Manager

|

Past performance is no guarantee of future results. Copyright © 2023 ClearBridge Investments. All opinions and data included in this commentary are as of the publication date and are subject to change. The opinions and views expressed herein are of the author and may differ from other portfolio managers or the firm as a whole, and are not intended to be a forecast of future events, a guarantee of future results or investment advice. This information should not be used as the sole basis to make any investment decision. The statistics have been obtained from sources believed to be reliable, but the accuracy and completeness of this information cannot be guaranteed. Neither ClearBridge Investments, LLC nor its information providers are responsible for any damages or losses arising from any use of this information. Performance source: Internal. Benchmark source: Russell Investments. Frank Russell Company (“Russell”) is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Frank Russell Company. Neither Russell nor its licensors accept any liability for any errors or omissions in the Russell Indexes and/or Russell ratings or underlying data and no party may rely on any Russell Indexes and/or Russell ratings and/or underlying data contained in this communication. No further distribution of Russell Data is permitted without Russell’s express written consent. Russell does not promote, sponsor or endorse the content of this communication. |

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here