Main Thesis & Background

The purpose of this article is to evaluate the PIMCO Dynamic Income Opportunities Fund (NYSE:PDO) as an investment option at its current market price. This is a closed-end fund whose objective is “current income as a primary objective and capital appreciation as a secondary objective”.

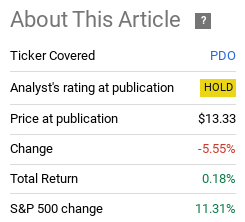

This is a fund I have owned for a while, but generally been disappointed in. It has not performed very well and when 2023 got underway I didn’t have a lot of optimism. I saw merit to holding, but a new “buy” argument was one that didn’t sit right with me. Fast forward to today, and my neutral outlook was vindicated. The fund’s total return has been about as flat as flat can be:

Fund Performance (Seeking Alpha)

Of course, the return wasn’t negative, but that isn’t saying a whole lot when the equity market is in bull mode. Seeing modest gains or no gains at all would leave an investor in the dust when inflation is high and other sectors and options are doing well.

With this backdrop in mind I thought it was time to take another look at PDO and see if an upgrade was warranted for the final stages of 2023. After careful review, I still see some headline risks that make an upgrade a difficult case to make. I will therefore be keeping my “hold” rating intact and will explain why in more detail below.

Risk-On Sectors Are Providing High Levels Of Income

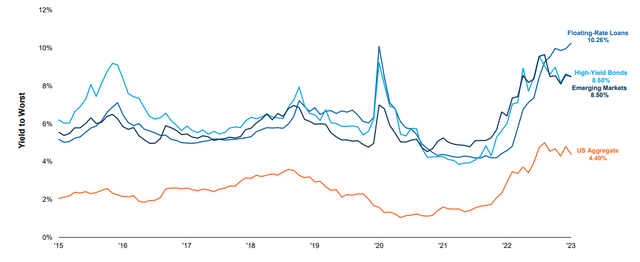

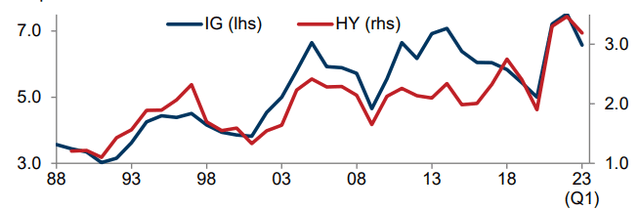

To start I will take a macro-view of where we are in the debt markets. This is relevant for PDO (and many other high yielding CEFs) because it lends an argument for why anyone would be considering this fund at the moment. For example, we do see that risk-on assets are offering high income streams for the time being. With inflation beginning to finally moderate (a few years after the “transitory” message went out of style!) the yields offered by junk credit looks attractive. This is true for junk bonds, loans, and non-US debt, which are clearly offering more than the average US aggregate (IG-rated) bond fund could offer:

Current Sector Yields (FactSet)

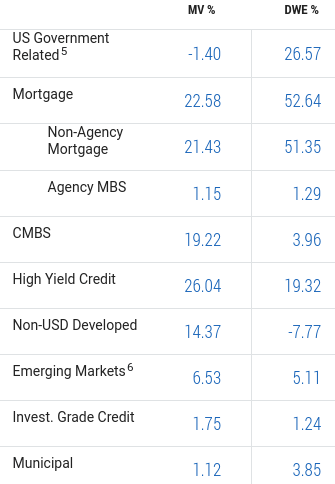

This matters because PDO is indeed a more risk-on CEF. The fund has a diversified basket of securities to be fair, but it is still made up predominantly of non-agency MBS and high yield credit, as well as non-US issues:

PDO’s Sector Breakdown (PIMCO)

I bring this up because it lends merit to at least giving this fund consideration. While I will get to the aspects that give me pause later in this review, the fact is that if one wants to beat inflation purely through income, they have to take on risk to do so. PDO is by no means the only option to consider for this objective, but it is a popular choice among Seeking Alpha followers. In this light it should be clear why I wanted to give this fund consideration again as we move closer to Q4. The current yield of 12% is realistic because the fund owns some riskier credit sectors. For the risk type of income-seeking investor, this could be a reasonable environment to take on this exposure.

