Introduction

Coty (NYSE:COTY) concluded its fiscal year 2023 on a high note, marked by a robust Q4 performance and exceptional results for the entire year. The company’s journey toward financial recovery, exemplified by a reduction in debt, harmoniously aligned with its commitment to continuous innovation, resulting in the expansion of market shares and sustained profitability across all key metrics.

Despite Coty’s commendable achievements, substantial untapped potential persists right now, especially in markets like Brazil and, on a longer horizon, potentially Asia too. The prospects of sales linked to travel following the post-COVID reopening further amplify the company’s growth outlook. The company appears poised for sustained expansion, indicating that its growth phase is far from reaching a plateau.

Analyzing Coty’s intrinsic value through a conservative lens uncovers compelling upside potential, affirming my view of it as an attractive investment opportunity. Furthermore, I consider the recent volatility in Coty’s stock a buying opportunity to load up on some Coty stocks right now.

In this article, a profound focus will also be directed toward Coty’s equity holdings, especially adding some thoughts regarding the true value of its SKKN stake.

This article’s premise centers on the notion that Coty is positioned as a long-term value proposition that has been successfully delivered on in its deleveraging turnaround so far.

Considering the culmination of these optimistic developments, a confident “buy” recommendation for Coty is warranted based on its current share price.

Coty Inc. Delivers Strong FY23 Results

Coty has once again showcased its exceptional performance through the recent publication of its fiscal year 2023 fourth-quarter and full-year results.

The company’s strong execution of its strategic growth pillars has yielded a remarkable twelfth consecutive quarter of outcomes that either align with or surpass expectations.

Amid the backdrop of ongoing macroeconomic uncertainties, the demand for beauty products remains steadfast, and there are no indications of consumers shifting towards lower-priced alternatives. Furthermore, the company’s “fragrance index,” similar to the famous “lipstick index” invented by Estée Lauder’s Leonard Lauder, has been tracked for over a year and demonstrates no signs of any deceleration. This notable achievement underscores Coty’s robust standing within the market and Cotys capacity to cater to the emotional needs of consumers.

Solid Revenue Performance and Margin Enhancement

Coty’s FY23 reported net revenues reached $5,554.1 million, reflecting an impressive 5% YoY growth, with core LFL revenue surging by a remarkable 12%. This growth was underpinned by core LFL growth of 13% in the Prestige segment and 11% in the Consumer Beauty segment. Additionally, the fiscal year 2023 reported gross margin ascended to 63.9%, marking an increase from the previous year. The adjusted gross margin also saw a commendable uptick of 20 basis points, reaching 63.9%. As I read the reports, this boost was mainly attributed to effective pricing strategies and supply chain productivity, even in the face of COGS inflation and negative FX impacts.

Coty reported operating income that more than doubled to $543.7 million YoY. Adjusted operating income surged by 20% to $738.8 million. While adjusted EBITDA witnessed a commendable 7% surge to reach $972.8 million, the robust performance of adjusted EBITDA outpaced recently revised guidance and initial EBITDA projections for the year, even in the face of over $70 million in negative FX impact on adjusted EBITDA.

Coty’s reported FY23 EPS of $0.57. Adjusted EPS nearly doubled to $0.53, supported by a non-operating EPS benefit of $0.15 arising from the equity swap’s mark-to-market valuation and a $0.10 expansion in underlying EPS, primarily driven by operational enhancements, as I view it.

Prestige Fragrances, Exceeding Expectations

Of particular note, Prestige fragrances emerged as a significant driver of Coty’s success, surpassing market projections for revenues. In the fourth quarter, the Prestige fragrance sector achieved remarkable expansion, soaring over 20%. This commendable growth trajectory persisted throughout the total fiscal year, delivering double-digit growth on a core LFL basis. This resounding achievement was widespread across all major brands housed within Coty’s portfolio.

In a strategic move, Coty further fortified its fragrance portfolio throughout FY23 with the expansion of many of its current licensees.

