Thesis

In the second quarter of 2023, PC Connection (NASDAQ:NASDAQ:CNXN) reported non-GAAP EPS of $0.80 that beat by $0.20, and revenue of $733.5M that missed by $30.22M. While net sales witnessed a contraction, the company’s strategic focus on integrated solutions and adaptability allowed them to achieve growth in specific segments. However, the article also points out some potential risks, such as overvaluation, slow earnings growth rate, and liquidity concerns. Overall, the analysis suggests that PC Connection may be a “hold” with the need for careful monitoring of key factors before further investments.

Company Profile

PC Connection, Inc., an entity in the international IT solutions domain, operates via three key segments: Business Solutions, Enterprise Solutions, and Public Sector Solutions. With a portfolio spanning across numerous IT commodities and services—such as computer systems, data center solutions, and networking communications—the company puts forth its proficiency in bespoke design, configuration, and implementation. Originating in 1982 and headquartered in Merrimack, New Hampshire, PC Connection employs a blend of marketing tactics, from outbound telemarketing to field sales and diverse media advertising, to amplify its global presence.

PC Connection’s Q2 Earnings Highlights

In the second quarter of 2023, PC Connection continued to widen its scope of offerings and successfully onboard new accounts throughout what management described as a “challenging” quarter. So while the broader landscape witnessed a contraction with net sales falling by 11.5%, the company’s strategy allowed them to buck the trend, recording growth in their integrated solutions business. PC Connection also showcased adaptability in weathering economic difficulties, as indicated by an improvement in gross margins by 90 basis points, rising to 17.4%.

Zooming in on specific segments, the company’s Public Sector Solutions business saw considerable success, with a robust 22.6% increase in Q2 net sales. This was largely propelled by strong demand in both K-12 and federal government sectors. On the other hand, the Business Solutions segment managed to enhance gross margins significantly by 356 basis points, reaching a record 23.5%. This increase was triggered by a strategic shift in product mix favoring data center products, coupled with a heightened mix of netted down revenue.

The company also saw promising developments in the Healthcare sector, where revenue grew by 5%. The key driver of this growth was the focus on workplace transformation solutions. Complementing these achievements, PC Connection earned industry recognition, clinching two Partner of the Year Awards from tech giant Microsoft.

In terms of financial strategy, PC Connection continued to streamline its cost structure. The company managed to reduce SG&A expenses by $1.2 million, owing largely to cost reduction initiatives. Simultaneously, the company recorded a slightly reduced effective tax rate of 26.9%, further boosting its bottom line.

Investor relations also received due attention. PC Connection showcased a shareholder-friendly attitude by repurchasing shares and dispensing dividends. In another commendable development, the company’s cash flow from operations saw a rather large boost with a $143.8 million increase from the previous year. This was achieved through lowering accounts receivable inventory and augmenting accounts payable. At the end of the quarter, the company boasted a comfortable financial position with cash and cash equivalents amounting to $244 million.

Performance

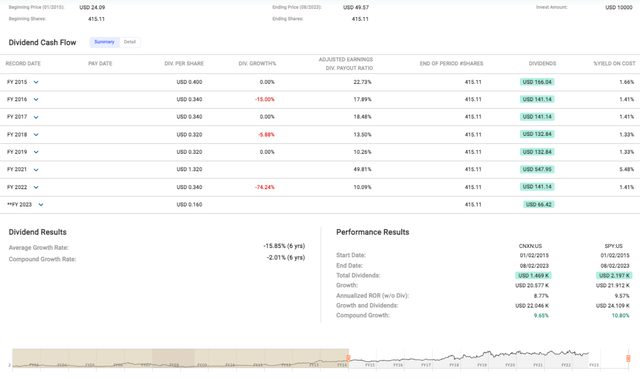

PC Connection’s share price over the medium-term has more than doubled from $24.09 at the start of 2015 to $49.57 by August 2023. That’s a fairly impressive feat, especially for a mid-size player in the highly competitive tech retail space.

Fast Graphs

The company’s average dividend growth rate at -15.85% and the compound growth rate at -2.01% over the past six years illustrate a company grappling with its dividend policy, possibly indicative of management’s efforts to balance payout and reinvestment in a shifting business environment.

If we compare PC Connection’s performance with the S&P 500 Index, its annualized rate of return (ROR) without dividends was 8.77% against S&P’s 9.57%, only slightly lagging the broader market. When considering growth and dividends, PC Connection achieved compound growth of 9.65%, a hairline behind the S&P’s 10.80%.

Valuation

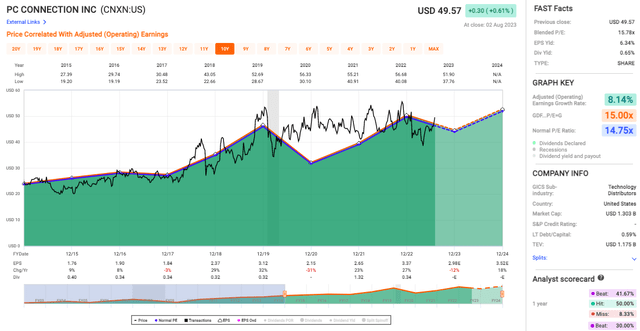

PC Connection’s Blended P/E of 15.78x is slightly above the Normal P/E Ratio of 14.75x suggesting that the stock may be somewhat overvalued.

Fast Graphs

The Adjusted Earnings Growth Rate at 8.14% is respectable, but it’s not particularly outstanding. Nevertheless, steady growth is often better than erratic, high growth since it suggests a certain level of stability in the company’s operations.

Given these details, it appears that PC Connection is a company that is potentially overvalued, with a relatively low dividend yield but a decent earnings yield and a stable earnings growth rate.

Risks & Headwinds

Despite a series of promising strides, PC Connection grappled with a multitude of challenges during the second quarter. A key setback was the aforementioned 11.5% reduction in net sales, amounting to $733.5 million. Concurrently, gross profit experienced a 6.7% decrease, settling at $127.8 million. This can be largely attributed to waning demand for endpoint devices, a consequence of sluggish hiring rates and diminishing headcounts in the face of challenging economic circumstances.

A decline was observed in operating income as well, which dropped by 27.9% to land at $25.1 million. Net income mirrored this trend with a 22.4% decrease to $19.7 million. This clearly underscores a contraction in the company’s profitability. Echoing the downward trajectory, diluted earnings per share receded by 22.3% to $0.75, and the adjusted earnings per share experienced a fall of 17.2%, taking it to $0.80.

A sector-wise analysis reveals similar distress. The Business Solutions segment reported a substantial 20.5% contraction in net sales. Meanwhile, the Enterprise Solutions segment recorded a 17.7% drop in net sales. The repercussions were felt in the gross profit figures for both segments, with the Business Solutions and Enterprise segments reporting a decline of 6.3% and 15.1% respectively. Gross margin in the Public Sector segment faced a 110 basis points drop to reach 12.7%, which was the result of an increased mix of endpoint solutions.

Lastly, adding to the company’s challenges, Selling, General and Administrative expenses (even though the company managed to reduce SG&A expenses by $1.2 million) constituted 13.8% of net sales, primarily as a fallout of lower revenues. The company also had to bear restructuring and other related costs, which amounted to $1.7 million.

Final Takeaway

Given the presented financial analysis, I would rate PC Connection as a “hold.” Despite facing some challenges, including lower net sales and operating income, the company demonstrated resilience with its strategic shift leading to increased margins in key sectors and strong cash position. With its current valuation being slightly above average and potential liquidity strains and slow adjusted earnings growth rate, it may be wise to monitor these factors prior to making additional investments.

Read the full article here