Overview

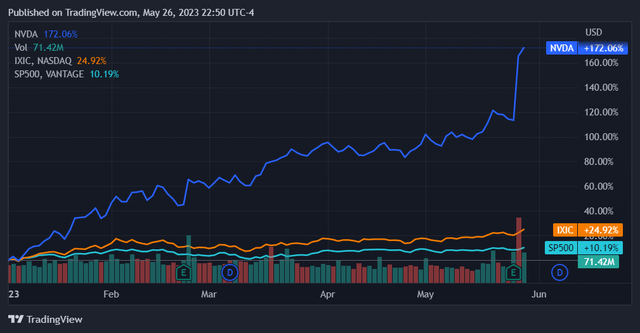

NVIDIA’s (NASDAQ:NVDA) latest earnings report might have been the biggest event in the stock market this year. Smashing expectations as well as issuing significantly upgraded guidance, NVIDIA stock responded with a 27% uptick that added $202B to its market capitalization in one trading day.

Now entering the weekend, NVIDIA continues to be the talk of the town amongst bulls and bears alike. Many investors are referring to it as an ‘unprecedented’ or ‘once in a lifetime’ earnings release, the likes of which have not been seen for companies that are already this large. I agree.

This recent performance has been an acceleration of NVIDIA stock’s already heady momentum so far this year. As of market close this week, NVIDIA has returned 6.9x the NASDAQ Composite as well as a staggering 16.89x the S&P 500 year-to-date.

Seeking Alpha

These latest results have supercharged what had already been an active discourse around NVIDIA. Bulls continue to state that NVIDIA is the market leader in a significant secular growth market while bears continue to express reservations about its lofty valuation.

The earnings results and the stock’s price action this past week have added ballast to both sides’ arguments without fundamentally changing the narrative for either.

In this article, I’ll put my chips down and posit my forward-looking view of the stock. I will do this by walking through the bear case in detail, extrapolating current NVIDIA metrics forward while also contextualizing it relative to comparable entities. Combining this with a review of its value proposition (business section) will allow me to determine if the stock is still worth buying at its current price.

Business

Before looking at NVIDIA’s stock I want to first comment on its business. While it is well-understood that NVIDIA is a market leader as well as a core beneficiary of the ongoing secular AI trend, it is sensible to evaluate its product and market positioning in more detail to see exactly why this is the case.

At present, NVIDIA’s sales are increasing rapidly due to it being the emerging market leader in providing custom chips that are particularly well-suited for artificial intelligence computing workloads. This is part of a longer-dated trend in what is NVIDIA’s real core competency: accelerated computing.

Accelerated computing is when a computing architecture makes use of another processor, distinct from the CPU, for certain tasks. In an accelerated computing architecture, the computer offloads certain types of tasks from the central processing unit onto this other processor. This coprocessor is specialized hardware that’s optimized for parallel computing, which allows for increased efficiency in the computing system overall.

This has been NVIDIA’s focus since 2006. Having been focused purely on hardware optimized for graphics processing until that point, NVIDIA expanded its offering – and total addressable market – significantly by releasing CUDA that year. CUDA software allowed for general parallel processing on NVIDIA hardware, allowing customers to leverage graphics cards for other types of parallel computing for the first time. This established accelerated computing as a paradigm particularly fit for large-scale, massively parallel, computer workloads.

It turns out that this kind of computing is what’s required for building artificial intelligence systems. Accelerated computing architecture is distinctly efficient for artificial intelligence workloads as AI requires massive levels of parallel processing, just like computer graphics. This has been the standard architecture for AI or machine learning workloads occurring at any reasonably large scale for some time. Companies already involved in genuine AI research have needed to operate a significant data center footprint with this architecture in order to develop AI software. Companies just starting out in AI ultimately need to have it or have access to it.

This all plays out in the enterprise GPU market. Companies need graphical processing units for their data centers in order to enable accelerated computing. The GPUs are the parallel-optimized processors that enable this computing paradigm. In this market, NVIDIA is undoubtedly king. As of Q4 2021, NVIDIA held 91.4% of the enterprise GPU market. The only other competitor of note was AMD, which held 8.5% of the market at that time. This is a dominant market position that indicates NVIDIA’s superior product and looks set to be sustained.

On a more speculative note, there is also another market worth mentioning: the personal computer GPU market. Just like enterprise data centers, GPUs and optimized coprocessors have also been increasingly present in consumer electronics. While video games may have kicked off and sustained this trend, artificial intelligence appears to have also become a factor: Apple has had dedicated AI coprocessors on iPhones since the iPhone 8, since Q3 2017. As artificial intelligence computing workloads become more commonplace, more of them may start occurring on end-user devices – which would likely increase demand in this market as well.

