Lifecore Biomedical (NASDAQ:LFCR) is a $288m market cap provider of contract development and manufacturing (CDMO) services to pharmaceutical companies. Several months ago, LFCR found itself in a difficult situation due to concurrent delays in product shipments and customer onboarding which forced the company into breaching its debt covenant and a technical default. This default was only technical in nature (not a result of any underlying business problems) and seemed likely to get resolved soon. However, the market took it very seriously and kept the share price depressed even despite several highly positive LFCR business developments taking place in the meantime. This created a very interesting setup with three short-term catalysts and huge upside potential. Here’s how I described it to my Special Situation Investing subscribers last week:

This is a high-uncertainty/high-reward setup where the ongoing strategic review might result in the sale of the company at a multiple of today’s price. However, the company is in technical default due to a covenant breach, is non-current on its financials, and has not provided any additional disclosures over the last two months. Investors are left in the dark with no updates on the debt forbearance or the sale process. Hence, LFCR is a bit of a black box today, which is why the opportunity exists. The key known fact is that the company owns a fast-growing and high-quality pharma CDMO business that is apparently coveted by market participants. In a sale scenario, this business could fetch a 15x-20x EBITDA multiple resulting in an equity value of $8-$20/share, a significant premium to today’s $5/share market price. 3 pending catalysts are likely to drive LFCR shares upwards – the announcement of a forbearance agreement with the lenders, getting current on the financials, or potentially full company sale.

The turnaround was quick and the first catalyst has already worked out this week. Yesterday, the company announced a new $150m financing and sale-leaseback agreement with its major customer Alcon as well as a repayment of the existing $99m term loan. This has completely eliminated the technical default and going concern issues causing LFCR’s share price to jump by 50%.

Although the multi-bagger thesis has partially played out already, there seems to be a substantial (50%-80%) upside left from the two remaining short-term catalysts – the company sale and LFCR getting current on its financials.

The company is currently running a strategic review and recent industry transactions suggest that LFCR is worth a significantly higher price in a sale scenario. LFCR is a CDMO that specializes in the fast-growing and high-quality aseptic fill finish sector. Aseptic fill finish involves the sterile filing of pharmaceutical products, such as medications and vaccines, into containers such as syringes, vials, and ampoules. Aseptic fill finish has been among the fastest-growing segments in the CDMO space.

LFCR Investor Presentation, October 2022

LFCR currently trades at 11.8x adjusted EBITDA and 3.0x sales. This multiple is significantly below the average 17x TTM EBITDA multiple for CDMO take-outs from 2017 through early 2023. Several industry transactions are provided below:

- Thermo Fisher buying Patheon for $7.2bn or 17x EBITDA.

- Baxter divesting its CDMO business for $4.3bn or 6.6x revenues.

- GHO Capital acquiring Alcami at a rumored 20x EBITDA.

- Cambrex scooping up Avista for $252m or 3.9x revenues.

- Lonza acquiring Capsugel for $5.5bn or 16x EBITDA.

Note that while LFCR is significantly smaller versus most of these industry transactions, the company’s focus on the high-quality fill-finish business suggests it might warrant a multiple in line or higher than these acquisitions. At 20x segment-level EBITDA, LFCR would be valued at $15/share, implying an 80%+ upside from current share price levels. With a more conservative 17x EBITDA multiple, LFCR shares would trade at c. $12.50/share.

Recent comments from the CEO have also confirmed the strategic review process is going smoothly:

These agreements demonstrate our focus on finding an optimal path forward for the business, while not losing sight of our continuous efforts to advance our project portfolio. We believe these agreements also improve the potential outcome from our strategic review process and open the door to greater flexibility for the Company going forward.

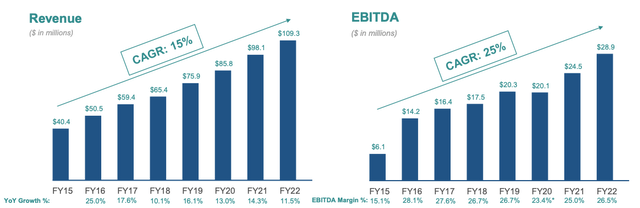

The third catalyst for LFCR is that the company is about to go current on its financials. Due to some accounting-related issues following recent asset divestments, the company hasn’t updated its financials since November ’22. Since then, a number of positive developments have happened, which the market might be not taking into account fully yet. First of all, LFCR has recently finalized the divestitures of its lower-margin/underperforming food segments, completing the company’s transformation into a high-quality fill-finish-focused CDMO business. CDMO business has been growing at +15% revenue CAGR and +25% EBITDA CAGR in the last eight years, which is not visible in the historical financials due to the overhang of the already divested food business. Clean financials and getting current on the reports will likely help LFCR’s stock to re-rate. Moreover, the company has recently announced a major commercial relationship agreement expansion with its key customer, which is expected to grow its total revenue/EBITDA by around 25-30%. This agreement was announced amidst the previous debt covenant breach crisis and it’s quite possible that the market doesn’t fully reflect it in the share price either.

Some Uncertainties

While the thesis is fairly straightforward and seemingly attractive, there are several uncertainties that might potentially explain LFCR’s current share price:

- Despite all the above-mentioned positives, visibility into the recent financials is limited. My valuation above is based on the management’s adjusted EBITDA guidance ($32m) issued in October ’22. The guidance was eventually withdrawn with the onset of the strategic review. It is not clear if it is still valid to expect the same adjusted EBITDA going forward, however, the recent developments, including confidence from LFCR’s major customer Alcon, suggest the company’s operational performance has not seen any significant negative impact since the time previous guidance was issued.

- Another question here is how comparable is LFCR to other CDMO industry acquisitions listed above. While the transactions were performed at >16x EBITDA multiples, they involved much larger and more diversified competitors. Several of LFCR’s CDMO peers are currently trading below these levels, including CTLT (12.2x 2023E EBITDA) and SCTL (6.5x 2023E EBITDA). Importantly, however, these peers have had limited presence in the fill-finish space and are instead focused on more commoditized CDMO sectors. Another data point is competitor Avid Bioservices (CDMO) which is currently valued at a much higher 30.8x FY2024 (ends in April) EBITDA. My point here is that the valuation multiples in the CDMO industry are widely scattered and it is thus difficult to pinpoint the correct multiple for LFCR without a precise understanding of to what extent each industry player is exposed to the fill-finish space.

Conclusion

At current share price levels, LFCR presents an interesting short-term special situation play with significant upside potential. Recent developments have largely eliminated any big downside scenarios, whereas the company is currently running a strategic review and is likely to get sold at a 50%-80% higher price than the stock is trading at right now.

Read the full article here