Expanding into the Lucrative Skincare Market

The spring of 2023 witnessed the initiation of Coty’s ambitious skincare acceleration strategy, characterized by the introduction of novel products and robust activations in markets for Lancaster and philosophy. These strategic maneuvers yielded remarkably favorable results, already driving double-digit revenue growth for both Lancaster and philosophy in the fourth quarter. Despite the initial hurdles posed by Chinese lockdowns, which impacted revenues for prestige cosmetics earlier in the fiscal year, the segment rebounded impressively in the fourth quarter, boasting a striking 25% LFL growth.

Growth Across all Global Markets

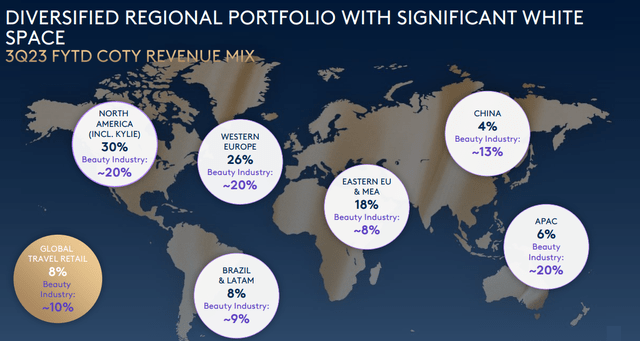

In terms of geographical performance, Coty achieved growth across all regions during both the fourth quarter and the entire fiscal year 2023. The Americas reported a solid 9% expansion as recorded, with a robust 10% LFL growth over the entire year. EMEA reported a modest 1% upturn, whereas core LFL growth surged by an impressive 13%. The Asia-Pacific region reported a commendable 7% growth and an even more remarkable 13% LFL growth.

COTY – Revenue Mix – Q3 23 FYTD (Coty Investor Presentation)

Notably, Coty’s performance in China, while currently contributing modestly to revenues, is particularly promising given the emerging middle class’s heightened interest in personal beauty expenditure. On the other hand, it might also be perceived as a plus that Coty not yet have strong sales exposure to Chinese markets, given the increasing worry about bigger turmoil involving China.

Within Coty’s geographical mix, a particular driver for Coty’s near-term future growth could be Brazil, with Coty having successfully established a market-leading position in Mass Fragrances while still facing immense potential for the years ahead.

COTY – Brazil Growth Opportunity (Coty Investor Presentation)

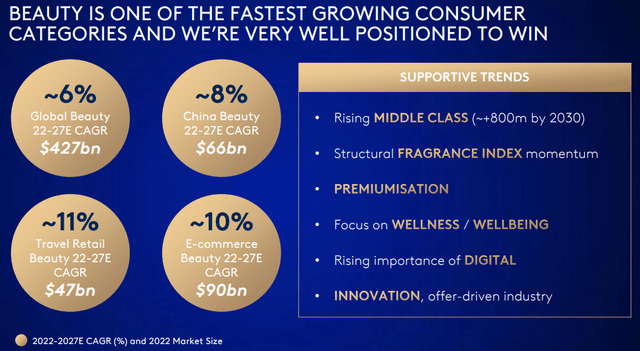

Beyond that Coty remains with immense white space opportunities meaning potential to capture additional market share of the growing beauty markets across the globe.

COTY – Quantified Market Potential (Coty Investor Presentation)

Deleveraging and Equity holdings

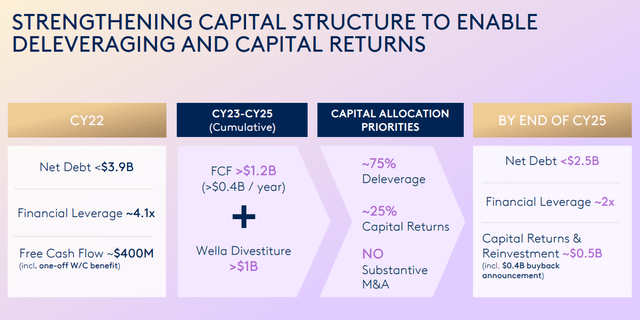

Coty’s financial net debt was reported at $4.0 billion by the end of FY23, reflecting a sequential improvement of $0.3 billion compared to the previous year.

