Danske Bank A/S (DNSKF) is currently trading at a much lower valuation than its Nordic peers, while the resumption of dividends could be an important catalyst for a higher valuation in the medium term.

Business Overview

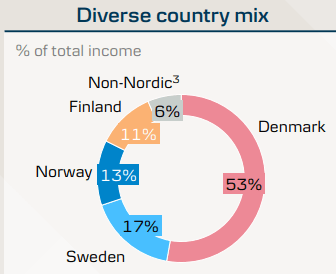

Danske Bank is a Danish bank, operating in its domestic market and other Nordic countries, plus Northern Ireland. It’s the largest bank in Denmark and the market leader, with a market share of about 24%. It has also a sizable position in Finland, where it’s the third largest bank with a market share of around 10%, while in Sweden and Norway it has a smaller market share (around 5% in each market) and considers itself as a challenger player in the market.

Geographic mix (Danske)

Its current market value is about $21 billion, being a mid-sized bank in Europe by this measure, and trades in the U.S. on the over-the-counter market. However, investors should be aware that its shares have higher liquidity in its domestic listing, making this the preferred way to trade its shares.

Danske’s core business is retail and commercial banking, having about 3.3 million personal and corporate customers, and more than 2,000 large corporate and institutional customers. At the end of last March, its total assets amounted to some $533 billion, of which about $255 billion was related to its loan book. Most of its loans are generated by personal banking, while commercial banking accounts for about 40% of the bank’s loan book, and a smaller part comes from corporate and institutional clients.

Historically, Danske was also exposed to some Baltic countries, but this exposure backfired in 2018, when it was revealed that Danske was used to launder money mainly from Russian customers, showing that the bank’s anti-money laundering (AML) processes had serious shortcomings. This issue was unresolved for several years, but last December the bank was able to settle this matter with Danish and U.S. authorities with a financial cost of nearly $2.3 billion.

Over the past few years, the bank has hired a lot of staff for compliance and legal teams, to strengthen its internal controls, and has exited this geography. Therefore, further issues aren’t likely, even though the reputational damage to Danske is something that is not easy to fix.

Going forward, Danske is not likely to change its business and geographical profile much, as the bank has de-risked its balance sheet and exited non-core businesses in the past few years, being now comfortable with its profile. This means that Danske is likely to grow in markets where it is a challenger bank to larger competitors, namely in Sweden and Norway. In its domestic market, as the market leader the bank enjoys good levels of profitability within a banking market that is relatively concentrated, supporting high levels of profitability in a sustainable way for established players.

Reflecting this profile, Danske’s main financial targets for 2026 aren’t particularly impressive compared to its current position, aiming to achieve a cost-to-income ratio of 45%, a return on equity of 13%, and have a capital ratio of at least 16%.

Financial Overview

Regarding its financial performance, Danske has reported a positive operating performance over the past few years, even though its business was impacted by the pandemic in 2020, which led to some earnings volatility in recent years.

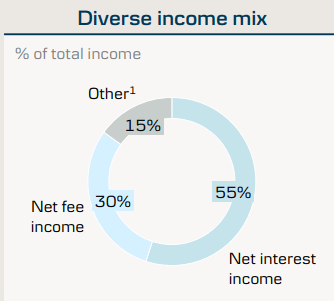

More recently, its business has been boosted by higher interest rates across its geographies, even though Danske is not among the European banks most exposed to rates. Indeed, some 55% of its total revenues are generated by net interest income (NII), while there are other European peers that generate about 75% of revenue from NII, being therefore much more exposed to higher rates.

Income split (Danske)

Nevertheless, Danske’s revenues increased in 2022 mainly due to higher NII and loan volumes, leading to NII growth of 14% YoY, to about $3.7 billion. On the other hand, its fee income declined by 7% YoY, and trading income collapsed by more than 40% due to weak capital markets.

Total revenues amounted to $6 billion, a decline of 3% YoY, despite the positive effect of higher rates, showing that Danske is not really a great rates play in the European banking sector. Moreover, due to the inflationary environment, the bank’s operating cost increased by 3% YoY to $3.9 billion, putting negative pressure on its efficiency level.

