It is dangerous to be right in matters on which the established authorities are wrong.”― Voltaire

The NASDAQ shot forward nearly 32% in the first half of the year, after falling by a third in 2022. Almost all of this rise was due to the performance of mega-cap stocks as breadth was very narrow. There are myriad reasons to be pessimistic about the prospects for equities in the second half of 2023. Here are just a few that come immediately to mind.

- The inversion between the 2- and 10-Year treasury yields has reached 1.1%

- The Federal Government is spending $1.5 trillion to $2 trillion annually over what it takes in.

- Rising defaults and falling values in commercial real estate, especially on office buildings in increasingly concerning as I outlined in this recent article.

- There are growing concerns about the largest nuclear reactor in Europe

- The consumer has lost buying power against inflation for 26 straight months now.

- Both U.S. and European manufacturing sectors are in contractionary territory

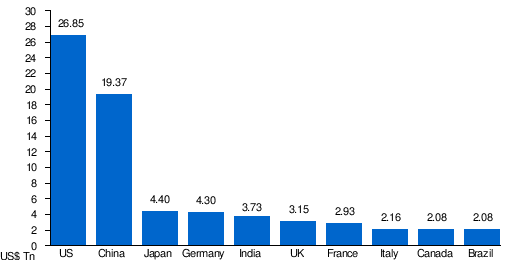

As I noted in my article yesterday, Apple (NASDAQ:AAPL) now has a market cap north of $3 trillion. This is greater than all but 6 countries annual GDP.

2023 GDP Est. (Wikipedia)

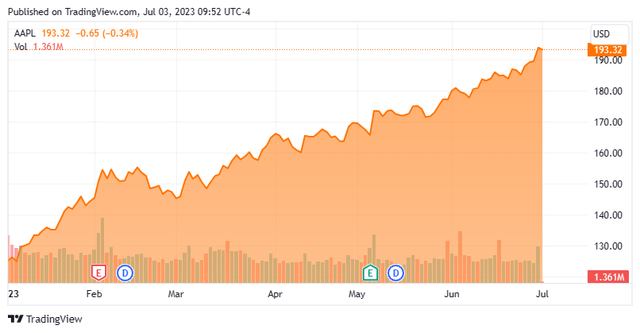

Clearly, this seems out of whack, to say the least. The stock of Apple rose some 55% in the first half of 2023. That might be justifiable if the company’s earnings prospects had improved dramatically since the start of the year. However, that is not the case. The median analyst firm profit projection for both FY2023 and FY2024 has stayed exactly the same over the past three months.

Seeking Alpha

Perhaps if Apple was undervalued to start the year, this huge move would seem more sustainable. However, AAPL began the year trading at approximately 21x forward earnings, slightly above the valuation for the overall S&P 500.

After the big rally in the shares, the stock now trades at approximately 32x forward earnings and nearly 8x forward revenues. Perhaps if interest rates were falling, an expansion in P/E multiple would be understandable. However, the Fed Funds rate now sits at 5.00% to 5.25% and another 25bps hike is highly likely at the Federal Reserve meeting later this month.

Typically, growth stocks usually underperform in a rising rate environment as they did in 2022. For some reason, the opposite has happened in 2023 year to date. Maybe the rise in Apple shares would be more plausible if the company was delivering 15% to 20% annual earnings and revenue growth or even 10% for that matter. However, both earnings and revenues are projected to fall slightly in FY2023 compared to FY2022.

Perhaps if AAPL was significantly below analyst price targets, the move in the shares would make more sense. However, since Apple reported first quarter results on May 4th, 16 analyst firms including JPMorgan and Credit Suisse have reissued Buy/Outperform ratings on the stock. Price targets proffered have range from $180 to $240 a share, with seven of these being at or below the current trading levels of the stock. In addition, five analyst firms including Barclays have maintained Hold ratings on the shares mostly due to valuation concerns. Price targets among this group of analyst firms range from $149 to $190 a share. Numerous insiders also dumped just over $50 million worth of shares collectively in April of this year when the stock was trading in the mid $160s, almost 20% below the current trading price of the stock.

Clearly, the stock is priced for perfection at current trading levels and could pull back significantly if we get a break in the overall market, which seems more than likely at some point in the months ahead. In addition, Apple would be very vulnerable if tensions between Taiwan and China escalate in the months ahead given its large presence in that region of the globe. As the famed economist Herbert Stein quipped in the 80s ‘“If a thing can’t go on forever, it will eventually stop.” I think we are close to that inflection point around the shares in this tech titan.

Therefore, I have executed some bear put spreads on Apple. This strategy involves buying a put and simultaneously selling a put at a strike under the first put on the same calendar month. Using this strategy, an investor is looking to capture a profit if the stock in question declines within the option duration enough to make the trade a winner.

I know that makes me a heretic in this market as less than one percent of the outstanding float in Apple stock is currently held short despite the shares extended valuation. That is significantly less than the roughly 3.5% of shares outstanding held short in Tesla Motors (TSLA), another mega-cap that has driven most of the market gains so far in 2023.

The short percentages should be much higher given the current valuations on these names. However, given anyone short these mega-cap names has been run over with a steam roller in the first half of 2023, I understand the reluctance to go short. That is why I prefer the bull put spread strategy highlighted below. If I am right and the market has a ‘hiccup’ over the next three months, I am likely to make $20 on a $2.50 bet and that seems a solid asymmetrical trade in this market.

Option Strategy:

Using the October $180/$160 strike pair, execute bear put spreads for a net debit of $2.40 to $2.50 a share. If we do get a significant decline in the overall markets and Apple pulls back 17%, this trade will provide an eight-to-one return. An approximate eight percent decline puts this trade in break-even status. In the case AAPL moves higher, it is likely the bull market is continuing, and the other parts of your portfolio are rising. As such, this trade acts like portfolio insurance to some extent.

It has been said that heresy is the revenge of a forgotten truth.”― R.A. Lafferty

Read the full article here