Life Time Group Holdings, Inc. (NYSE:LTH) operates approximately 160 fitness centers across the United States serving more than 800k members. The company has found success through a wellness lifestyle approach incorporating premium amenities at resort-like destinations. The attraction here is an impressive growth outlook with firming profitability in recent quarters.

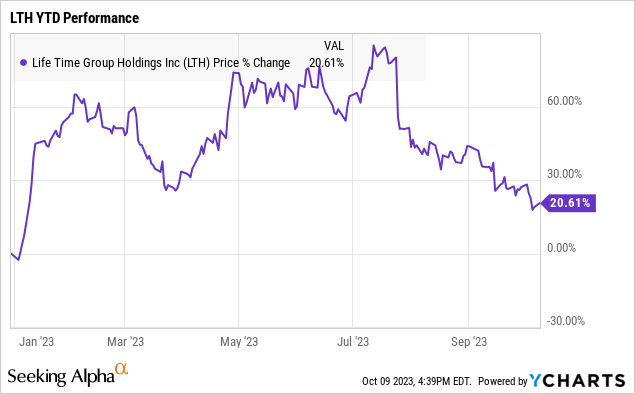

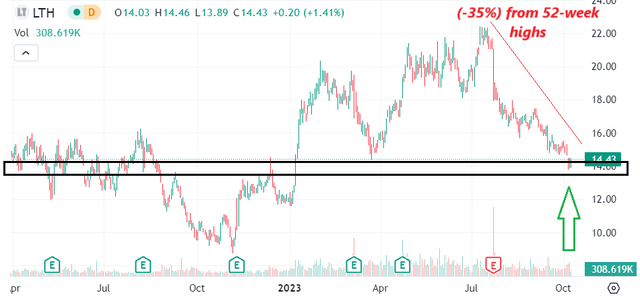

We like the stock ahead of the company’s upcoming Q3 earnings report set to be released later this month. The setup here is that LTH has been under pressure, down more than 30% from its 52-week high. We believe the current level offers an attractive entry point for a quality stock that is well-positioned to rebound with several tailwinds into 2024.

LTH Financials Recap

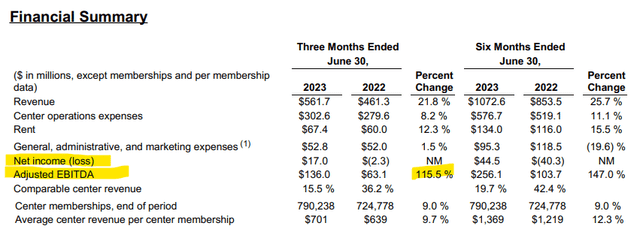

Life Time last reported its Q2 results back in July with the headline EPS of $0.19, beating expectations by $0.09, and reversing a loss of -$0.04 in the period last year. Revenue of $562 million was up by 22% year-over-year and also exceeded expectations.

The momentum has been driven by the combination of continued membership growth, which climbed by 9% from the period last year, with the average revenue per center per membership up a stronger 12.3% year-to-date.

Favorably, an effort at cost controls including general, administrative, and marketing expenses resulted in a small increase of only 1.5% y/y, and this added to earnings. Adjusted EBITDA reached $136 million in the quarter, more than double the $63 million in Q2 2022.

source: company IR

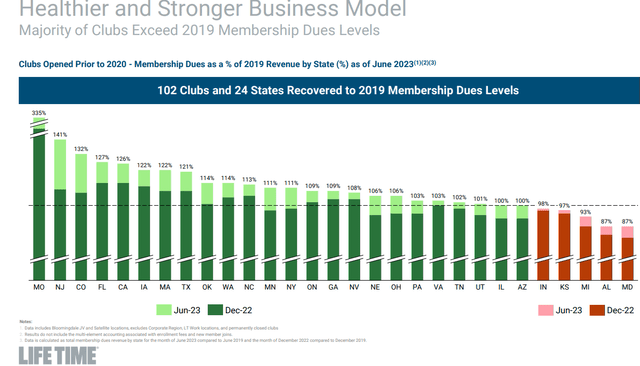

The story here in 2023 has been improving operating metrics, even exceeding pre-pandemic benchmarks across various performance indicators. Notably, membership dues across the entire network are now at 114% of 2019 levels with several states far exceeding that threshold.

Management highlights how Life Time Fitness members are on average using the facilities more often, and also spending more on additional services as a good indication of brand momentum and the health of the business model.

source: company IR

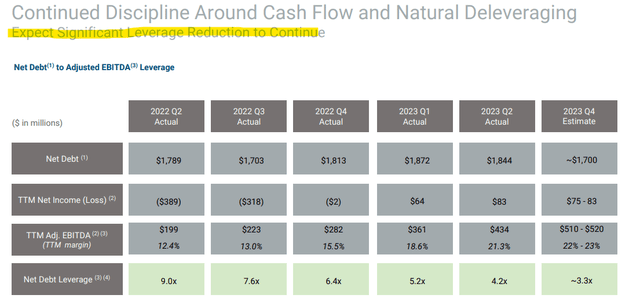

Another important theme has been the ongoing balance sheet deleveraging based on the stronger cash flow. Compared to the pandemic where the company was forced to take on significant debt, where the leverage ratio reached as high as 9x in 2022, that level has since declined to 4.2x in the last quarter.

