As part of our ongoing series of articles on bank stability, and at the request of many of our clients, we have publicly addressed the major risks we foresee for bank stability in the coming years. We want to now address issues being discussed about brokerage houses.

But before we begin, I want to take this opportunity to remind you that we have reviewed many larger banks in our public articles. But I must warn you: The substance of that analysis is not looking too good for the future of the larger banks in the United States, details for which you can read here.

Moreover, if you believe that the banking issues have been addressed, I’m sorry to inform you that you likely only saw the tip of the iceberg. We were able to identify the exact reasons in our public article which caused SVB (OTCPK:SIVBQ) to fail well before anyone even considered these issues. And I can assure you that they have not been resolved. It’s now only a matter of time.

Today, we will be discussing Schwab.

There have been several bearish articles on Schwab (SCHW) lately. For our clients, we published detailed reports on almost all large brokerages that disclose their financial data publicly, and Schwab was among them. As such, we would like to address the bearish thesis on Schwab.

Most importantly, please recognize that we’re going to discuss the long-term financial stability of the company rather than provide a short-term view on the stock. Our focus always is on the stability of the financial institution rather than opining upon the stock valuation.

The key argument of those who are bearish on SCHW is that Charles Schwab Bank (CSB), a banking subsidiary of the Charles Schwab Corporation, has seen massive deposit outflow lately. Some compare this situation to the infamous SVB case and expect that SCHW is likely to face major issues soon.

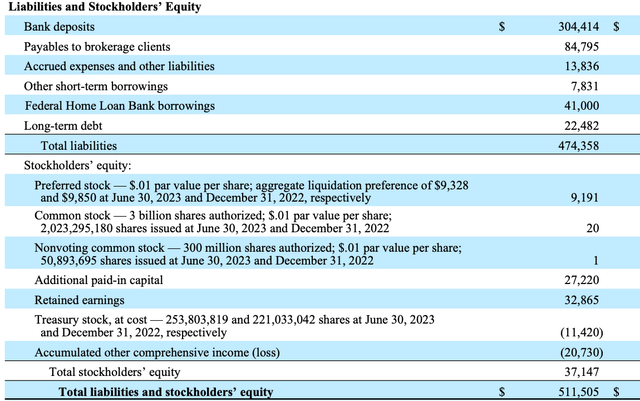

Without a doubt, bank deposits are a key source of funding for both the bank and the company, as they account for 60% of the company’s total liabilities and equity.

Company Data

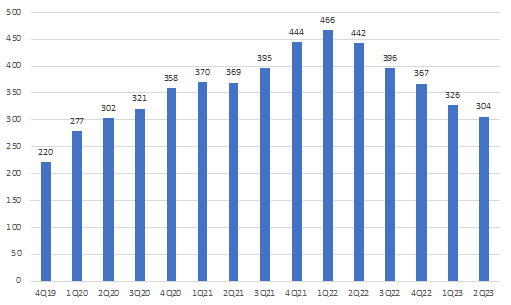

The chart below shows the dynamics of the company’s bank deposits since 4Q19.

SCHW: Bank deposits, $B

Company Data

Note: Including time certificates of deposit that consist of brokered CDs

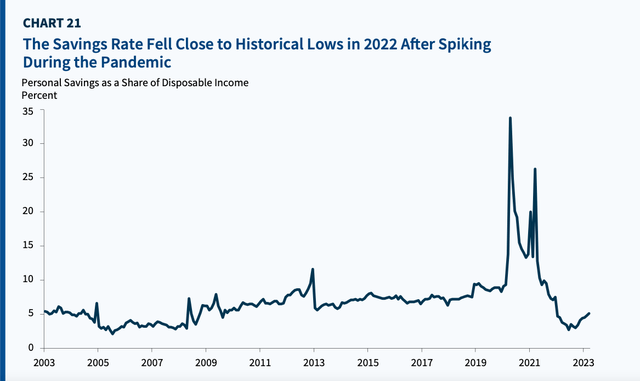

As the chart above shows, SCHW’s bank deposits began to increase significantly in 1Q20, when the pandemic started. Various monetary stimulus measures and a sharp drop in consumer spending led to a strong increase in the savings rate. The chart below demonstrates this.