Perhaps surprisingly, NVIDIA is not the leader in the PC GPU market; Intel (INTC) is.

|

Company |

Q4 2022 PC GPU Market Share |

|

Intel |

71% |

|

NVIDIA |

17% |

|

AMD |

12% |

Source: Statista

It will be interesting to see how this market evolves as to demand and market share composition. While not as directly in play as the enterprise GPU market at present, it is one to keep an eye on as AI becomes more commonplace.

Overall we can see why it makes sense that NVIDIA is uniquely positioned to benefit from the AI trend and to continue doing so.

Valuation

Having outlined NVIDIA’s differentiation we can now look at its forward earnings and relative valuation. My goal here is to extrapolate current growth rates and valuations for NVIDIA and comparable entities, in order to see what the current market price implies. This has the effect of constructing the bear case in significantly more detail to see if it is reasonable to believe and over what interval.

I believe it is first sensible to compare NVIDIA against its primary competitors in the GPU space – Intel (INTC) and AMD (AMD).

Additionally, I think it also makes sense to compare NVIDIA to other very large ($500B+) technology stocks. This is due to this basket of stocks trading as forward-looking instruments with significant growth premiums, fluctuations in which can inform how the market is pricing the future earnings for NVIDIA on a relative basis.

The table below compares NVIDIA’s expected (consensus) forward earnings relative to its peers.

|

2022 EPS |

1 Yr. FWD EPS |

2023 EPS |

LT. FWD EPS CAGR |

2024 |

2025 |

2026 |

2027 |

2028 |

|

|

NVDA |

$1.74 |

28.91% |

$2.24 |

37.07% |

$3.07 |

$4.21 |

$5.78 |

$7.92 |

$10.85 |

|

AMD |

$0.84 |

13.97% |

$0.96 |

27.32% |

$1.22 |

$1.55 |

$1.98 |

$2.52 |

$3.20 |

|

INTC |

$1.94 |

-31.38% |

$1.33 |

3.26% |

$1.37 |

$1.42 |

$1.47 |

$1.51 |

$1.56 |

|

GOOG |

$4.56 |

3.79% |

$4.73 |

16.89% |

$5.53 |

$6.47 |

$7.56 |

$8.84 |

$10.33 |

|

MSFT |

$9.01 |

10.95% |

$10.00 |

11.97% |

$11.19 |

$12.53 |

$14.03 |

$15.71 |

$17.59 |

|

*AMZN |

-$0.27 |

-7.85% |

$0.78 |

36.73% |

$1.07 |

$1.46 |

$1.99 |

$2.73 |

$3.73 |

|

META |

$8.59 |

1.66% |

$8.73 |

19.71% |

$10.45 |

$12.51 |

$14.98 |

$17.93 |

$21.47 |

|

AAPL |

$5.89 |

5.21% |

$6.20 |

11.63% |

$6.92 |

$7.72 |

$8.62 |

$9.62 |

$10.74 |

|

TSLA |

$3.62 |

30.58% |

$4.73 |

21.73% |

$5.75 |

$7.00 |

$8.53 |

$10.38 |

$12.63 |

|

Avg EPS |

$3.99 |

$4.41 |

$5.18 |

$6.10 |

$7.21 |

$8.57 |

$10.23 |

Source: Seeking Alpha

*Diluted EPS. Due to slight differences in fiscal reporting periods between the firms, the 4 quarters occurring in calendar year 2022 are utilized for each.

**Amazon (AMZN) estimates are calculated in a distinct way due to the company having had negative EPS last fiscal year. To better reflect forward earnings CAGR, I assume that it will return to the average of its 10-year trailing yearly EPS ($0.78) in 2023 before applying expected long-term earnings growth rates. This allows for a forward estimate without the distorting numerical effects of crossing between negative/positive EPS.

At current expectations NVIDIA will handily surpass Intel in EPS for fiscal year 2023. It will then continue to outperform its semiconductor competitor peers while trailing mega technology averages overall, only crossing the average across these firms in 2028. At that point its EPS will surpass every peer apart from Microsoft (MSFT) and Meta (META). This shows us that NVIDIA’s relative earnings growth is significant even within a 5-year span, indicating a reasonable horizon for it to potentially grow into its valuation.