High Yield Corner Has Some Wiggle Room

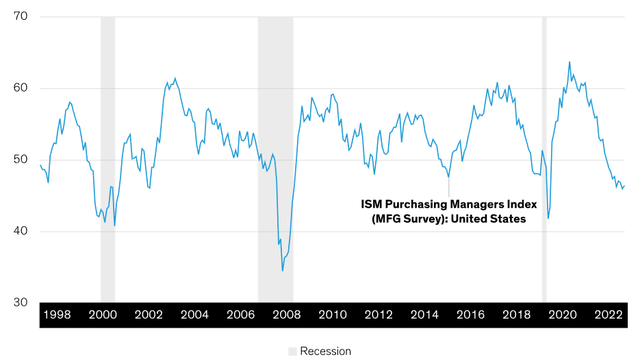

Expanding on the above point, the high yield sector doesn’t actually appear overly risky right now. This may seem counter-intuitive because all we have been hearing about for the past year or year and a half is how the US (and other parts of the developed world) are pushing towards a recession. Major economic signals seem to indicate that is the likely scenario, yet we keep on avoiding it all the same. Still, manufacturing indicators are pointing quite heavily towards that base case as the year has gone on:

PMI (Index) (US) (Bloomberg)

This begs the obvious question: if difficult times are ahead, why would someone want exposure to riskier asset classes / debt sectors?

The answer is that, fortunately, the high yield corner of the market is entering this period from a pretty strong starting point. If we look at corporate fiscal health, signs are fairly strong. While interest coverage ratios have been weakening in the short-term, they stood at historically high levels when the year got underway. This has resulted in a weakening environment that still sports strong coverage metrics for both IG and high yield debt:

Interest Coverage Ratios (Corporate – US) (Goldman Sachs)

This doesn’t mean that PDO is an automatic buy (or sell) at these levels. But it does highlight that “riskier” debt at this juncture is not overly risky. That could change – and change fast – if economic conditions deteriorate. But for the time being I am not overly concerned about seeing a spike in defaults or delinquencies going forward. That is supportive of not being too bearish on PDO and other leveraged funds.

Income Doesn’t Look Sustainable

Let us now consider some of the challenges facing PDO. While there are legitimate reasons to consider buying this fund, so too are there reasons for avoiding. This push-pull dynamic is central to why I see “hold” as the appropriate choice here.

Concern number one has to do with income. PIMCO’s August UNII report (contains July’s figures) was released last week and the reality is things aren’t very pretty. This is true across the board for its leveraged CEFs, and that is inclusive of PDO. The UNII balance has been growing and coverage ratios leave quite a bit to be desired:

UNII Report (PIMCO)

The takeaway here should be clear. PDO is not earning enough in income to cover its current distribution. The only bright side to this is that the yield (at 12%) is high enough that the fund can afford a cut and still draw in plenty of investor interest. But until that happens that headwind of a cut remains a very real hurdle. Unless we see dramatic improvement soon, this is something owners of the fund need to prepare for.

Valuation Not Crazy, But Not A Bargain Either

This next topic is also a bit mixed. On the surface, PDO seems like a reasonable option compared to similar CEFs from PIMCO. Many of its sister funds sport high premiums to NAV, making PDO’s 2% premium look less frothy by comparison:

Valuation Metrics (PIMCO)

So this isn’t truly a “bad” attribute going forward.

But, on the other hand, it doesn’t really scream opportunity either. A 2% premium is still a premium, and that should make readers cautious. Back in March during my last review, PDO was trading just slightly above par. As we now know, that wasn’t a “buy” signal either because the fund’s return has been zip since then.

My summation would be that if buying at a 0% premium didn’t amount to anything, how can I surmise that a 2% premium is going to be a great buying opportunity? I can’t – and that is why I remain stuck with a neutral outlook.

Mortgage Bonds Another Reason For Neutral Opinion

A discussion on PDO would not be complete without touching on the state of the US housing market. As the sector graphic earlier showed us, PDO has almost a quarter of its total assets exposed to the residential mortgage market. The majority of these securities for PDO reside in the non-agency corner, which means they are not backed by the federal housing agencies.

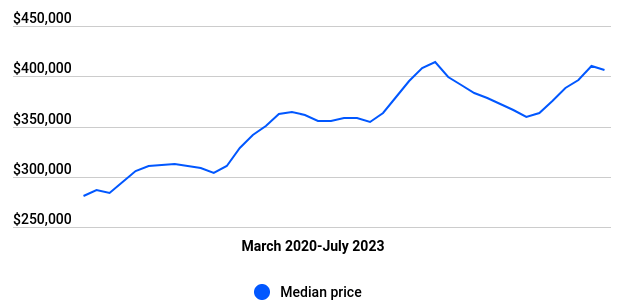

This makes the mortgages a bit riskier but they are still generally considered a safer asset type on average. This is especially true when employment is strong and home values have been rising. Those residing in these homes have the means and the incentive to make good on their payments in that scenario:

Median Sale Price (US homes) (National Association of Realtors)

This helps to support the underlying value of the MBS (both agency and non-agency) within PDO’s portfolio. As long as the values of the homes backing the loans are rising in value and homeowners are making good on their obligations, this asset class will be resilient.

