Wealth is a person’s ability to survive a certain number of days forward.” – R. Buckminster Fuller

Today, we take a deeper look at a developmental concern that is deep in Busted IPO territory thanks to some clinical setbacks. However, the company still is developing several early-stage candidates and the stock trades not that far above the net cash on its balance sheet. Trial readouts are on the horizon and the stock has seen some recent insider buying. An analysis follows below.

Seeking Alpha

Company Overview:

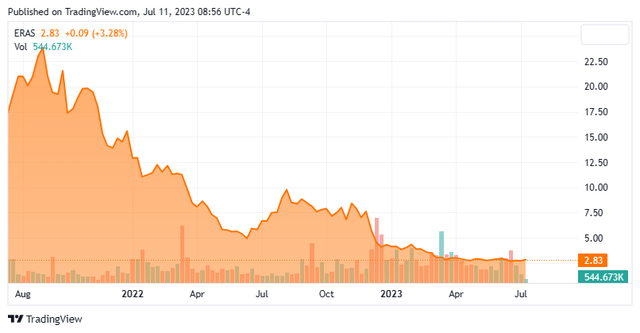

Erasca, Inc. (NASDAQ:ERAS) is a San Diego based clinical-stage biopharmaceutical concern focused on the development of therapies that treat cancers affected by the RAS oncogene/mitogen activated protein kinase (RAS/MAPK) pathway. The company has four clinical assets pursuing six indications, of which one is scheduled to be evaluated in a Phase 3 study in 1H24. Erasca, whose name is a play on the term ‘erase cancer‘, was formed in 2018 and went public in July 2021, raising net proceeds of $317.0 million at $16 a share. The stock trades just under three bucks a share, translating to an approximate market cap of $425 million.

RAS/MAPK Pathway

The RAS oncogene controls systemic body fluid circulation, but it is also present in many tumor microenvironments. In fact, RAS is the most regularly mutated oncogene, while the MAPK pathway is one of the most frequently altered signaling corridors in cancer. Together the RAS/MAPK pathway accounts for ~5.5 million new cancer diagnoses globally each year. In healthy patients, RAS acts like a light switch, toggling between “ON” and “OFF”. When ON, a RAS isoform protein sends signals that tell a cell to grow and divide. RAS mutated proteins rarely switch OFF, leading to uncontrolled cell growth, which is engendered through the MAPK pathway that consists of a series of protein kinases (in order: RAF (consisting of ARAF, BRAF, and CRAF proteins), MEK, ERK, and MYC). RAS is further supported by other key signaling nodes, such as EGFR/FLT3, SOS1, and SHP2. Once considered an “undruggable” target, therapies attempting to keep RAS permanently locked in the OFF position have been approved, beginning with Amgen’s (AMGN) KRAS G12C [OFF] inhibitor Lumakras (sotorasib) in 2021.

Erasca’s aim is to develop therapies that comprehensively shut down RAS/MAPK through three approaches: 1. Targeting key upstream and downstream signaling nodes in the pathway; 2. Targeting RAS directly; and 3. Targeting escape routes that emerge in response to treatment.

Pipeline

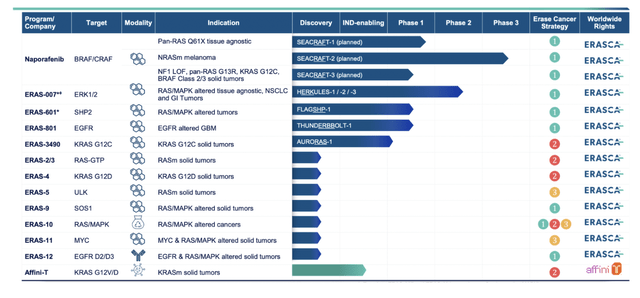

That said, the company’s current clinical assets all target proteins upstream or downstream from RAS.

Company Website

Naporafenib. After a recent pruning of its portfolio – more on that development below – Erasca’s lead candidate is now naporafenib, an orally administered pan-RAF inhibitor that will be undergoing assessment in patients with NRAS mutant (NRASm) melanoma, RAS Q61X tissue agnostic solid tumors, and other RAS/MAPK pathway-driven tumors. Although it has been studied in over 500 patients as both a monotherapy and in combination across eight clinical trials, the upcoming studies will be the first under the company’s sponsorship. Erasca in-licensed naporafenib from Novartis (NVS) in December 2022 for a total upfront consideration of $100 million, consisting of $20 million in cash and $80 million in ERAS shares priced at $6.50. Additionally, Erasca is potentially obligated on up to $280 million in sales and regulatory milestones, as well as low single-digit royalties.

Its most advanced indication is NRASm melanoma, for which it will be studied in combination with (ironically) Novartis’ MEK1 inhibitor Mekinist (trametinib) in a potentially pivotal Phase 3 trial (SEACRAFT-2) that is expected to initiate in 1H24. Naporafenib will first reenter the clinic in 2H23, when a Phase 1b study (SEACRAFT-1) will examine it in combo with Mekinist in patients with RAS Q61X solid tumors.

As for its efficacy against NRASm melanoma in previous studies, a naporafenib 200mg twice daily plus trametinib 1 mg once daily combination produced an objective response rate (ORR) of 33.3% (13/39), whereas naporafenib 400mg twice daily plus trametinib 0.5mg once daily generated an ORR of 21.9% (7/32) across two studies (Phase 1b and Phase 2) – suggesting but not proving that trametinib was the more efficacious contributor. The combo’s safety profile was not exactly glowing – with all 30 patients experiencing a treatment-related adverse event in the Phase 1b study – but not disastrous as skin rash was the most common issue.