The company’s unwavering commitment to active deleveraging was evident through its successful generation of $402.9 million in free cash flow during FY23. This robust cash flow generation played a pivotal role in driving down Coty’s financial leverage ratio, which stood at 4.1x by the end of Q4.

This marked a substantial improvement from the 4.7x recorded at the end of FY22 and the 4.4x reported at the end of Q3. These achievements have not gone unnoticed, as Coty received multiple upgrades from leading rating agencies.

The company remains on track with its deleveraging efforts and continues to reach its target of 2x Net debt financial leverage by CY25.

COTY – Deleveraging Guidance (Coty Investor Presentation)

Strategic Stake Divestiture: Wella Stake

An integral aspect of Coty’s strategic debt reduction roadmap involves divesting its stake in Wella. By the end of Q4, the value of Coty’s retained 25.9% Wella stake amounted to $1.06 billion. In line with Coty’s plan to fully divest its Wella stake by the end of CY25, a significant step was taken in July 2023. Coty entered into a binding Letter of Intent, committing to sell 3.6% of its Wella stake to IGF Wealth Management for $150 million. While the transaction is still subject to customary closing conditions, including consent by KKR. I think the deal is highly likely to go through, and it underscores Cotys commitment and capability to execute on its deleveraging plans for FY25.

SKKN Stake and Potential Impact on Economic Debt

Coty’s pursuit of an even stronger financial position by further decreasing its debt levels might also include its stake in SKKN, affiliated with Kim Kardashian. In 2020, Coty acquired a 20% stake in SKKN at a valuation of $1 billion.

Recent developments, including an announcement on July 11, 2023, of Kim initiating talks with Coty indicate that Coty is in discussions to potentially sell back this minority stake to SKKN. While the exact value of the stake in today’s context is not yet confirmed due to SKKN’s private status and lack of public information, noteworthy considerations arise. SKKN’s recent funding round placed its valuation at over $4 billion, underscoring its growth trajectory and appeal, especially to Gen Z customers. Sales are projected to reach $750 million in 2023, up from $500 million last year. Coty’s stake might have undergone dilution through subsequent funding rounds since 2020, yet I strongly suspect its value is substantially exceeding the initial purchase price.

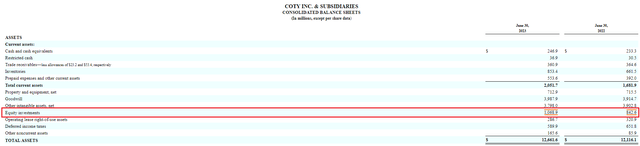

Coty’s “equity holdings,” accounted for on their balance sheet, where such minority stakes are supposed to be reflected, currently hold a value of merely about $1.06 billion.

COTY – FY23 Balance Sheet – Assets (SEC 10-k-filling)

This value obviously predominantly encompasses Coty’s Wella stake. However, especially Cotys SKKN stake, as I just discussed, could potentially bring this number substantially higher. Hence, the potential value of the SKKN stake could notably impact the economic net debt figure. Taking into account the approximate $1 billion Wella stake and the estimated value of the SKKN stake (potentially surpassing the $200 million purchase price), the resulting reduction in economic net debt could be far beyond the company’s calculated net economic debt number of about $3 billion. So an update on that and the potential that Coty might soon announce that it will sell its SKNN stake for a valuation significantly higher than its initial purchase price could lead to momentum in the company’s shares.

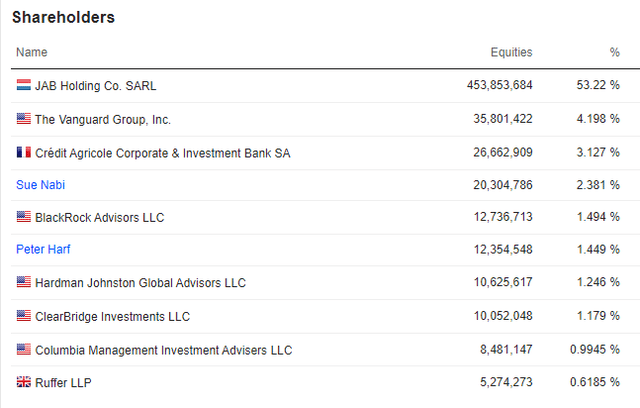

Strong Anchor Shareholders

At the executive level as well as within the board of directors, both the CEO, Sue Nabi, and the Chairman, prominent investor Peter Harf, hold substantial stakes in Coty, along with their other colleagues. Their personal investments amount to multi-million-dollar exposures to Coty stock. Notably, there have been several instances of insidershare purchases without a single sale over the entire year so far.

