Investment

PGT Innovations, Inc. (NYSE: PGTI) should face near-term headwinds from softening in demand of the residential market. Despite this, I am of the opinion that the weakness is already priced at the current levels as PGTI’s stock is currently trading at a discount to its 5-year P/E average. Additionally, the company’s prospects for long-term growth are promising, as evidenced by the upward trend in home equity and underbuilt homes in the US. Therefore, I recommend a buy rating for this stock.

Brief Recap

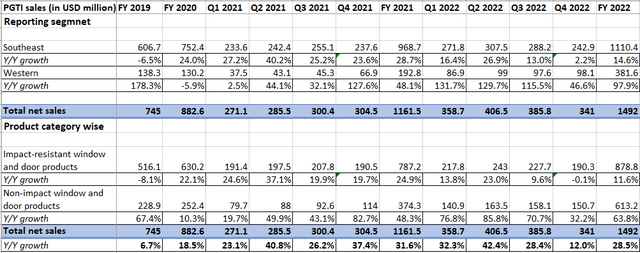

PGT Innovations reported 12% Y/Y revenue growth in the fourth quarter of FY2022, driven by its legacy businesses and the recent acquisition of Anlin & Martin, which was partially offset by the negative impacts of Hurricane Ian and the Ransomware attack. The Western segment grew 46.6% Y/Y (15% organically) while the Southeast segment had a modest growth of 2.2% Y/Y (2% organically) during the fourth quarter. This lower growth rate in the Southeast segment was primarily impacted due to the aforementioned two events during the quarter.

PGTI’s Historical revenue growth (company data, BI Insights )

Moving on to the margin performance of the company, due to unfavourable events (Hurricane Ian & the Ransomware attack), the company’s management was unable to align the cost structure with the operating capacity of the plants which resulted in a decremental margin during the fourth quarter of FY2022. Moreover, the increase in adjusted SG&A due to the recent acquisition, expansion of new south operations, increased labour & distribution cost, and an increase in marketing investment also negatively impacted the margins.

PGTI’s Historical margins (company data, BI Insights)

Near-term Outlook

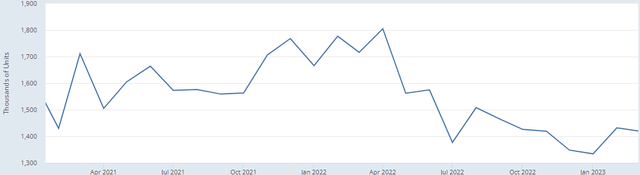

PGT innovation is expected to witness a volume decline in FY2023 due to softening in demand in the residential market. Federal Reserve has increased interest rates which should create affordability concerns and discourage potential buyers from making investments in the housing sector. Moreover, housing starts stood at a decline of approximately 17% Y/Y as of March 2023 which also indicates declining demand in the residential market in the coming quarters. Despite ongoing concerns about weakened demand, the company is focusing to meet the needs of builders and customers by introducing innovative new glass products. As an example, PGTI offers a diamond glass impact-resistant unit with improved clarity, scratch resistance, and up to 45% lighter weight than the standard product. This should help PGTI to increase demand for its products and support revenue growth in FY2023. Moreover, PGTI should also benefit from the recent acquisition of Martin Garage Doors. Martin deals in premium garage doors which should expand the brand presence and geographic footprint of PGTI. Hence, the revenue flow from this recent acquisition should act as a growth tailwind for the topline of PGTI.

Housing starts (FRED)

On the other hand, I anticipate that the margins should decline Y/Y in FY2023 due to volume deleverage. As mentioned earlier, the weakening demand is expected to cause a decrease in volume for the coming quarter. This, in turn, is likely to result in volume deleverage and have a negative impact on the margins. However, the company is taking proactive actions for cost reduction, under which the company has decided to reduce the unutilized assets by discontinuing these product lines within the portfolio. This should partially offset some headwinds from volume deleverage.

Long-term Outlook

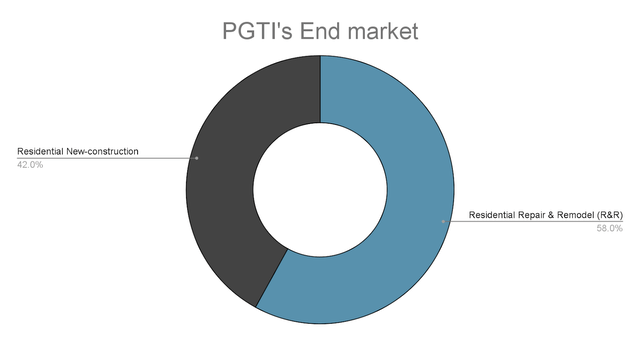

While it is true that PGT Innovation is expected to witness headwinds in the near term, the secular growth tailwinds in new construction and R&R markets make me bullish on the stock. These trends include ageing housing stock across the U.S. and a significant rise in home equity & underbuilt homes in the U.S. By 2027, approximately 24 million homes in the U.S. are expected to reach the prime remodelling age. This increase in remodelling activity should boost the demand for the windows and doors of the PGTI, thereby benefiting its R&R business in the upcoming years. Additionally, the significant rise in average homeowners’ equity, which is at an all-time high of 3,48,000 also indicates that homeowners are expected to spend more on their home R&R in the coming years.

Furthermore, the current situation of underbuilt homes in the U.S. has created a need for an additional 17 million housing units to satisfy demand, which should be advantageous for the new residential market. Consequently, this is expected to create a favourable growth environment for the new construction business of the company in the upcoming years.

PGTI’s end market (PGTI investor relation)

Valuation

PGT Innovations is currently trading at a 14.47x FY2023 consensus EPS estimate of $1.76 and a 12.45x FY2024 consensus EPS estimate of $2.04. This is a discount to its 5-year average (FWD) P/E of 16.89x. Moreover, a comparison with the sector median also suggests the company is at a discount due to the anticipation that softening in the housing market should have a negative impact on the performance of PGT innovations in the near term.

Risk

My thesis is built on the assumption that there should be a shallow downturn in the residential market. More than expected inflation can make the Federal Reserve more hawkish towards rising interest rates, which can lead to a residential market downturn much more severe. Moreover, the company is developing new innovative products which are expected to support revenue growth in the coming quarters. However, the traction of these products in the market remains uncertain which may have a negative impact on PGTI’s top-line and stock performance.

Conclusion

While the near-term prospects for PGT innovations may appear bleak, I believe the adverse effects are already priced into the current stock prices. Consequently, I anticipate that this stock has good upside potential over the next few years, thanks to the positive momentum generated by secular growth tailwinds. Therefore, I am bullish on this stock.

Read the full article here