That said, the combo has a low bar to hurdle in the post-frontline setting. Globally, ~69,000 new cases of NRASm melanoma are diagnosed annually, which are initially treated with PD-1 immuno-oncology [IO] therapy. Those unresponsive to IO treatment received chemotherapy, which has demonstrated a ~7% ORR in relevant studies. MEK inhibitor binimetinib produced an ORR of 15%, median progression free survival of 2.8 months and median overall survival of 11.0 months; thus, the inspiration for the trametinib-naporafenib combo. Erasca believes naporafenib’s total addressable market across all relevant tumor types is ~500,000 in the U.S. and Europe – ~54,000 for the NRASm melanoma indication.

ERAS-801. The company’s other clinical programs are in early-stage development, including ERAS-801. It is a CNS-penetrant epidermal growth factor receptor (EGFR) inhibitor being assessed in a Phase 1 trial (THUNDERBOLT-1) treating patients with recurrent glioblastoma multiforme (rGBM). GBM is a cancer of the brain and spinal cord that is diagnosed in 125,000 individuals across the globe annually. It is currently treated with surgery, followed by radiation and chemo. If GBM recurs, treatment options are limited. Erasca puts that population at ~37,000 in the U.S. and Europe. ERAS-801 has received Fast Track designation from the FDA as well as Orphan Drug designation late last month. Monotherapy dose escalation data from THUNDERBOLT-1 are anticipated in 2H23.

ERAS-601. Also expected to produce early stage data is ERAS-601, an oral inhibitor of SHP2, a convergent node for upstream receptor tyrosine kinase signaling whose activation drives tumor cell proliferation. ERAS-601-chemotherapy combinations are undergoing assessment in a Phase 1b study (FLAGSHIP-1) treating patients with solid tumors. Dose expansion data from that study are anticipated in 1H24.

ERAS-007. Naporafenib has moved to lead clinical program due to the de-prioritization of ERAS-007, an oral ERK 1/2 inhibitor that was assessed against solid tumors as a monotherapy and in combination across a series of trials dubbed HERKULES. Results, for the most part, were underwhelming. As such, it was de-emphasized, along with another clinical program (ERAS-3490) and three discovery efforts announced in a June 5, 2023 press release.

ERAS-007 is not completely dead, as Erasca elected to further evaluate it in combination with Pfizer’s Braftovi (encorafenib) and Eli Lilly’s EGFR inhibitor Erbitux (cetuximab) (collectively known as EC) for the treatment of BRAF mutated colorectal cancer in patients who are EC naïve. This decision was based on two confirmed partial responses (PRs), one unconfirmed PR, and one disease control out of six patients who received ERAS-007 100mg twice daily. Expansion data from the Phase 1b combo dose is expected in either 2H23 or 1H24.

Balance Sheet & Analyst Commentary:

To finance its now slightly abridged research and clinical endeavors, the company held cash and marketable securities of $389.7 million as of March 31st, 2023, providing it a cash runway to YE25. Erasca last tapped the capital markets in December 2022, executing a secondary offering that raised net proceeds of $94.9 million at $6.50 per share concurrent to its deal for naporafenib.

Somewhat surprising, the small Street coverage is unanimously bullish on the company’s prospects, featuring two buy and two outperform ratings and price objectives ranging from $8 to $15, representing multi-bagger upside from current trading levels.

Furthermore, Chairman & CEO Jonathan Lim is bullish on his company’s outlook, purchasing 100,000 shares of ERAS at $2.75 on June 8, 2023. Between his family trust and his managing partner position of City Hill, LLC, he controls 20% of the ownership interest.

Verdict:

Erasca pursued too many indications, boasting of as many as 13 discovery or clinical programs at YE22 with only ERAS-007 advancing into Phase 2 studies under its sponsorship. With the slow pace and high cost of clinical oncology trials and nothing eye-popping in terms of efficacy data from its early-stage trials, the company’s stock languished in the single digits. Management – likely sensing that ERAS-007 was not going to make it to the finish line – was thus compelled to make a splash in the form of naporafenib, bringing Erasca (theoretically) closer to commercialization. However, with that potentially pivotal trial not initiating until 1H24, it will be a long time before the market will have any actionable data.

Admittedly, Erasca will have early-stage data from ERAS-801 (2H23), ERAS-007 (2H23 or 1H24), and ERAS-601 (1H24) – and those catalysts may turn around the dour sentiment on the stock (Street analysts and insider purchase notwithstanding). The bet here is that they won’t. The other issue is that no fewer than 17 other biopharmaceutical concerns are developing therapies that target the RAS/MAPK pathway. Naporafenib may be the most clinically advanced pan-RAF inhibitor, but there are seven in the clinic undergoing evaluation in Phase 1 or 2 studies. Also, there are seven other SHP2 inhibitors in the clinic to challenge ERAS-601.

With another capital raise likely necessary before any actionable data from SEACRAFT-2, the recommendation is to avoid even though it trades at only ~$35 million premium to cash.

Finance is the art of passing money from hand to hand until it finally disappears.” – Robert W. Sarnoff

Read the full article here