There is a downside to investing in this sector at the moment, however. Much of this rests on the fact that these loans are fixed-rate and were locked in during periods of lower rates (compared to current). This means that as inflation remains high and the Fed keeps rates higher for longer, the attractiveness of these assets declines because investors can earn higher yields elsewhere (those loans/debt that is originating at current rates).

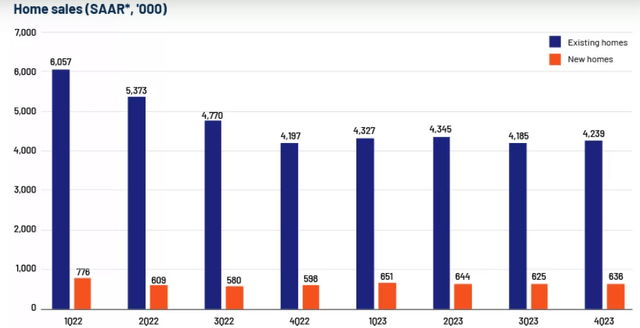

There are positive underlying factors that balance this risk out. This is why I am not bearish on the sector, or PDO by extension. While rising income opportunities elsewhere does limit the attractiveness of fixed-rate debt with long durations, the lack of new mortgage originations helps to limit the downside risk to this sector. Simply put, as fewer mortgages get originated, that means less supply on the market. That supply dynamic will keep the price of securities higher, all other things being equal. This has been a trend – on a year-over-year basis – throughout 2023 compared to 2022 when it comes to new home sales domestically:

Home Sales By Quarter (US) (SIFMA)

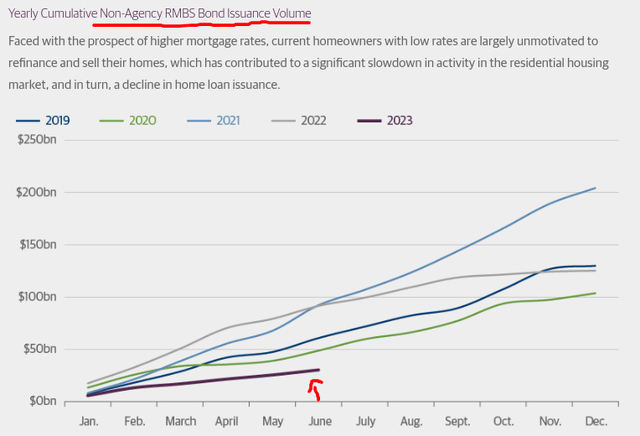

This is not a story that is going to suddenly reverse in my view. With interest rates high on a historical basis (for the past two decades) and current homeowners reluctant to uproot, it is going to take time to see new sales / mortgage originations spike higher. Affordability is tight and that is making new purchases less common than just a short one or two years ago. While new home sales aren’t specific to non-agency MBS, we see a similar story emerge in terms of new issuance when we examine that sub-sector of the MBS market:

Non-Agency MBS Issuance By Year (residential) (Guggenheim)

What I am getting at here is that this is yet another metric for PDO that is a mixed bag. There are supporting underlying factors and other factors that are not quite as attractive. When I see this type of environment – hold is the logical choice.

Bottom-line

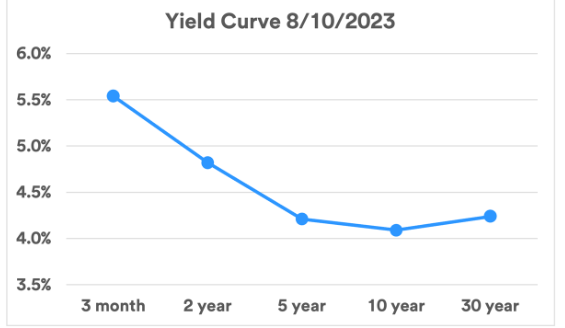

PDO continues to see challenges being a risk-on, leveraged play in a rising interest rate world. The fund has returned investors very little since the end of Q1 and many market conditions – such as an inverted yield curve and a looming recession – will continue to pressure forward returns in all likelihood:

T-Bill Yield Curve (US Treasury)

There are some aspects to be bullish on though. The fund’s premium to NAV is very reasonable and the income stream is quite high. While I see an income cut as a risk, it isn’t as serious as it might sound given that PDO can afford a modest cut and still offer a double-digit yield. That should limit any post-cut fallout that we have seen in other PIMCO CEFs in the past.

In sum, there are enough pros and cons to make the investment picture a bit muddled. When that is the case I generally exercise caution and that is what I would suggest here as well. Therefore, I will be keeping my “hold” rating consistent for the latter stages of 2023 and would urge my followers to approach any new positions in PDO very selectively at this time.

Read the full article here