Iran still has an outsized ability to rattle global energy markets.

Markets will not reopen until Monday but a $10 rise in the price of a barrel of oil since the start of the year is a reminder of how seriously traders take any threat to the country, even though years of US sanctions mean Iran’s oil exports no longer make up a major share of the world’s supply.

The main source of market concern is Iran’s influence over shipping in the Strait of Hormuz, through which the oil and gas of its Gulf neighbours has to pass, and its sponsorship of militias throughout the region that could launch attacks on energy infrastructure.

“It is very tricky,” said one senior energy trader, as he considered how to navigate the fallout from air strikes on Iran by Israel and the US on Saturday. “Targeted attacks could result in chaos and there is the potential for further [price] spikes because there will be a lot of uncertainty.”

Last year, each jump in the oil price during the brief war between Iran, Israel and the US was followed by a sell-off, as traders bet that there was little chance of regime change in Tehran, or broader instability.

But that calculus has shifted, with growing fears that the US will seek the overthrow of the Iranian regime, a scenario that raises the risk of conflict spilling across the Middle East, and significant disruption to energy flows.

How important is Iran to global energy supplies?

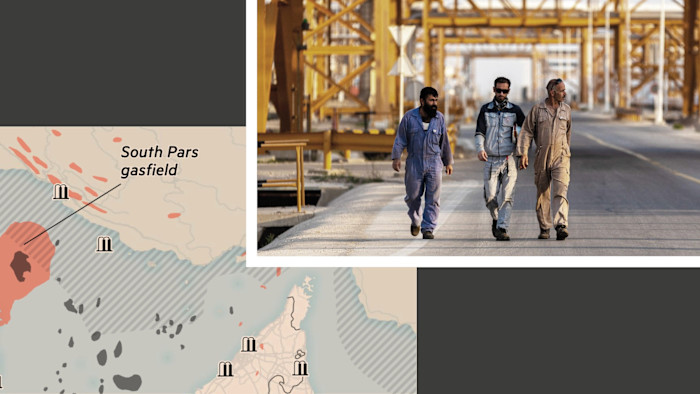

Iran has the world’s fourth-largest proven reserves of crude oil, but years of sanctions and under-investment have hobbled its exports.

The country pumped 3.45mn barrels a day (b/d) of oil in January, according to the International Energy Agency, less than 3 per cent of global supply.

Almost all of its exports go to China, mainly to independent refiners in Shandong province that are willing to buy sanctioned oil at a steep discount. Iranian crude accounted for roughly 13 per cent of China’s seaborne oil imports last year, according to Kpler, an energy data company.

During last year’s conflict, Israel attacked Iran’s fuel depots but steered away from other energy infrastructure. Because of its shallow coastline, Tehran has an acute vulnerability: almost all of its crude flows from a single export terminal, Kharg Island, 15 miles offshore in deeper waters. In recent days, the terminal has stepped up its exports and drained its inventories of crude.

But the loss of Iranian barrels would not, by itself, upend the market. With global supply set to exceed demand in the first half of this year, the impact is expected to be limited.

“In the current context, the markets could absorb it if the oil disappeared tomorrow,” said Richard Nephew, a former US deputy special envoy for Iran, who is now at Columbia University’s Center on Global Energy Policy.

Tehran would not want to stop the flow of crude except in the most dire circumstances, said Dan Marks, a research fellow in energy security at the Royal United Services Institute.

“The regime is hanging by a thread and if you added a cessation of oil exports, it would be a huge blow.”

Iran also exports natural gas to neighbouring countries, including Turkey and Iraq, but these flows are frequently disrupted. Supplies to Iraq were recently halted over what Tehran described as technical problems, while gas trade with Turkmenistan has been sporadic after disputes over unpaid bills.

How could Iran disrupt global energy flows?

Around 21mn barrels of oil from Iran, Iraq, Kuwait, Saudi Arabia and the United Arab Emirates pass each day through the Strait of Hormuz. Iran has repeatedly threatened to close the chokepoint and laid mines across the waterway during the 1980s.

Helima Croft, an analyst at RBC Capital Markets, said if Tehran felt that the US was serious about regime change, the response may be dramatic. “We think there is a significant risk that round two between Tehran and Washington will be wider and more disruptive than the 12-day war last June,” she said.

She added that on a recent visit to the Middle East “multiple well-placed observers warned that Iran would likely look to target energy facilities and other key economic assets to force Washington to stand down”.

Nephew added: “Their thinking would be: ‘If we are not allowed to have an energy system, neither are you.’”

However, Marks said that Tehran had few good options. “If the economy was healthy and the regime was strong, it could shut down exports or close the Strait of Hormuz. You can just say you have laid mines, or fire a few missiles, and then the shipping will stop. No one wants to have their crew killed,” he said.

“But what is the end game? The world could withstand a crisis for a few weeks, but there will be more military action, their neighbours would be unhappy, currency would spike and you risk hyperinflation.”

Tehran can also call on a network of militias across the Middle East to disrupt oil production, exports or shipping.

What will happen to oil prices?

Traders remain relaxed about the long-term impact of confrontation, pointing to ample alternative supplies and uncertainty over the scale and duration of any conflict.

Iranian output could be offset by higher production from Saudi Arabia or by drawing on storage in the event of a brief disruption, said Giovanni Staunovo of UBS.

Members of Opec, the oil producer group, are scheduled to meet on Sunday to discuss their output for April.

Analysts expect Opec to increase production by 137,000 b/d, but one person close to the situation suggested Opec could increase by three or four times that in order to calm markets.

Meanwhile, one senior trader said the industry had got used to rearranging energy flows and had prepared for disruption around the Gulf.

“You build as much flexibility in there, and know you might have to change freight journeys,” they said, adding that the industry had successfully dealt with the shocks of the Covid-19 pandemic and from Russia’s full-scale invasion of Ukraine.

Brent crude rose as much as 3 per cent on Friday to touch a seven-month high of $73 a barrel, and has risen nearly 12 per cent over the past month as expectations of conflict rose.

David Fyfe, chief economist at Argus, highlighted the knock-on effects for Chinese refiners, which have benefited from cheap crude from Russia, Venezuela and Iran. Any supply shortfall would push them towards more expensive Middle Eastern grades, squeezing margins.

That pressure could become a political bargaining chip between Washington and Beijing. “Trump is very much aiming his crossbow at Beijing,” Fyfe said. “The big question is whether he follows through.”

How important is oil to Iran’s economy?

Iran’s leaders have long insisted that the country must wean itself off oil. Supreme Leader Ayatollah Ali Khamenei has repeatedly criticised the sector’s dilapidated state and warned that dependence on oil left Iran vulnerable to external pressure.

“Running our country on oil revenue leaves us at the mercy of major policymakers in the world,” he said in 2014, urging diversification to “become immune to the influence of powers”.

But the country remained “overwhelmingly reliant” on oil revenues, said Nephew. “They have some minor stuff here and there, but this is it, the major export industry after all these years. The lack of investment and sanctions have made it impossible to develop anything else.”

Read the full article here