We can now look at how relative P/E valuation will evolve for NVIDIA and its peers over this timeframe. This chart does not account for changes in the quantity of shares outstanding.

|

Price |

P/E 2022 |

2023 |

2024 |

2025 |

2026 |

2027 |

2028 |

|

|

NVDA |

$390.28 |

224.30 |

174.23 |

127.13 |

92.70 |

67.52 |

49.28 |

35.97 |

|

AMD |

$127.40 |

151.67 |

132.71 |

104.43 |

82.19 |

64.34 |

50.56 |

39.81 |

|

INTC |

$28.92 |

14.91 |

21.74 |

21.11 |

20.37 |

19.67 |

19.15 |

18.54 |

|

GOOG |

$125.68 |

27.56 |

26.57 |

22.73 |

19.43 |

16.62 |

14.22 |

12.17 |

|

MSFT |

$334.05 |

37.08 |

33.41 |

29.85 |

26.66 |

23.81 |

21.26 |

18.99 |

|

AMZN |

$120.59 |

N/A |

154.60 |

112.70 |

82.60 |

60.60 |

44.17 |

32.33 |

|

META |

$263.50 |

30.68 |

30.18 |

25.22 |

21.06 |

17.59 |

14.70 |

12.27 |

|

AAPL |

$175.52 |

29.80 |

28.31 |

25.36 |

22.74 |

20.36 |

18.25 |

16.34 |

|

TSLA |

$194.00 |

53.59 |

41.01 |

33.74 |

27.71 |

22.74 |

18.69 |

15.36 |

|

Avg. P/E |

94.93 |

91.82 |

71.75 |

56.49 |

44.75 |

35.75 |

28.83 |

Source: Seeking Alpha

NVIDIA is indeed particularly expensive when considering its P/E multiple for the past year, 2023, and 2024. I will also note that Google (GOOG) remains remarkably cheap relative to its peers across this entire time horizon.

Starting in 2025 things start to look more reasonable for NVIDIA, with its P/E premium materially closer to the average. NVIDIA’S P/E gets close to AMDs in 2026 and actually goes below it in 2027, becoming even cheaper relatively in 2028.

By 2026 NVIDIA’s P/E premium will be around 50% of the average and less so after that, with less than a 25% premium in 2028. For current and historical premiums for this stock that can’t be considered particularly expensive.

|

2022 |

2023 |

2024 |

2025 |

2026 |

2027 |

2028 |

|

|

NVIDIA P/E / Avg P/E |

236.28% |

189.74% |

177.18% |

164.09% |

150.88% |

137.83% |

124.78% |

Source: Seeking Alpha

Considering its relative growth rates, I don’t think that NVIDIA looks too expensive on a forward basis. It is set to become relatively cheaper each year and is not even priced as expensively as AMD from 2027 onwards.

Risks

The first risk for this scenario playing out would be a change in relative growth rates across this basket of firms. NVIDIA’s semiconductor competitors can start to absorb market share from it, or to accelerate their own growth rates materially, its forward price will not be as appealing on a relative basis and it could no longer be considered an opportune investment at current prices.

The other risk would be a reduction in the company’s growth premium, irrespective of its relative valuation. If NVIDIA ends up underperforming its now significantly higher expectations for growth, investors would expect less future returns and could sell off shares. This would lower the stock’s growth premium and bring the company’s trading P/E multiple to something more in line with the sector median.

The final and arguably most significant risk to NVIDIA is supply chain risk. NVIDIA’s business is built around designing but not producing its own chips, and its business would be hampered severely by disruptions to its primarily Taiwan-based supply chain. While supply chain diversification efforts are ongoing at the TSMC (TSM) level, they are still in the early stages. As such, I consider this risk to be material. I’ll reiterate that owning Intel stock would be an excellent hedge against any potentiality of this nature.

Conclusion

At current prices and expected growth rates, NVIDIA is projected to grow into its valuation in less than a decade and become relatively cheaper a lot sooner than that. Continued high growth expectations would likely see the stock maintain a healthy growth premium in its valuation that would keep it close to its current/historical P/E multiple. All else being equal, I would expect this growth premium to persist for as long as the company can deliver results at the higher end of guidance or better during this current stage of growth.

Along with this, there is a fundamental undercurrent of improving relative multiples as compared to other very large technology companies. This implies potential upside for the stock over the next 5 years or more. Given ongoing macroeconomic uncertainties, however, I am looking to trade this stock with a one-year horizon, a timeframe within which I believe there is ample opportunity for further returns.

To be clear, I am expecting NVIDIA to both grow earnings as well as maintain or exceed its current P/E multiple throughout the next four quarters. Continuing to grow earnings at its current level will allow NVIDIA to maintain robust future growth assumptions on the part of investors and maintain the present level of growth premium for its shares. As with this most recent quarter, I am expecting subsequent quarters to continue to pull its future performance forward to current share price appreciation; an equal multiple at higher earnings will then yield a higher share price. More than one year out, my certainty around macroeconomic conditions that affect the stock decreases significantly and will have to be re-evaluated at that time. Considering all of this, NVIDIA stock is still a good buy.

Read the full article here