While still elevated, management sees that level narrowing to 3.3x by the end of this year considering guidance for full-year adjusted EBITDA between $510 and $520 million against $1.7 billion in debt. Life Time Group is also targeting full-year revenue of around $2.25 billion, representing a 23% increase from 2022. Notably, both of those estimates were revised higher compared to the Q1 forecast.

source: company IR

What’s Next For Life Time Group?

What we like about Life Time is the sense that the company is finally hitting its stride with a refined business model that is proving to be highly successful. The company has this leadership position in the segment of “premium” fitness clubs that benefit from the secular trend of growing interest in wellness and healthy lifestyles.

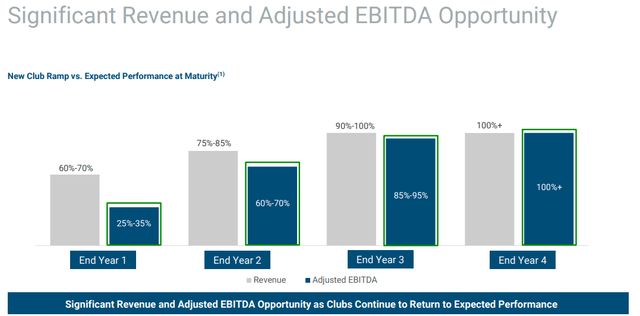

Maybe the most encouraging chart when looking at the stock is the path where new clubs ramp up in profitability over time. In year one, a new Life Time Fitness location is expected to generate just 60%-70% of its expected revenue performance at maturity and 25-35% of potential EBITDA.

Those levels start to approach 100% by year 3. This is important as it highlights many of the recent launches and expansion efforts are still set to contribute positively to the bottom line.

source: company IR

Life Time notes that it has more than 80 new clubs planned to open at various stages of development over the next few years. That pace ties into the consensus estimates for continued growth and stronger earnings going forward.

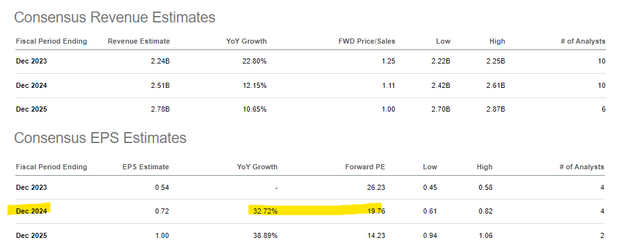

Compared to the 2023 EPS estimates of $0.54, LTH is forecast to reach EPS of $0.72 in 2024, representing a 33% increase. The outlook here is for double-digit top-line growth over the next few years while earnings accelerate higher.

Seeking Alpha

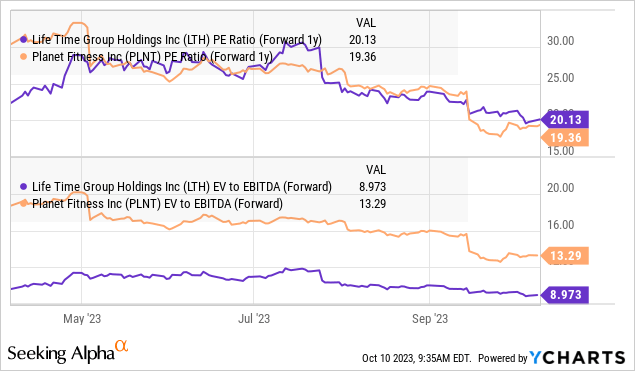

In terms of valuation, we believe that 20x 1-year forward P/E based on the 2024 consensus EPS is attractive. Here we can bring up Planet Fitness, Inc. (PLNT) for comparison purposes as the largest publicly traded “fitness centers” stock. LTH currently trades at a discount in terms of its EV to forward EBITDA multiple of 9x compared to 13x for PLNT.

On this point, each company has several differences. First, Planet Fitness focuses more on the budget side of the spectrum with its no-frills low pricing. In contrast, Life Time features facilities with value-added amenities like tennis courts, pickleball, swimming pools, cafes, and personal training in an attempt to build more of a community aspect and command higher pricing.

The argument we make is that LTH deserves a valuation premium given its market positioning as representing a competitive advantage. We’d argue that Life Time has a stronger long-term growth outlook from its smaller base.

Final Thoughts

We rate LTH as a buy with a price target of $20.00 for the year ahead, representing a 27.5x multiple on the current consensus 2024 EPS. The way we see it playing out is that a strong string of results over the next few quarters should help rebuild the market confidence that the company remains on track with its expansion efforts and trend of climbing profitability.

In our view, the recent selloff in the stock is more related to concerns regarding the strength of the economy and potential slowdown in consumer spending and is not reflective of the company’s long-term growth potential. The effort at balance sheet deleveraging and higher margins can support a higher valuation premium, in our opinion.

In terms of risk, a scenario where a deeper economic slowdown emerges would undermine the growth outlook. Weaker-than-expected results would open the door for a deeper selloff and force a reassessment of the outlook.

Seeking Alpha

Read the full article here