Sue Nabi possesses around 2.4% of all outstanding Coty shares, which are valued at approximately $240 million. Similarly, Peter Harf, who serves as both the Chairman of Coty and is affiliated with JAB Holding, the company’s largest shareholder, holds Coty stocks worth $150 million, equating to about 1.5% of the outstanding shares. This alignment of ownership ties their interests closely to the company’s performance, incentivizing decisions that benefit all shareholders. This aspect also contributes to my optimistic outlook on Coty’s future performance.

JAB Holding, which is the family office company with more than $50 billion in AUM and represents the interests of the German Reimann family-Reckitt Benckiser descendants-is the controlling shareholder of Coty.

JAB controls approximately 60% of Coty’s shares through various holding companies. The investment professionals at JAB played a crucial role in initiating Coty’s turnaround strategy a few years ago, which involved significant management changes aimed at bringing in skilled individuals from their network. Their active involvement underscores their dedication to the company’s resurgence, which has been successful so far.

COTY – Top 10 Shareholders – the remaining 8% are held through JAB subsidiaries, not apparent in this image. (Marketscreener)

In 2019, during a challenging period marked by operational declines and a sharp drop in share price, JAB acquired an additional 150 million shares for $11.65, ultimately making JAB the controlling shareholder of Coty that it is today. As they increased their stake from 40% to the current 60%, JAB Holding communicated their long-term approach and strong belief in the company’s strategic value as a long-term investment.

As of July 14, 2023, JAB announced that it had entered a multi-year Total- Return-Equity-Swap-Agreement in the vicinity of about 40 million Coty shares with a variety of banks in order to gain “long” exposure to Cotys share price performance. These transactions resulted in JAB obtaining additional synthetic exposure to approximately 5% of the outstanding shares of Coty.

Valuation Analysis

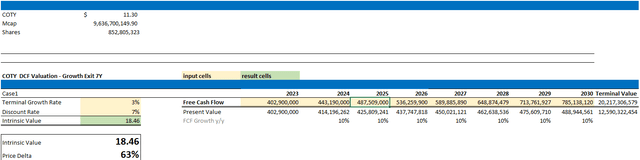

To determine a reasonable value target for Coty’s shares, I utilized a DCF model projecting Coty’s near-future Cash Flows and deriving an intrinsic value for its shares.

My focus is not on achieving pinpoint precision, but rather on identifying trends and providing insight into where Coty’s share price could reasonably trade if it aligns with the assumptions I’ve used.

These assumptions are built on a foundation of conservatism, though Coty’s history of excellent management execution suggests that they might be surpassed, as it has consistently demonstrated.

COTY – DCF Valuation (Author)

In my DCF analysis, I incorporated a growth exit window for Coty extending to FY2030 with a terminal growth rate of 3% onwards on the FCF level.

However, bolstered by promising financial metrics and growth prospects reported this year, this projection might be deemed conservative, especially considering the factors we discussed earlier. The potential for Coty to capitalize on the immense market share it can capture due to the ongoing growth in the beauty industry worldwide could lead to an extended growth exit timeline.

I find it reasonable to assume a FCF growth rate of 10% year over year. While the FCF margin is implied to be less than 10%, the continuation of current top-line revenue growth, coupled with effects like relief from interest payments resulting from Coty’s successful deleveraging efforts, might significantly elevate this margin in the coming years. Given the potential for Coty to further enhance its margins through operational improvements, this FCF margin assumption could even be seen as conservative.

With these assumptions in mind, our calculations yield a fair value of $18.46 per share. This valuation underscores a substantial upside potential, exceeding 60%.