FDIC

A large share of this retail savings was transferred to the stock market, and brokerages were beneficiaries of this trend. Unsurprisingly, SCHW’s bank deposits grew by 63% YoY in 4Q20.

When the Fed started its tightening cycle in early 2022, most U.S. banks had to increase their deposit rates. The rate on SCHW’s bank deposits remained near zero at the time, and the so-called “yield chasers” began to withdraw their deposits from SCHW. The chart with the deposits’ dynamics clearly illustrated that, as they peaked in 1Q22. Importantly, most clients kept their money at SCHW, as they just did cash reallocations within the company. In other words, they used their available cash for investing, mostly for purchasing SCHW’s own money market funds. As a result, the company’s bank deposits declined, although its total AUM grew.

The SVB failure put additional pressure on the company’s deposit base, but, in our view, the key reason is yield chasing. This is clearly not a bank run but rather an allocation to higher-yielding products.

While the headline deposit dynamics do look concerning, as SCHW’s deposits have fallen by 35% since they peaked in 1Q22, a deeper look suggests that the situation is much better than it initially appeared. SCHW’s financial position looks different compared to the SVB case.

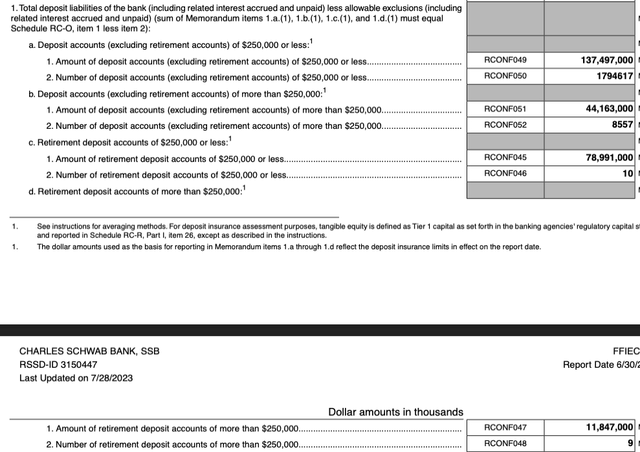

First, SCHW has a high deposit granularity, and its average client deposit balance is around $150K. By comparison, SVB’s average client deposit balance was more than $1.1MM. Furthermore, as can be seen, the majority of SCHW’s deposits are less than $250K. Banks with higher deposit granularity are much more resilient to liquidity issues.

FFIEC

Second, SCHW, as a whole company, continues to enjoy stable client inflows. The table below has the line “core net new assets,” which is one of the key performance metrics for SCHW. As we can see, SCHW saw strong inflows in 11 out of 12 previous months, and there was a very mild outflow only in April 2023. We also note that SCHW’s AUM surpassed the $8T mark in June.

Company Data

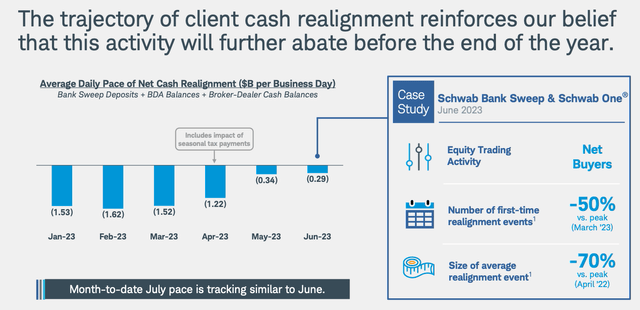

Third, the latest data suggests that deposit outflows have slowed recently. Moreover, SCHW expects deposit growth to resume in 4Q. Here are two quotes from SCHW’s latest earnings call:

“Now we shared in our last SMART report the dramatic reduction in the pace of client cash allocation activity from April to May. And in June, we saw a further slowing in the pace of deposit flows. And the reduction would have been even more significant or not for a large reversal in client equity allocations from sales in May to net purchases in June. Now that broader trend is encouraging, but not surprising, and it’s reinforced by specific data points we see when we look under the hood. We’re seeing fewer and fewer individuals making their initial purchase of an investment cash solution, a purchase money fund or CD or treasury security. And since the clients with larger cash balances moved first, again, not surprisingly, the average size of those initial purchases has also come down.”