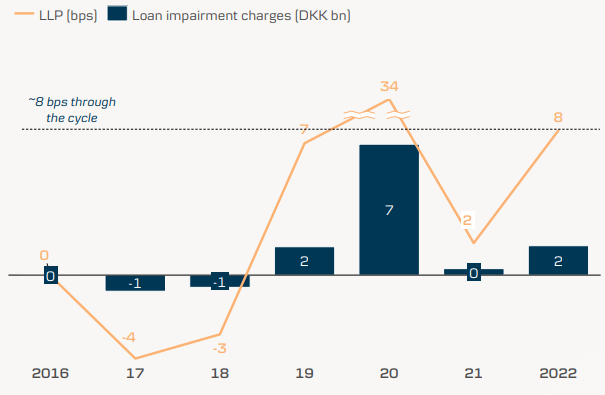

Regarding credit quality, Danske has a very good track record, showing superior levels of asset quality throughout its history. This is a structural factor of Nordic countries, being a very positive backdrop for Nordic banks, of which Danske is obviously no exception. As shown in the next graph, Danske’s provisions for loan losses are usually quite small and way below the average of the European banking sector, being a strong support for high profitability levels over the long term.

Loan loss provisions (Danske)

While in 2022 its loan loss provisions increased compared to the previous year, this increase was only to $294 million, representing a cost of risk ratio of only 8 basis points (bps), in-line with its historical average over the past seven years. Due to higher rates and an economic slowdown, it’s likely that loan loss provisions will increase in the coming quarters, but this should remain at relatively low levels and isn’t expected to be a major headwind to earnings growth in the near future.

Despite the sound operating performance over the past year, Danske’s bottom-line was greatly affected by one-off items, namely further provisions related to the Estonian AML issue and a goodwill impairment related to Danica pensions. This negatively impacted its net profit by more than $2.2 billion, pushing its reported bottom-line to negative territory. Nevertheless, adjusting for these issues, its adjusted net income was close to $1.9 billion, which would nonetheless represent a decline of 20% YoY.

During the first quarter of 2023, Danske has maintained a positive operating momentum, with core banking income (NII plus fees) increasing by 22% YoY to more than $1.6 billion in the quarter. However, this was supported by NII (+43% YoY) while fees declined by 13% YoY, increasing Danske’s reliance on income from rates, even though it only represented close to 60% of total revenues, still a level that is below the average of the European banking sector.

Regarding costs, the bank reported a small decrease (-1% YoY) in operating expenses, leading to a cost-to-income ratio of 46.7% in the quarter, quite close to its 2026 target. This is a very good level of efficiency compared to its peers, being also one of the key strengths of the bank over the long term.

Additionally, credit quality also remained quite good, given that is cost of risk ratio was only 3 bps in the quarter. Despite this, Danske expected its annual cost of risk ratio to be around 14 bps, thus higher loan loss provisions are expected in coming quarters due to a weaker macroeconomic outlook.

As the bank didn’t report any one-off items in the quarter, its net profit recovered rapidly and amounted to more than $750 million in Q1. For the full year, the bank upgraded its previous guidance and now expects to generate a bottom-line between $2.4-$2.7 billion in 2023, which will be the highest level since 2019.

According to analysts’ estimates, its net profit should be closer to the top end of its guidance range, which leads to a return on equity of about 11%, a good level of profitability but still somewhat below its medium-term target of at least 13%.

Regarding its capital position, Danske is among the best capitalized banks in Europe, given that at the end of Q1 its CET1 ratio was above 18%. This is well above both the European banking sector average and its own capital requirements of 13.5%, thus Danske has an excess capital position and does not need to retain much in the way of earnings in the future.

Therefore, its capital position is a strong support for a sustainable shareholder remuneration policy, both through dividends and potential share buybacks. Its dividend policy is to distribute some 40-60% of annual profits to shareholders, which seems quite conservative considering the bank’s superior capital position, allowing for further capital returns through share buybacks in the next few years.

Danske says that its dividend distributions can be above $7 billion from 2023-26 considering this dividend policy, which seems to be sustainable. Moreover, I think the bank can easily perform share buybacks of about $1 billion per year, which would increase its capital returns over the next three years to about $10 billion, or close to half its current market value.

Investors should note that due to its reported losses last year, the bank decided to suspend its dividend payments, but they are likely to be resumed in the short term as they are clearly supported by earnings and Danske does not need to further build up its capital position. The announcement of a sizable dividend could be a positive catalyst for its shares, even though historically Danske has only paid one dividend per year and therefore a dividend announcement is likely to be made at the beginning of 2024.

Current consensus reflects a dividend related to 2023 earnings of $1.88 per share, which at its current share price would lead to a dividend yield of about 7.7%. This means that Danske is likely to become a high-yield stock over the next few months.

Conclusion

Danske is a quality bank in Europe, even though investor sentiment has been quite weak over the past few years due to its AML issue. While this is resolved, Danske continues to trade at a discount to its peers, given that it’s currently trading at only 0.87x book value, while its Nordic peers trade on average at close to 1.20x book value.

This valuation gap seems to be unwarranted as the bank’s fundamentals aren’t much different from other Nordic banks, with the resumption of dividend payments serving as a potential catalyst to close this gap in the near future.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here