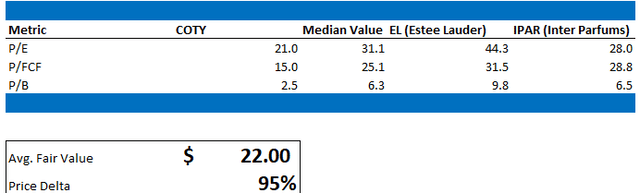

Furthermore, I proceed with a comparative valuation approach that compares key valuation metrics of Coty with industry peers Estée Lauder (EL) and Inter Parfums (IPAR).

COTY – Comparative Valuation (Author)

Significant disparities become evident when comparing Coty’s market valuation with those of its peers, as demonstrated in this calculation. While to some extent this discrepancy can be attributed to Coty’s volatile past, I believe that the current valuation gap is unreasonable and unsustainable over the long term. Considering Coty’s clear commitment to deleveraging, with an expectation to normalize debt levels by CY25, along with its overall excellent operational execution, the current valuation spread seems unjustified.

Both valuation methodologies converge on a singular observation: Coty’s potential is undervalued. In my view, a fair share price range of $18-$20 would be appropriate for the market to consider, offering a promising return in the near-term horizon. Additionally, if Coty’s progress and growth outperform the assumptions I’ve made here, there’s potential for an even higher fair share price, potentially propelling stock prices beyond this range.”

Risks

Coty operates in a fast-paced industry marked by high volatility. The beauty and cosmetics landscape witnesses trends that can emerge rapidly and fade just as swiftly. The company’s success hinges on its ability to consistently anticipate and navigate these trends effectively.

A potential risk stems from Coty’s reliance on a handful of key brands or products for a significant portion of its revenue. Any market saturation, Increased competition or a decline in the popularity of these brands could adversely affect the company’s overall financial performance.

Furthermore, Coty’s holdings, notably the $1 billion Wella stake, might also present uncertainties. Operational changes in Wella could impact the valuation of Coty’s retained stake. Unforeseen challenges or shifts in market conditions might affect the value of the Wella stake as well, thereby impacting Coty’s financial position. Due to the magnitude of Cotys Wella stake, this equity holds special importance.

Moreover, while I argue that the value of Coty’s 20% stake in SKKN is underestimated, this assertion of mine remains speculative due to the factual lack of information available. The valuation of SKKN is subject to uncertainties, and any unfavorable news or developments related to this stake could potentially affect Coty’s stock price adversely.

As for my valuation, the valuation model employed in this analysis is based on simplified assumptions. While these assumptions serve the purpose of projecting a fair share price trajectory for Coty, they inherently lack the accuracy of a more complex model. If Coty’s growth trajectory deviates from expectations, including slower top-line growth or challenges in converting sales to Free Cash Flow, the accuracy of the projected price target could be compromised.

Conclusion

In conclusion, Coty’s impressive fiscal year 2023 performance reflects a company in the midst of a dynamic transformation. The robust sales growth, fueled by Prestige fragrances and strategic maneuvers in the skincare market, underscores Coty’s resilience and adaptability. With strong growth across global markets and significant enhancements in financial metrics, Coty is poised to capitalize on emerging opportunities, particularly in markets like Brazil and Asia. The active debt reduction efforts, highlighted by divestitures and improved financial leverage, contribute to a strengthened balance sheet.

Coty’s holdings, particularly the Wella stake and the potential value of the SKKN stake, introduce an element of excitement and potential upside. The alignment of ownership interests among executives and shareholders instills confidence in the company’s trajectory. Furthermore, our comprehensive valuation analysis, encompassing both DCF and peer comparison approaches, underscores the potential for Coty’s undervalued shares to offer substantial gains.

Despite the industry’s inherent volatility and associated risks, Coty’s strategic positioning, operational resilience, and growth prospects warrant a confident “BUY” recommendation. The convergence of positive factors, including transformative operational achievements, focused deleveraging, and compelling valuation metrics, paints a picture of Coty as an attractive investment opportunity. As the company forges ahead with its strategic initiatives and capitalizes on the resurgence in beauty product demand, the potential for investors to benefit from Coty’s continued growth appears robust.

Read the full article here