“So we’d expect we’ll see return of deposit growth I would say, ahead of that typical seasonal buildup that you get in later November and into December.”

And here’s a chart that shows the trajectory of client cash realignment:

Company Data

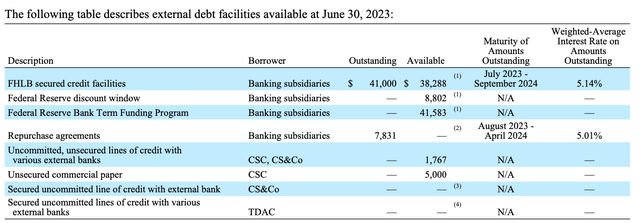

Those who are bearish on SCHW often say that as a result of these deposit outflows, the company had to raise expensive wholesale funding and issued brokered CDs. As a result, according to the bearish thesis, this is very likely to lead to a significant NIM contraction. Without a doubt, we agree that more expensive funding will put pressure on the company’s NIM. The table below shows that the weighted-average rate on FHLB borrowings is much higher compared to what SCHW pays on deposits.

However, two things are worth mentioning here. First, SCHW attracted around 50% of the available funding, so the company still has quite a large liquidity cushion. Second, even with the current trajectory of client cash realignment, this expensive funding will be repaid by the end of 2024 or probably earlier if deposits resume growing.

Company Data

Finally, we would like to note that Schwab Bank has quite a unique position. If a sharp sell-off in the stock market happens, then clients will very likely sell their positions and raise cash, which will likely result in a strong increase in SCHW’s bank deposits.

Bottom Line

We wrote a detailed report on Schwab, as well as on other large brokerages, and assessed the company using 20 different metrics. We do think that the recent deposit outflows are not a near-term risk for the company and do not agree with the bearish thesis. Overall, we view Schwab as a good brokerage and a decent bank. From a relative standpoint, it’s one of the better brokerages.

With that being said, there’s a reason why Schwab Bank did not make it into our Top-15 banks. The company has quite a large share of long-duration securities on the balance sheet. If you follow our banking articles, you probably noticed that almost all large U.S. banks have this issue, and SCHW looks better than the majority of them in that department.

But it’s unlikely that SCHW will face major liquidity issues with this level of policy rate. However, if rates go up to the double-digit range, there will likely be new massive deposit outflows, and SCHW will have to sell its long-duration securities at a huge loss. By contrast, the Top-15 banks that we have recommended to our clients are much more resilient to this issue. As such, if you keep all your savings at Schwab, it would be good to do some diversification and look at safer banks.

At the end of the day, we’re speaking of protecting your hard-earned money. Therefore, it behooves you to engage in due diligence regarding the banks which currently house your money.

You have a responsibility to yourself and your family to make sure your money resides in only the safest of institutions. And if you’re relying on the FDIC, I suggest you read our prior articles which outline why such reliance will not be as prudent as you may believe in the coming years.

It’s time for you to do a deep dive on the banks that house your hard-earned money in order to determine whether your bank is truly solid or not. Details are in our due diligence methodology, outlined here.

Housekeeping matters

This article, as well as Saferbankingresearch.com, was a combination of efforts between Avi Gilburt and Renaissance Research, which has been covering U.S., European, LatAm, and CEEMEA banking stocks for more than 15 years.

If you would like notifications as to when my new articles are published, please hit the button at the bottom of the page to “Follow” me.

Also, for those that are questioning why all comments (including mine) go through moderation, you can read here: Haters Are Gonna Hate – Until They Learn.

Lastly, I have asked the editors to close the comments section, as I will be out in religious observance of the holiday of Sukkot. The comments section will re-open when I return next week.

Read the full article here